Global Leader in Gold Seeks To Dig Out Copper Niche

| Price $39.71 | Dividend Holding | January 4, 2023 |

- 4% projected dividend yield for 2024.

- Gold prices should benefit from economic instability, persistent inflation, deficit spending, high debt, and a global move away from the dollar.

- Newmont is the world’s top gold producer, annually outputting 5.3 million ounces of gold and significant quantities of silver, copper, zinc, and lead.

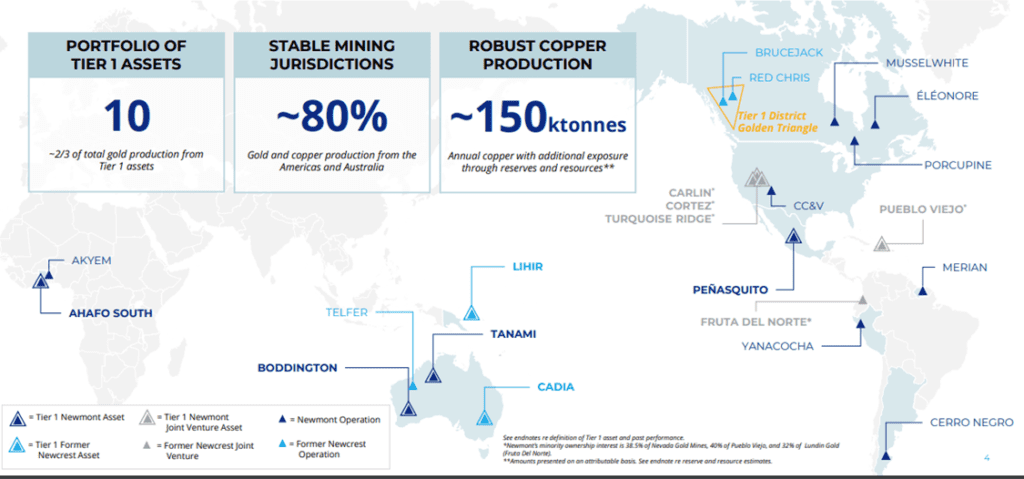

- NEM’s main production assets are strategically located in politically stable regions.

- NEM benefits significantly from gold price increases, adding $400 million in annual free cash flow for every $100/oz rise in gold prices.

- The major acquisition of Newcrest closed in November, significantly expanding the gold and copper asset base.

Investment Thesis

Newmont Corporation (NEM) is the #1 gold producer globally, outputting 5.3Moz (million ounces) of gold per year, 35oz of silver, 100Mlbs of copper, and various other byproduct metals, including zinc and lead. The total GEO production (gold equivalent ounce) is over 7 million ounces. NEM has one of the longest production profiles in the industry, with current production being maintained until at least 2032.

