Economic and Market Review

March 30, 2024

| Equity Indices | YTD Return |

| Dow Jones | 4.98% |

| S&P500 | 9.94% |

| NASDAQ | 9.23% |

| MSCI – Europe | 6.95% |

| MSCI–Emerging | 1.79% |

| Bonds | |

| 2yr Treasury | 4.71% |

| 10yr Treasury | 4.32% |

| 10yr Municipal | 2.54% |

| U.S. Corporate | 5.41% |

| Commodities | |

| Gold | $2254.41/oz |

| Silver | $25.15/oz |

| Crude Oil (WTI) | $83.92/bbl |

| Natural Gas | $1.83/MMBtu |

| Currencies | |

| CAD/USD | $0.74 |

| GBP/USD | $1.26 |

| USD/JPY | ¥151.60 |

| EUR/USD | $1.07 |

Overview

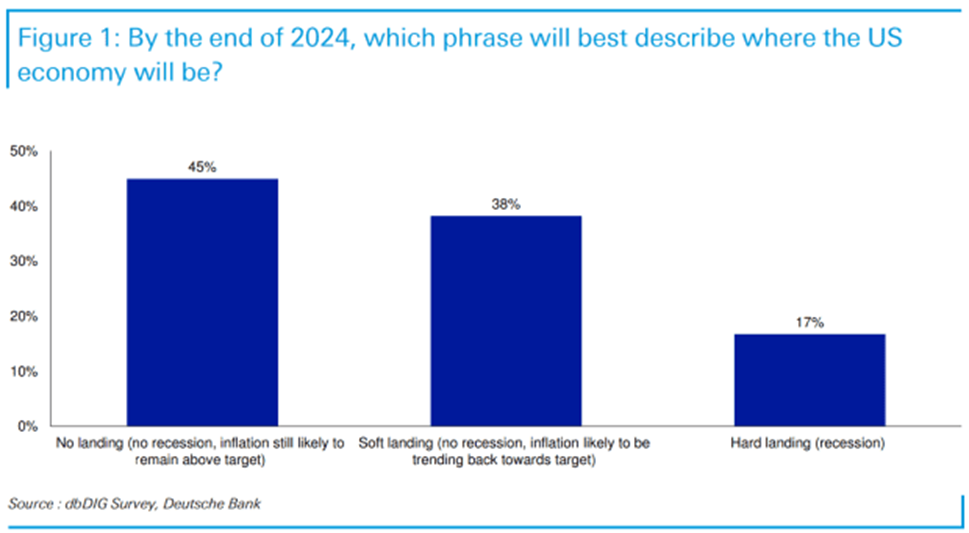

The S&P 500’s 25% run-up over the trailing 5 months could continue higher. A run-up of this rapid has only occurred 10 times since the 1930s. As discussed last month, this was overwhelmingly led by gains in the “Magnificent 7,” who have seen explosive growth. Investor sentiment has shifted, with a Deutsche Bank survey indicating that 45% of investors now expect a “No-Landing” scenario for the US economy, where inflation remains above the 2% target while economic growth continues robustly.

