Volkswagen’s High Yield Backed By Undervalued Brand Portfolio

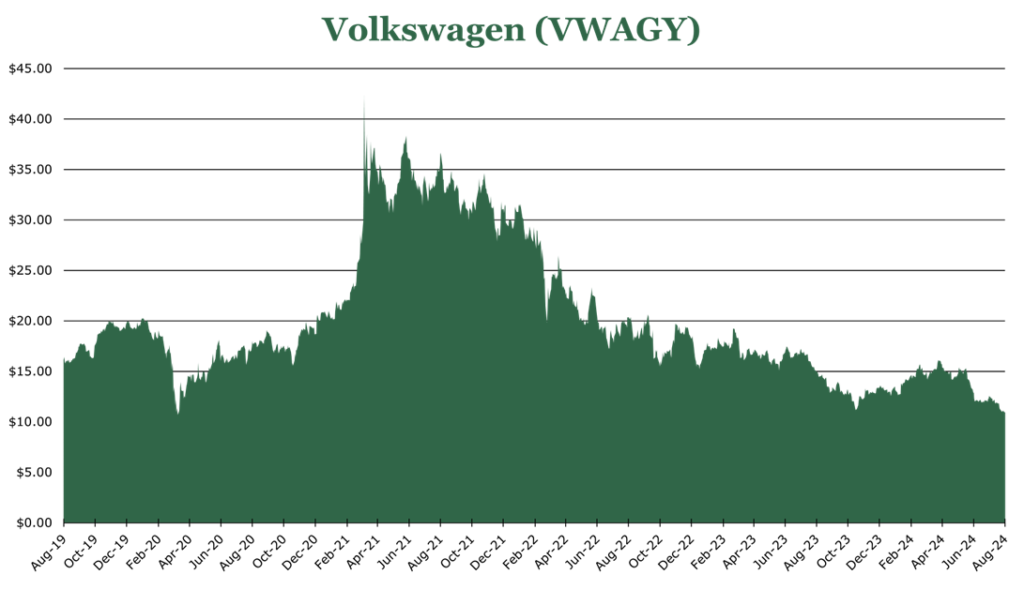

| Price $10.92 (VWAGY) €92.94 (VOW3) | Core Holding | August 15, 2024 |

- 8.9% Dividend Yield.

- Powerful brands including Audi, Lamborghini, Bentley, and majority ownership in Porsche.

- New EV JVs to reduce capital costs, with Rivian for global EVs and Xpeng for Chinese-made EVs.

- Cost savings program targeting $11 billion in total savings by 2026.

- 11% market share, second in the world with 9.24 million vehicles delivered in 2023.

- Low valuation relative to peers, trading at just 3.1x earnings.

1 EUR = 1.09 USD

Investment Thesis

Volkswagen (VWAGY 1/10 ADR, trades in Europe on XETR as VOW3) is a German automotive giant, encompassing more than 10 vehicle brands, including VW, Audi, Lamborghini, Bently, and several European brands like Skoda. During 2023, Volkswagen delivered 9.24 million vehicles in 153 countries.

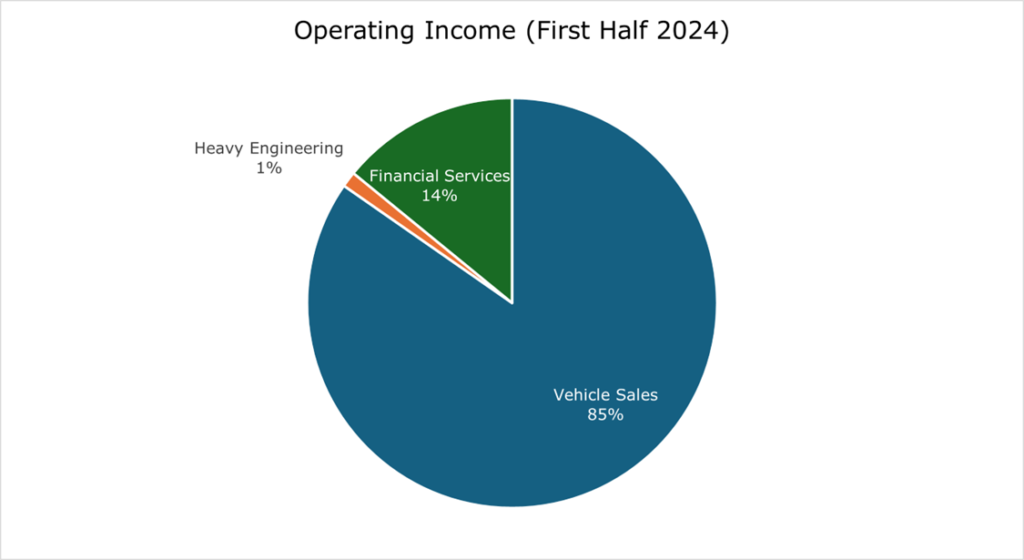

Additionally, Volkswagen holds significant ownership in the publicly traded Porsche and Traton. Together, these investments represent around $8.79/share of value, or more than 80% of Volkswagen’s current price. As of the half year ending June 2024, these companies represent 25% of sales and 53.7% of Volkswagen’s operating income. We believe that these holdings are underpriced by the market.

