Hasbro’s 6.1% Dividend Yield Pays as We Wait for Recovery

| Price $46.41 | Core Holding | December 1, 2023 |

- 6.13% Dividend Yield.

- The company is undergoing major restructuring to focus on its core brands, offload the costly entertainment segment, and implement cost-saving measures.

- The company aims to save $220 million annually by the end of 2023, increasing to $300 million by 2024, by reducing its workforce and offloading non-core divisions.

- The Wizards of the Coast and Digital Gaming segment shows robust growth and high margins, now constituting 30% of Hasbro’s revenue.

- The Consumer Products segment faces challenges due to the macroeconomic environment but contains high-selling brands like Transformers.

Investment Thesis

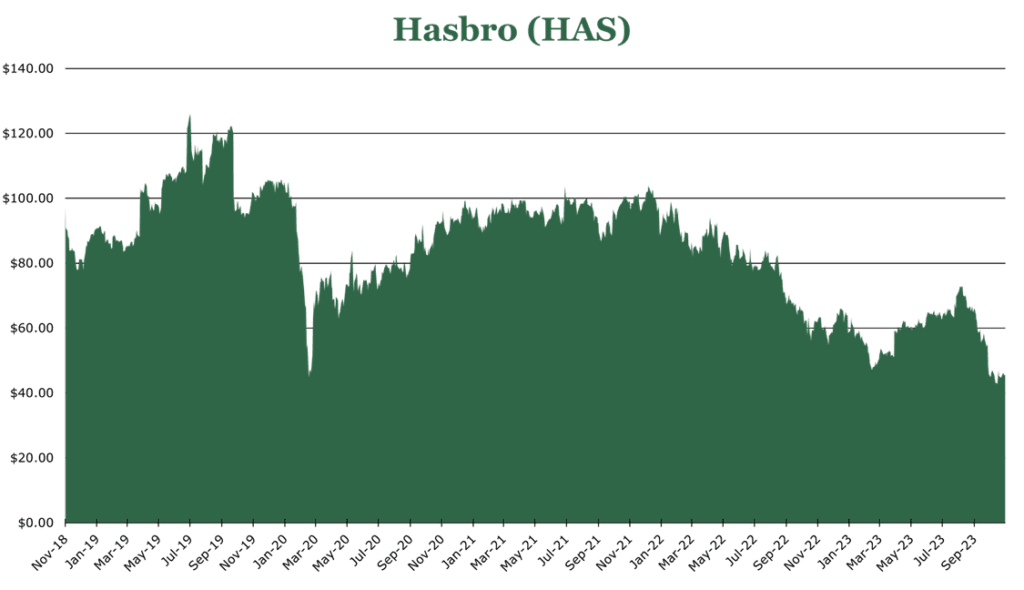

Hasbro (HAS) is a multinational toy and game company selling products in 35 countries. Hasbro is down 57% from its high of $107.52 in July of 2019. We believe Hasbro is oversold and represents strong recovery potential and a big secure dividend while we wait.

Hasbro’s brand portfolio boasts globally recognized brands such as Magic: The Gathering, Dungeons & Dragons, Nerf, Peppa Pig, Play-Doh, and Transformers. The stock currently trades at a significant discount to our estimate of fair value. Given the low valuation and long-term growth potential, we believe the stock is attractive for dividend investors.

Hasbro is streamlining to focus on its core brands’ growth potential and unlock their value. With the hemorrhaging Entertainment segment being offloaded and significant administrative cost-saving actions, Hasbro is poised for a strong recovery that is not priced into the stock in our opinion.

Estimated Fair Value

EFV (Estimated Fair Value) = E25 EPS (Earnings Per Share) times PE (Price/EPS)

EFV = E25 EPS X P/E = $4.80 X 16.3 = $78

| E2024 | E2025 | E2026 | |

| Price-to-Sales | 1.2 | 1.1 | 1.0 |

| Price-to-Earnings | 11.3 | 9.5 | 7.4 |

Divestitures and Transformation

Hasbro entered the entertainment area through its acquisition of eOne in 2020. The $4 billion purchase yielded immediate topline revenue gains. However, the business was incredibly costly to operate, with almost $600 million per year in production costs alone. Additionally, it required Hasbro to carry significant risk on its books while shows were in production. The final nail in the coffin was almost certainly the SAG-AFTRA strike, halting production across the industry and hitting Hasbro with a 40% reduction in segment revenue year over year in the September quarter.

The divestiture, valued at $500 million, will not mean losing access to high-paying intellectual properties like Peppa Pig. Instead, Hasbro will license production, allowing for a more asset-light approach and lower costs.

This is part of a broader “Blueprint 2.0” or “Fewer, Bigger Better,” seeking to shift the company to areas where Hasbro has fewer but larger brands. The chosen brands are Magic: The Gathering, Dungeons & Dragons, Nerf, Peppa Pig, Play-Doh, Hasbro Gaming, and Transformers.