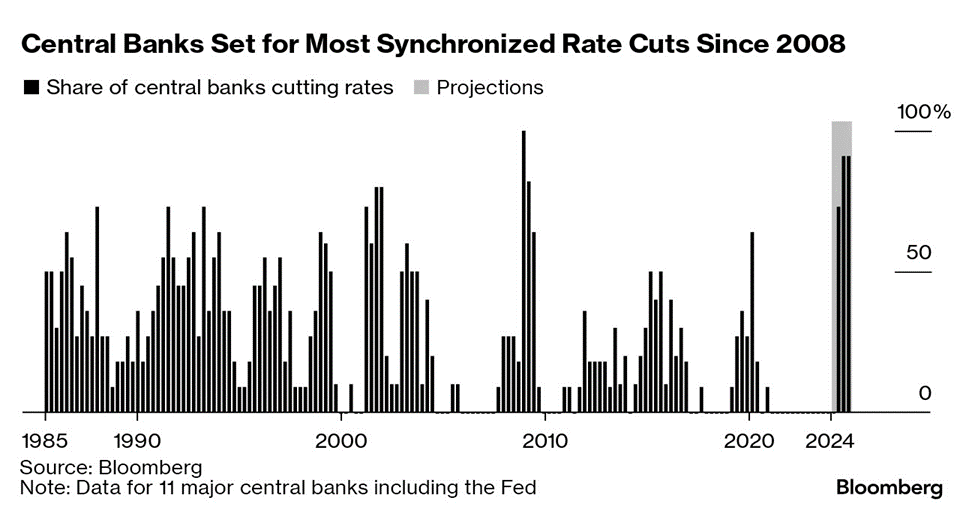

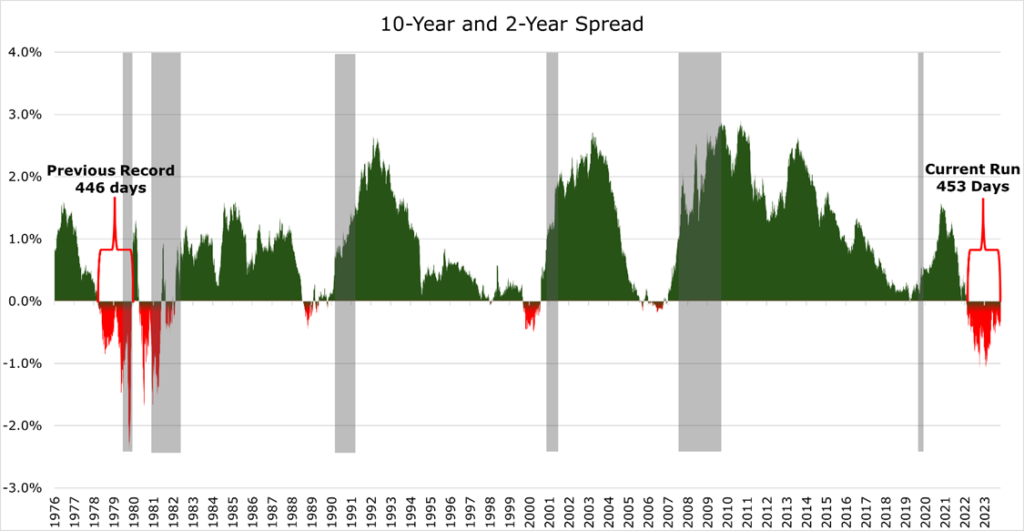

Bond markets have priced in long-term uncertainty, with the 2-year to 10-year spread being inverted for a record period, typically indicating impending negative economic and financial market activity. This comes as the world’s major central banks prepare for significant rate cuts, potentially marking a dovish era where long-term inflation overshoots are tolerated to maintain strong economic growth.