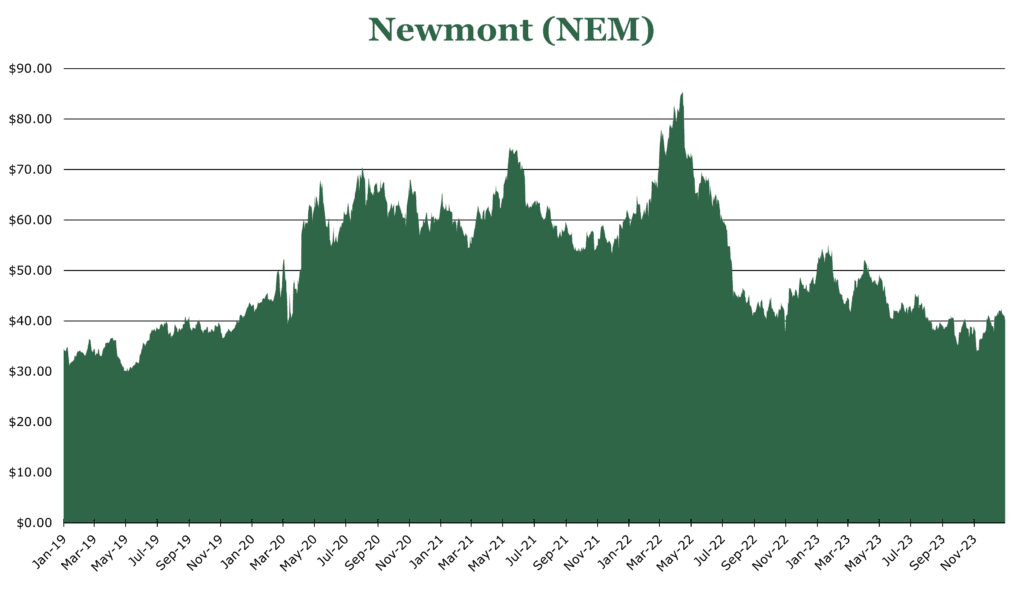

NEM’s main production operations are in more politically stable locations in Canada and Australia. NEM’s price has fallen by over 50% since its 2022 peak of over $80 per share, giving the current entry near the 5-year lows. For every $100/oz gold increase, NEM adds $400 million per year in free cash flow. With gold prices experiencing long-term tailwinds that support a sustained price level, coupled with a leading production profile and metal diversification, NEM represents a stable dividend income investment and potential for capital appreciation.

Estimated Fair Value

EFV (Estimated Fair Value) = E25 EPS (Earnings Per Share) times P/E (Price/EPS)

EFV = E25 EPS X P/E = $3.10 X 18 = $55.80

| E2024 | E2025 | E2026 | |

| Price-to-Sales | 4.0 | 2.7 | 2.6 |

| Price-to-Earnings | 17 | 15 | 13 |

Portfolio Overview

| Quarter ending September | AISC (all-in sustaining costs) ($/Oz) | Production (Gold Equivalent kOz) |

| North America | $1,712 | 507 |

| Central and South America | $1,438 | 71 |

| Australia/Pacific | $1,006 | 304 |

| Africa | $1,270 | 208 |

| Total | $1,426 | 1260 |

Company-wide operations for the full year 2023 are expected to be 5.3Moz of gold production, with 100Mlbs of copper production, 15Moz of silver, 100Mlbs of lead, and 230Mlbs of zinc. Average AISC (all-in sustaining costs) are expected to be in the $1,426/oz range.

North American production increased by 3.7%, but AISC increased by 15.5%. Cost increases in the area were largely inflationary, but the average assets are older in North America, meaning higher sustaining costs to access deeper or more difficult deposits of gold.

Central and South American production decreased by 71.5%, with an increase in AISC of 20.2%. The strike at the Peñasquito mine significantly impacted South American operations. Excluding this, production increased marginally due to higher recovery at Cerro Negro. Cost increases were inflationary and were not meaningfully above what was expected.

Australia/Pacific saw a 2.7% increase in production, with only a 4.5% increase in AISC. At the Boddington mine in Australia, gold production was in line with the prior year, but there was a 39% increase in the production of other metals, mostly copper. We expect improvements in production into 2024 as the waste processing plant allows for higher extraction rates from ore.

Africa saw a production decrease of 18.1%, with an AISC increase of 21.5%. This was due to a temporary closure in Akyem, where a road needed to be reinforced. Additionally, in Ahafo South, a large custom-tooled gear for the mill was damaged, requiring the mill to operate at limited capacity. NEM estimates a return to full capacity in the first half of 2024.