These brands saw 8% year-over-year revenue increases while the rest of the portfolio performed weakly. A similar trimming will likely go on within the company’s licensed area once contracts expire, with Hasbro naming the Disney brands of Star Wars and Marvel as key partners it wants to continue to license.

| Brand | Description | Revenue as a % of Total (September quarter, 2023) | % Change Year over Year |

| Franchise Brands | Core Portfolio: Magic, D&D, Nerf, Peppa Pig, Play-Doh, and Transformers | 67.2% | 8% |

| Partner Brands | Star Wars, Marvel, other Licensed Brands | 15.2% | -35% |

| Portfolio Brands | Non-core brands: GI Joe, My Little Pony, etc | 11.3% | -19% |

| Non-Hasbro Branded Film and TV | eOne Acquired Brands | 6.2% | -47% |

The savings portion of the plan is set to deliver a total of $220 million in annualized savings by the end of fiscal 2023, realizing a total of $300 million by the end of fiscal 2024. To get there, Hasbro eliminated roughly 15% of global employees and offloaded inventory of non-core items. The plan’s ultimate goal is to increase the operating profit margin to 20% by 2027, or an 870bps increase from the September quarter of 2023. Management does not expect meaningful bottom-line yield from this plan this year but expects some bottom-line growth in fiscal 2024.

Consumer Products and Wizards of the Coast and Digital Gaming

The Wizards of the Coast and Digital Gaming segment contains all the video games and Magic the Gathering IPs. This area saw strong growth driven by the licensed gaming revenue area and the release of Baldur’s Gate III, a Dungeons & Dragons IP. Net revenues for the segment grew by 40% year over year, with the Dungeons & Dragons IP growing at over 100% year over year. On a macro level, the gaming and tabletop business typically has a longer revenue tail than other Hasbro products and appeals to a more age-diverse audience.

| Revenue as a % of Segment Total (September quarter, 2023) | % Change Year over Year | |

| Table Top Gaming | 68.6% | 18% |

| Digital Gaming | 31.4% | 133% |

The segment has high margins at 48% operating margin, which increased significantly by 1430bps year over year. This segment now makes up just under 30% of total revenue. While we believe that the core of the business will remain the Consumer Products segment, the Wizards of the Coast and Digital Gaming segment will provide an important buoy for repositioning efforts.

The core of the Hasbro business is the Consumer Products segment, anchored by GI Joe, Transformers, Furby, and Playdoh. The macroeconomic environment has stressed this segment, with revenues decreasing by 18% year over year. On a real basis, about 12% of this decrease is attributed to volume loss.

The direct-to-consumer platform Hasbro Pulse is a particular growth avenue for this segment. While currently in the early stages of expansion, sales grew 57% year over year through this channel. Specific results are not broken out, but the Blueprint 2.0 strategy calls for $1 billion in yearly sales by 2027 in the combined Direct-to-consumer and Digital areas. The Consumer Products segment typically sells products wholesale to retailers, and this extension into direct-to-consumer could improve margins as it grows.

As part of the previously discussed Blueprint 2.0 plan, around $50 million worth of inventory will be offloaded on a heavy discount, which will be a headwind for profitability for the segment for the remainder of the year. Management expects this to translate to a slight boost in fiscal 2024 as retailers re-stock on newer Hasbro products. Additionally, the next priority for cost savings is in the manufacturing area, while fiscal 2023 efforts have thus far been focused on the supply chain.

| Revenue as a % of Total (September quarter, 2023) | % Change Year over Year | |

| Consumer Products | 63.6% | -18% |

| Wizards of the Coast and Digital Gaming | 28.2% | 40% |

| Entertainment | 8.2% | -42% |

Risk

Determining which brands to focus on is key to executing Blueprint 2.0. While the selected brands saw 8% year-over-year growth, consumer preferences change over time, and consumer tastes can change quickly. Continuing partnerships and innovation to develop new products is critical to Hasbro’s operations, with Disney being a key partner. The loss of the Disney partnership or putting money into the wrong brand could spell additional financial hardship.

We expect overall consumer spending to slow, as detailed in our article here. While the timing or intensity of this reduction is unknown, Black Friday this year was a record-breaker but contained lots of discounting. In our opinion, this headwind will be a drag on Hasbro’s recovery.

Outlook

On a shareholder return basis, we expect repurchases to remain minimal. In the first 9 months of 2023, Hasbro repurchased no shares despite having $241.6 million in available repurchases. However, it maintained its annualized dividend of $2.80 per share or a 6.13% yield. We believe the dividend is safe at its current level, and we do not expect meaningful repurchase activity until the second half of 2024.

Current debt is $3.6 billion, with a debt to EBITDA of 2.6x which is down slightly from record highs. However, with the offloading of the entertainment sector, around $125 million in production loans will be removed, and the $375 million in net proceeds will pay off the debt tranches with the highest interest.

Altogether, the capital priorities are to finish the cost savings and repositioning program, delever the balance sheet to improve credit rating, and maintain the dividend at its current level.

Despite significant short-term challenges, the steps toward a turnaround are in place. Management is taking active steps to unlock the potential of its block-busting brand portfolio and name recognition. The stock now trades at a steep discount as it trades at an almost 10-year low. Its strategy is expected to begin yielding bottom-line results in fiscal 2024, and in our view, it is a buy at its current level. In summary, Hasbro’s powerhouse of brands, strategic focus, and current market valuation make it an attractive proposition for investors seeking growth potential in a well-established company while earning a high dividend.

Competitive Comparisons