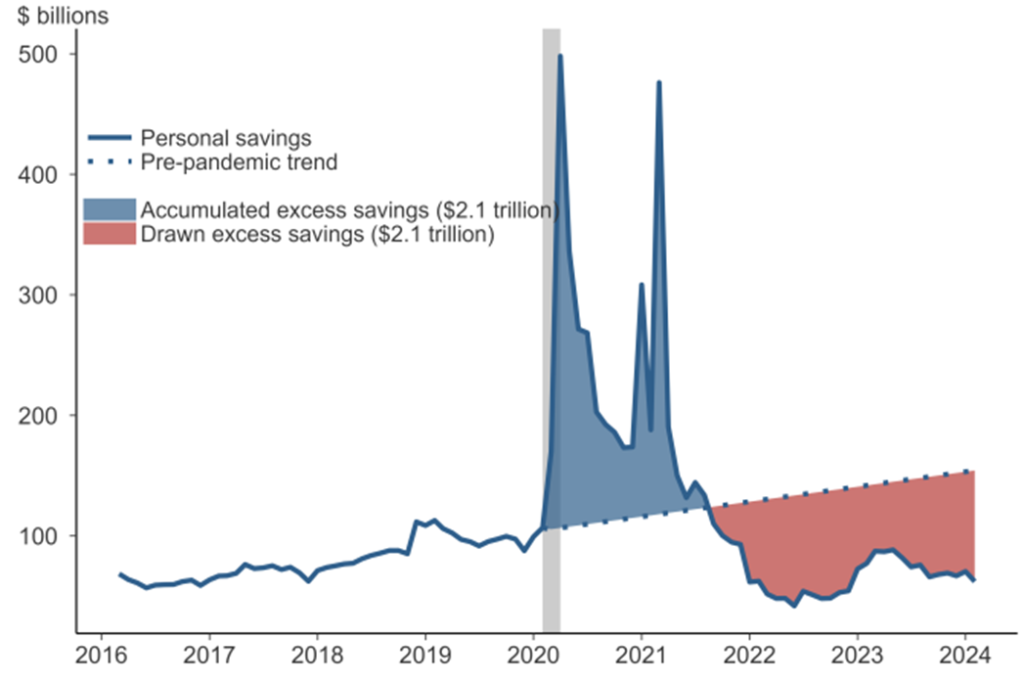

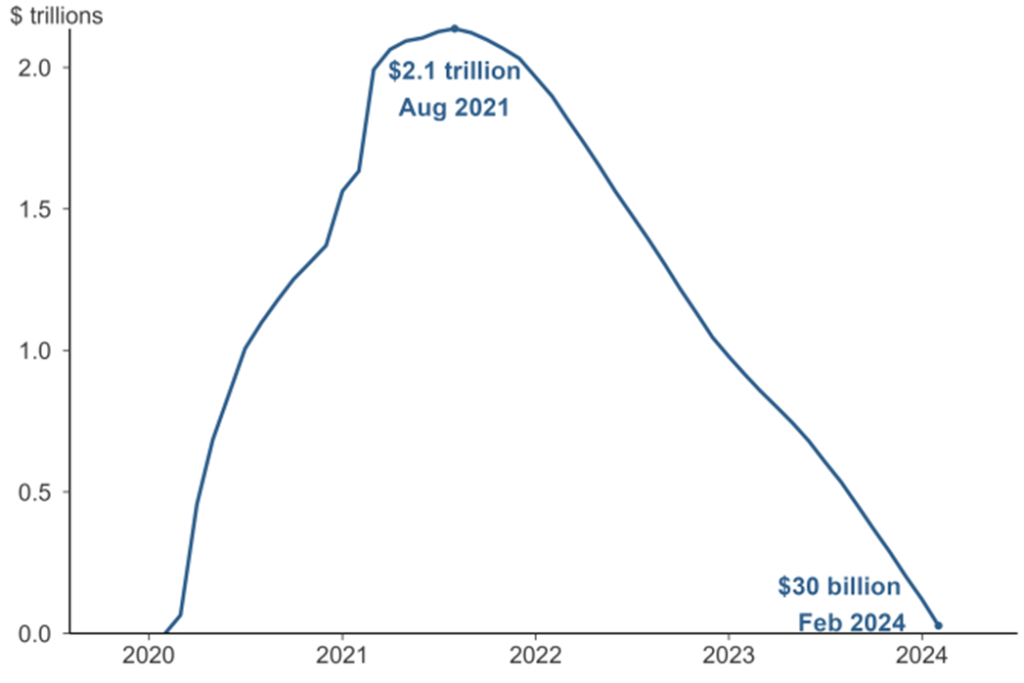

The era of abundant pandemic savings driving excess consumer spending appears to be waning, with less than $30 billion left out of a peak of $2.1 trillion. The housing market has offered no relief to consumers, with the price-to-household income ratio reaching unprecedented levels.

Emerging markets are facing significant challenges as global debt levels soar to record highs. These economies are grappling with increased debt distress as their servicing costs have risen sharply. High borrowing costs driven by a strong US dollar and elevated global interest rates have put immense pressure on these countries, requiring unsustainable growth rates to manage their debt burdens.