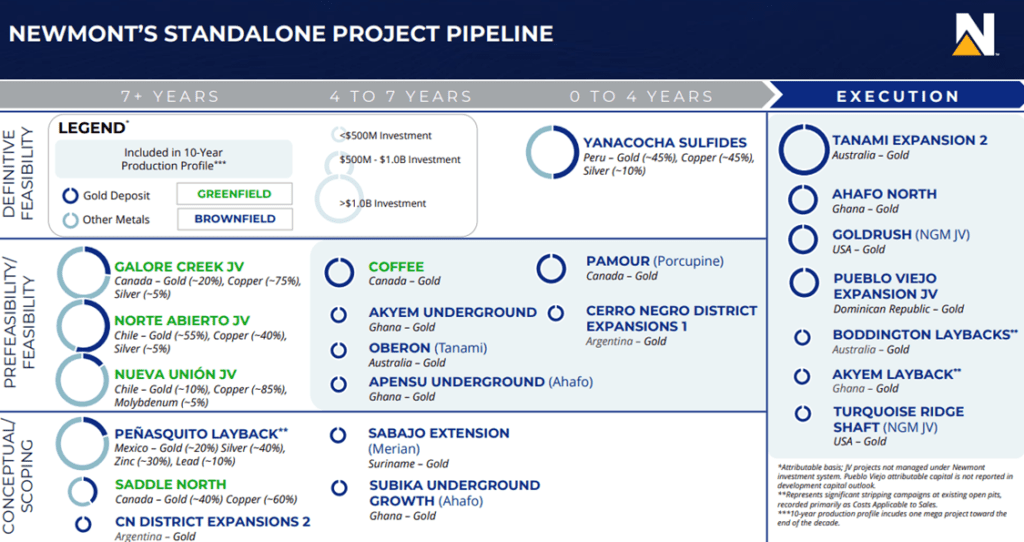

Expansion

Expansion is still strong with this mature mining operation. In the short term, NEM will largely continue to focus on gold. However, many of the projects in the latter half of the decade have significant deposits of copper. The shift toward copper production directly responds to the global energy transition. Copper is a key metal in producing electrical components, and demand is still higher than supply. McKinsey estimates copper demand will balloon by 46% by 2031, with supply running short by 6.5 million metric tons. Additionally, S&P states that around 60% of global copper is sourced from countries with unstable geopolitical situations, making the Australian production profile of NEM particularly attractive.

The $16.8 billion buyout of Newcrest Mining closed in November of 2023. First announced in March 2023, the transaction will add ~2.2Moz of gold production and 280Mlbs of copper production. Newcrest also has a significant reserve profile, which will significantly expand NEM’s asset base and grant NEM control of more than half of the world’s tier 1 gold deposits. By the end of 2025, the combined entity will be expected to save at least $300 million through integrating Newcrest assets with NEM’s management and supply chain.

Short-term gold expansion includes two major expansions to existing operations at Tanami in Australia and Ahafo in Ghana. Longer-term expansion includes life expansions at Porcupine, Cerro Negro, and a Sulfide extraction in Peru.

The Tanami expansion is expected to add an estimated 175koz in annual production, with a mine life extension to 2040. Additionally, this expansion will not meaningfully increase AISC, allowing for a significantly improved production profile. Full estimated costs are expected to be $1.2 billion, with approximately $600 million left to spend until completion.

Ahafo North expansion will utilize existing infrastructure for the Ahafo South mine, allowing a 13-year aggregate life expansion with 300koz of additional production. This expansion would bring down the average AISC, with initial estimates putting the expansion at $850/oz compared to Ahafo South’s $1,208/oz. The project is expected to cost around $1 billion, with $600 million in estimated costs left.

The most significant long-term project is a trimetallic (45% gold, 45% copper, 10% silver) mine near existing operations in Peru. Initial estimates put output at 525,000kGEO (thousands of gold equivalent ounces), with output well past 2040. The mine is a refractory deposit, meaning it is contained within rocks resistant to the traditional chemical process. This requires more capital-intensive extraction but generally yields a higher grade. Initial earmarking of funds has been delayed until the end of 2025 after digesting the Newcrest acquisition with integration and divestitures.

Risk

Mining is unpredictable, with many surprises across a breadth of risks: labor, regulatory, costs, mine quality, pricing, and weather.

Most of NEM’s operations are in geographically stable regions of the world. Around 80% of NEM’s total copper and gold production comes from the Americas and Australia. While these regions typically have higher AISC, geopolitical instability is a non-issue. However, NEM did experience labor disputes during the quarter ending September, with the Peñasquito being non-producing for the entire quarter. This mine was re-opened in mid-October 2023 with a raise for workers.