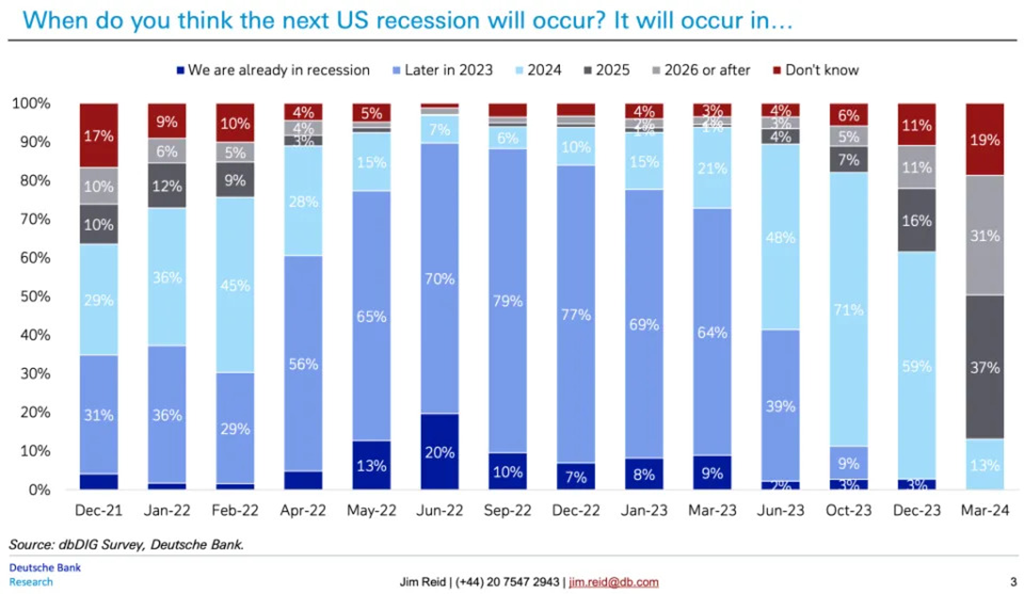

Investors Now Expect “No Landing”

The debate of whether the Fed would tame inflation with a recession (hard landing) or manage to bring down inflation without major economic contraction (soft landing) has seen a drastic shift in recent weeks. According to a Deutsche Bank survey, 45% of investors now believe the US is heading for a “No-Landing” scenario. In this scenario, inflation remains sticky above the 2% target, but economic growth remains robust.

As a backdrop, the 11 largest central banks are prepped to begin the largest campaign of rate cuts since the 2008 global financial crisis. These rate cuts in the face of sticky inflation may represent a new, more dovish era of central banking, in which central banks begin to tolerate long-term inflation overshoots if they preserve strong economic growth.

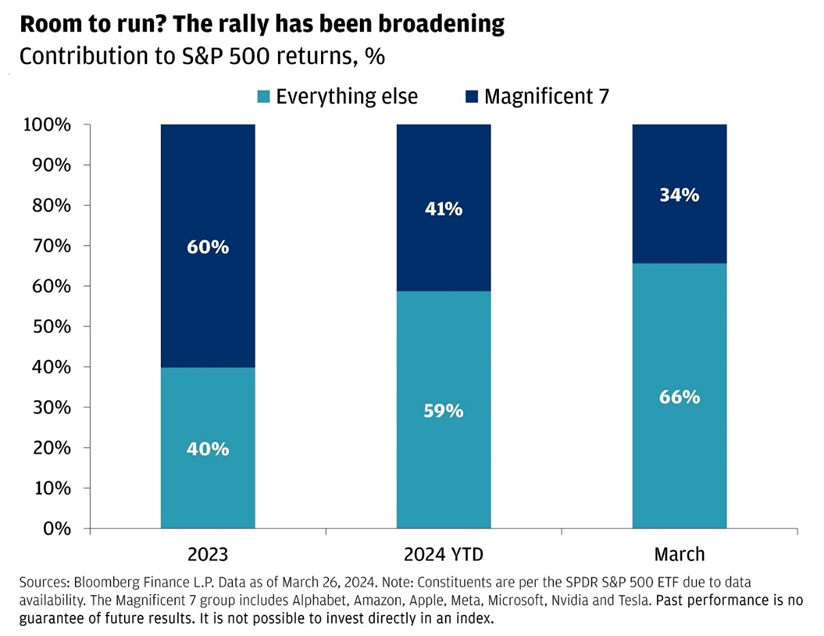

While typically persistent inflation would weigh stocks down, the central bank’s seeming acceptance of long-term inflation in exchange for continued economic growth has seen the rally in the S&P500 expand beyond the “Magnificent 7” – though there is still ground to make up.

With the Fed seemingly avoiding a recession, the era of economic uncertainty has continued, with economists still split on what the future holds. Over the short term, it seems that sticky inflation expectations and a reduction in the number of forecasted interest rate cuts have continued to be offset by strong US GDP growth and AI hype.

Longest Yield Curve Inversion on Record

Bond markets have aggressively priced in long-term uncertainty, with the 2-year – 10-year spread being inverted for the longest period since the 1970s. Typically, an inverted yield curve is a negative indicator of economic activity and financial markets. Higher short-term yields increase borrowing costs on consumer and business loans. Lower long-term yields are indicative of investors being risk averse, with money being parked in safe long-term government assets rather than invested in the short-term.

Pandemic Savings Are Finally Drying Up

Much of the reason behind sticky inflation is excess consumer spending, which we discussed in our consumer spending article here. During the pandemic, US households experienced a significant increase in savings due to fiscal support and a decrease in spending. This led to a rapid rise in aggregate personal savings to about $2.1 trillion over the typical level. However, as economic activity began to recover, households started using their excess savings to support spending, leading to a decrease in savings below the pre-pandemic trend by late 2021.

The most recent estimates by the Bureau of Economic Analysis and the San Fransisco Fed indicate that less than $30 billion of this excess savings remain. Later in the year, this could provide relief to headline inflation as consumers cut down spending and resume saving from current income. Equally, though, this could weigh down GDP numbers.

Debt Crisis Weighs Globally

Global debt hit a record high in 2023, reaching $313 trillion, with the global debt-to-GDP now 330%. This is up 20.5% from 2019, which had a debt-to-GDP ratio of 320%. According to the Institute of International Finance, around half of the increase came from advanced economies, though economic growth has allowed them to pay down excess borrowing and decrease the global debt-to-GDP ratio.

The US may be one of the few that have escaped the period of high debt and inflation relatively unscathed. The broader Eurozone slipped into a shallow recession in early 2024, with the worst growth rates seen since the late 90s. The near-term isn’t much brighter for Europe, with the EU economic bellwethers France and Germany estimating persistently weak growth continuing into 2024.

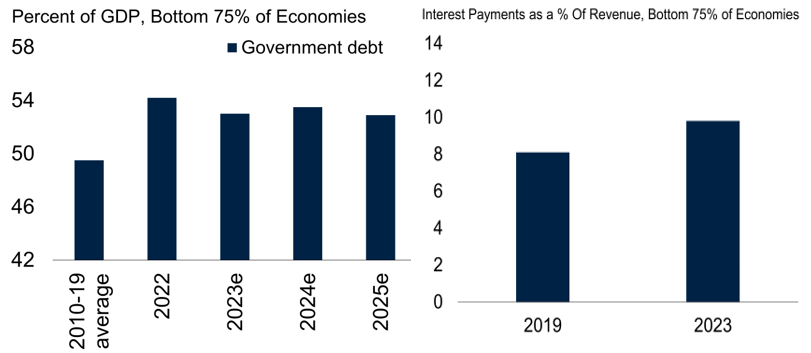

However, the situation with the emerging and developing economies has become desperate. Debt-to-GDP for the emerging markets (bottom 75% of global economies) has seen a drastic degradation, with 69% having higher debt-to-GDP than before the pandemic, now averaging 53%. While this level is much lower than the advanced (top 25%) economy average of 112.7%, emerging market economies typically have to issue debt at burdensome interest rates to attract foreign investors, have relatively limited tax bases, and frequently have weaker currencies.

The World Bank has warned that the high borrowing costs seen due to a strong US dollar and high global interest rates have drastically increased the need for untenable growth numbers in the bottom 75% of economies. Currently, 13 low-income countries and 23 middle-income countries are at high risk of or have already slipped into debt distress, with payments on debt crippling the budget.