The acquisition of Newcrest has likely prevented NEM’s stock price from increasing with gold prices. The $19 billion price tag is high, even for a company as strong as NEM. There is skepticism within the market on whether mergers in the gold mining area will ever recover their cost basis. This, coupled with weak results in the second half of 2023, has sustained the dip in price. We believe that the whole is worth more than the sum of its parts and that NEM is in an excellent position going into 2024 and especially 2025.

Outlook

The full year 2023 is expected to be weaker due to broader economic conditions and the labor action at the Peñasquito mine. However, the year’s final quarter is expected to be the strongest, which we believe will carry momentum into next year.

| Quarter ending September | Year over Year Change |

| Production (excluding royalties) | -11.8% |

| Revenue (excluding royalties) | -5.3% |

| AISC (all-in sustaining costs) | 12.2% |

Most of the production and non-inflationary cost headwinds will be alleviated by the first half of 2024. The balance sheet will significantly benefit from the planned divestitures and potentially support a significant dividend.

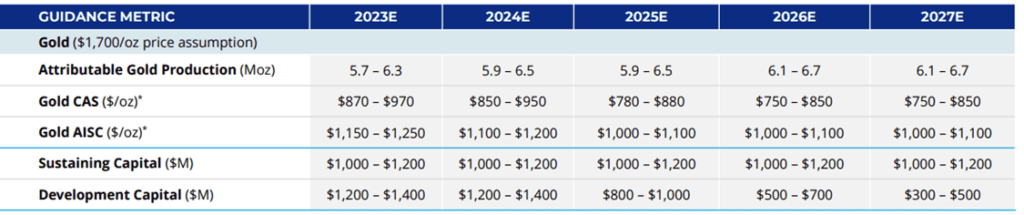

Over the 5 year horizon, NEM expects AISC to decrease back to the $1,100 neighborhood while production is expected to increase meaningfully by the end of the range. Annual average capex spend is around $2.5 billion per year, concentrated at the beginning of the range.

The dividend is paid as a base of $1.00/share, with a variable paid out as a percentage of incremental free cash flow. This currently results in a yield of 4%. With gold prices sustaining price levels at or above $2,000/oz, NEM could pay as high as $2.00/share in 2024, though we believe $180 is a more realistic estimate, bringing the yield to 4.5%. There are significant secular tailwinds for gold, which we discuss in our article on the modern gold market. Gold reached a historic all-time high of $2,122/oz on December 3. Gold has been a historically stable value asset, one of the few options now that Treasuries have fallen out of favor internationally, hinting at its potential to sustain high prices. During the quarter ending September, NEM realized an average gold price of $1,920/oz, representing a significant moat compared to AISC.

With $3.1 billion in cash on hand, $397 million in quarterly free cash, and 0.8x debt to EBITDA, NEM is in a very safe position in the gold sector. Fitch assigns it a rating of A-, making it one of the top-rated mining firms in the world. Newmont has continued to deliver cost savings wherever possible, with the Full Potential program initially beginning as a $400 million cost-saving program in 2019, growing to $1 billion in annual savings, and continuing into 2024 with acquired assets. NEM estimates that there is $200 million in additional savings to unlock with Newcrest assets by following the program.

NEM has announced its intention to sell approximately $2 billion of assets and further focus on the development of copper. This large-scale offloading will occur by the end of 2025 and will likely concentrate on tier-2 operations without development potential. According to the Wall Street Journal, the most likely divestitures are Cripple Creek and Victor gold mines (often referred to by Newmont as CC&V), with other mines in Canada, Australia, and Ghana under consideration for sale. The cash resulting from these sales will go to strengthening the balance sheet.

In conclusion, Newmont Corporation stands as a key player in the global mining industry, not just as the leading producer of gold but also as a growing player in copper. Newmont’s focus on operational efficiency and cost management while continuing to invest in growth opportunities demonstrates a balanced approach to creating shareholder value and strengthening its market position.

Competitive Comparisons