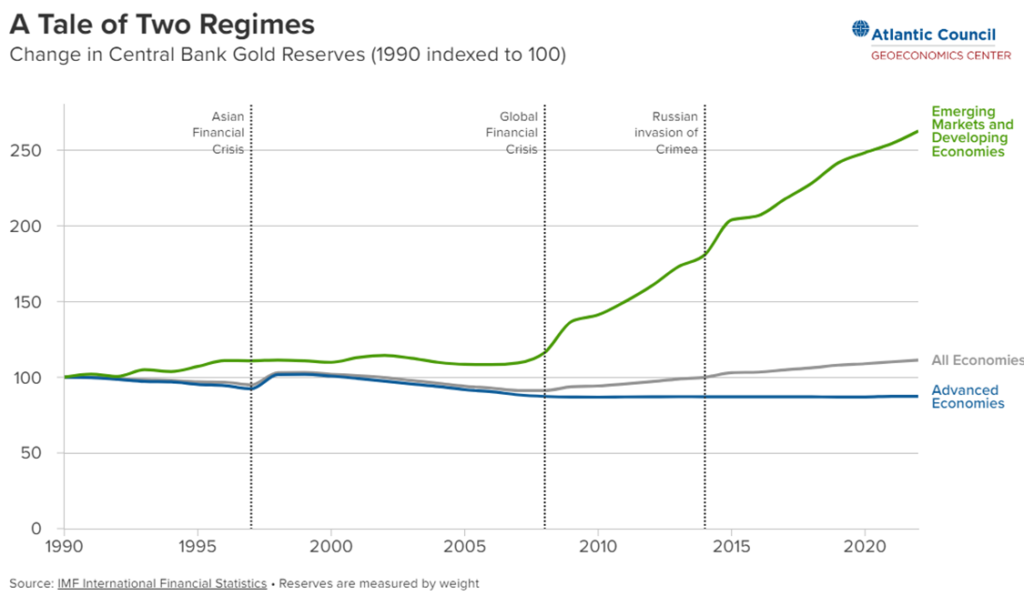

As discussed in our gold article, the strong US dollar, high global inflation, and sanctions have driven away many developing central banks from US Treasuries. Many of these have replaced purchases of US bonds with gold, which has seen record high prices in March.

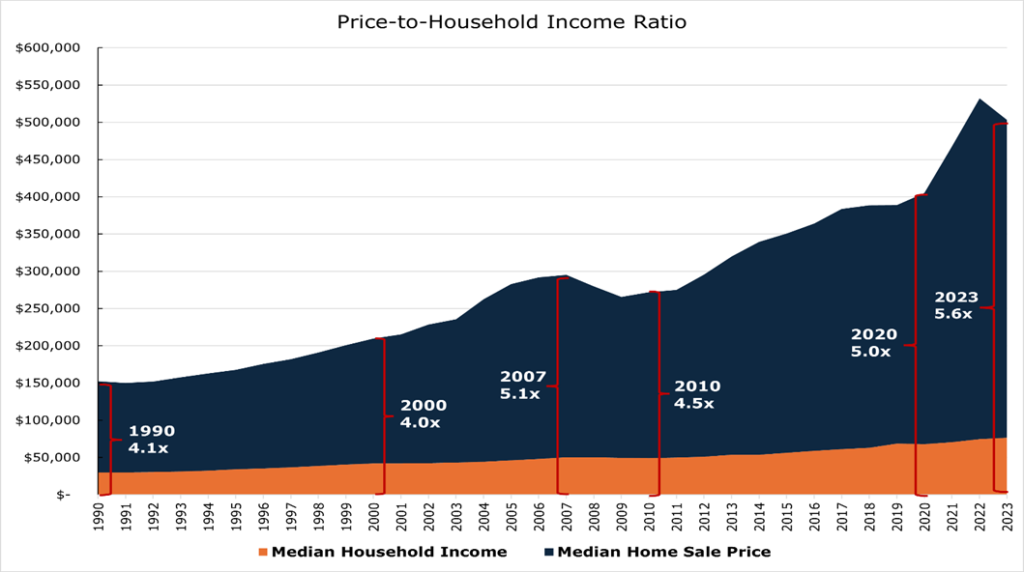

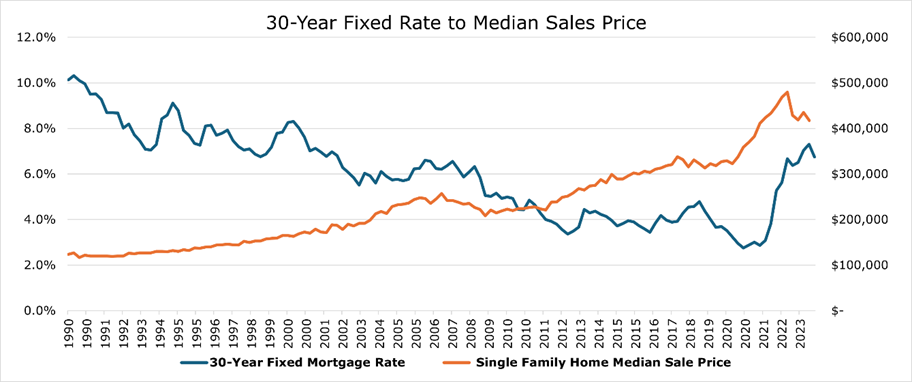

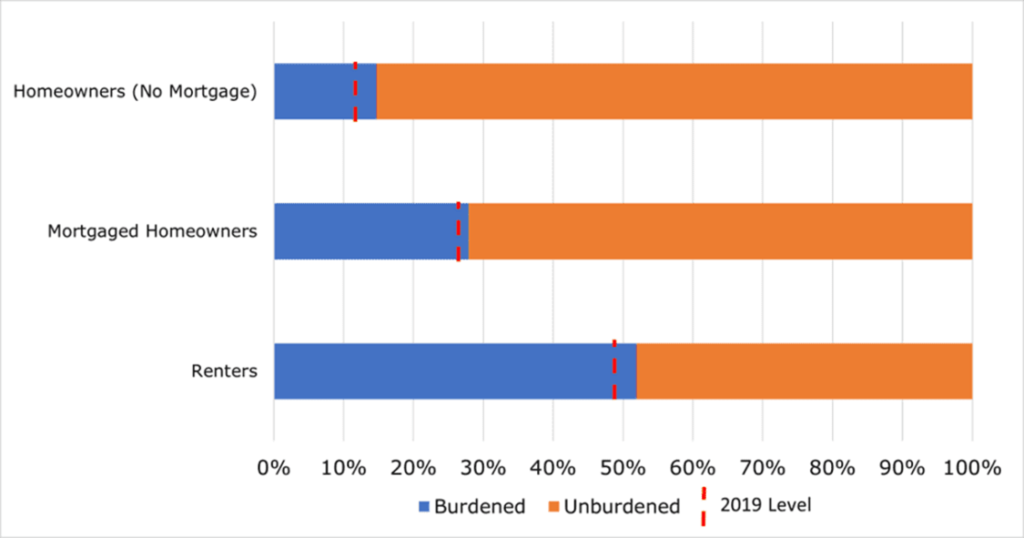

Home Price-to-Household Income Ratio Highest Level Ever

At the end of 2023, the price-to-household income ratio was at a record high of 5.6x, significantly elevated compared to the pre-pandemic 20-year average of 4.5x. A mixture of low-interest rates, low construction, and high demand drove rapid, short-term change.

With high-interest rates increasing mortgage payments, the average home price in the US has fallen for the first time since 2022.

According to Freddie Mac, the average rate for a 30-year fixed mortgage hit 6.94% in March, above the 20-year pre-pandemic average of 6.17% and near the pre-financial crisis average of 7.3%.

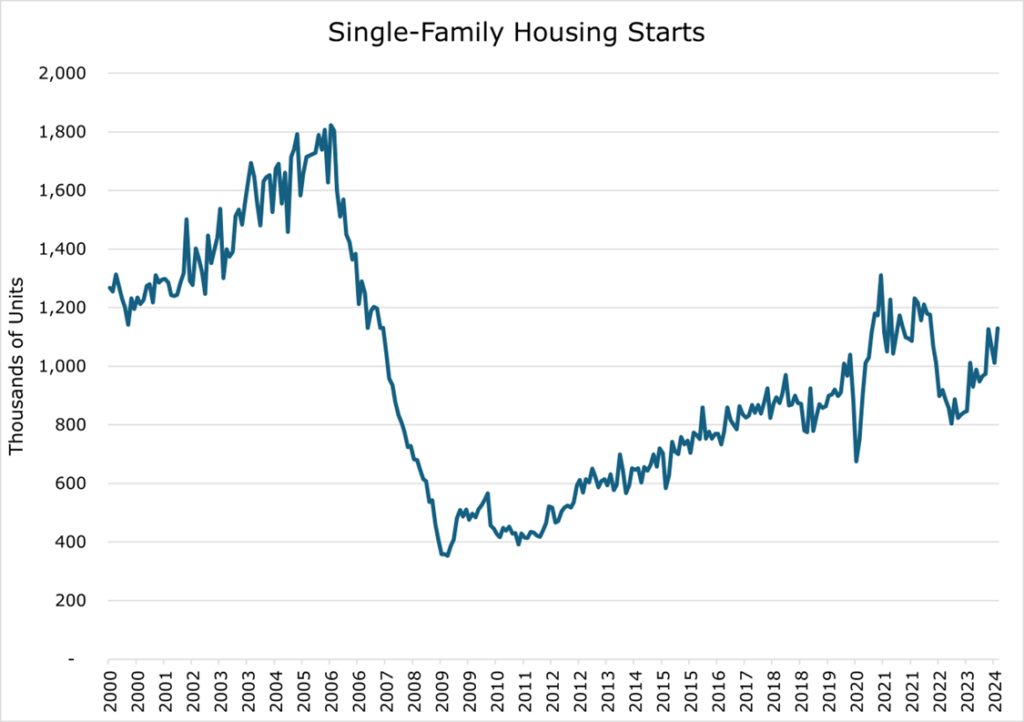

The Department of Commerce is reporting that new home starts are beginning to see improvement after a slump in 2022 and early 2023. Housing Completions hit a 17-year high, indicating that downward pressure on home prices may continue.

While the speculative part of the housing market has likely rolled over with high mortgage rates, supply remains inadequate compared to demand, which could significantly hamper economic growth. When housing costs begin to exceed a significant portion of household income, families begin to cut back on other expenditures, which can draw down consumer spending.

The impact of high housing costs has been one of the key drivers of localized labor shortages in hot markets like San Fransisco or New York City, with surveys of Labor Union members reporting housing costs as their member’s biggest issues.

Is Chocolate the First Climate Commodity Casualty?

As climate change continues to impact weather patterns around the globe, equatorial cash crops such as cocoa and coffee are facing significant challenges that could lead to substantial price increases.

The majority of the world’s cocoa crop grows in Western Africa, with 70% of the crop coming from small non-industrial farmers. These farmers already struggle with cocoa blight, which can eliminate as much as 20% of their crop on average. The 2023-2024 season was far worse than typical, with most of the cocoa regions in the world seeing some of the wettest weather in a generation. This caused a dramatic decrease in yields, with cocoa hitting more than $10,000/metric ton for the first time.

The Ghanaian Cocoa Commodity Board has announced an expected yield of around 425 kMT (thousands of metric tons), a 22-year low and an almost 50% drop from the initial forecast. The ICCO (International Cocoa Organization) predicts that the global cocoa deficit for the 2023-24 season will widen to 374,000 MT from 74,000 MT in the previous season.

The World Bank is projecting coffee to share a similar but less drastic fate in the near term, with Southeast Asian suppliers grappling with similar crop-yield problems. The Vietnam Coffee Association projects a 20% year-over-year decline in coffee exports for the 2023-24 season due to extended droughts. However, South American producers have made up the shortfalls from Asia with a narrow surplus in the coffee market.

Conclusion

In conclusion, 2024 is turning out to be the “year of uncertainty.” In our view, Europe’s economic contractions have bottomed out, and will see a slow recovery in 2024. In the developing world, India is booming, with China’s contraction bottoming out and likely headed toward economic recovery. While the final drawdown of pandemic-era savings at hand could reduce US inflation below the sticky 3% level as consumer spending rolls over, it may equally contract GDP growth before the Fed conducts its first rate cut, expected in June or later.