| Brand | % Ownership | Asset Value ($ Billions) | Value per VWAGY share |

| Porsche | 75.80% | $28.5 | $5.69 |

| Traton | 89.72% | $15.5 | $3.10 |

Despite having a substantial portfolio of recognizable brands and the second highest market share in the world at 11%, Volkswagen trails behind its peers in market value. Though Volkswagen is experiencing some margin compression due to the broader macroeconomic climate, it still pays out a peer-leading 8.9% dividend yield backed by a strong globally recognized brand portfolio. Thus, we believe that Volkswagen’s leadership position offers a strong dividend yield at an attractive valuation.

Estimated Fair Value

EFV (Estimated Fair Value) = EFY25 EPS (Earnings Per Share) times P/E (Price/EPS)

EFV = E25 EPS X P/E = $6.0 X 5.0 = $30.00 (VWAGY)

| E2024 | E2025 | E2026 | |

| Price-to-Sales | 0.14 | 0.14 | 0.14 |

| Price-to-Earnings | 3.14 | 2.08 | 1.79 |

Market Conditions

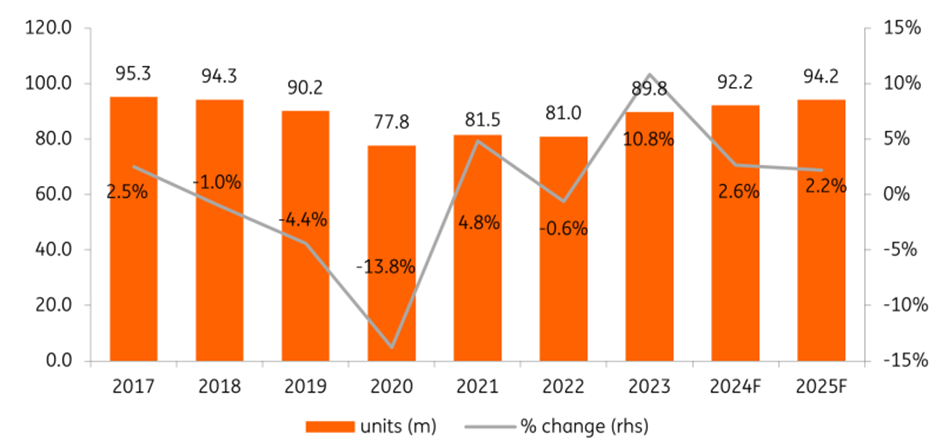

The global market for automobiles is expected to marginally slow in 2024 compared to the 10.8% growth seen in 2023. Over the next two years, ING expects automotive volumes to only grow by 2.6% year over year in 2024, and 2.2% in 2025. Though Volkswagen reported stronger growth in the first 6 months of 2024 compared to the first 6 months of 2023, the ransomware attack at North American auto dealers and remaining uncertainty around when rates would come down have weighed down expectations.

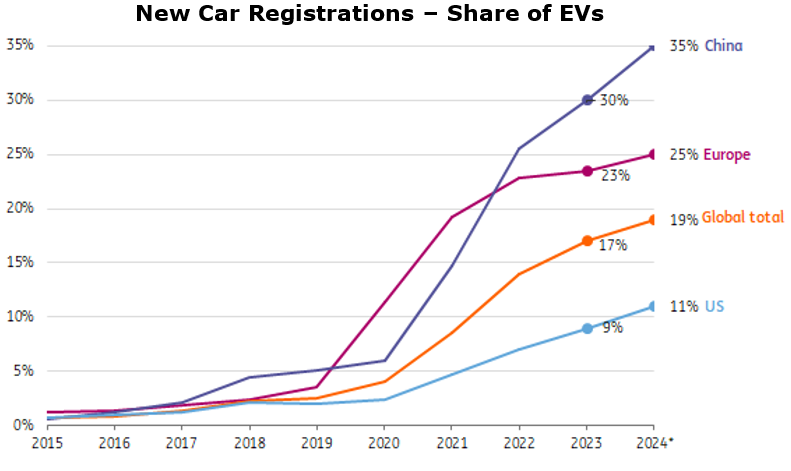

The overall slowdown in the automotive market will have an outsized impact on the transition to EVs.

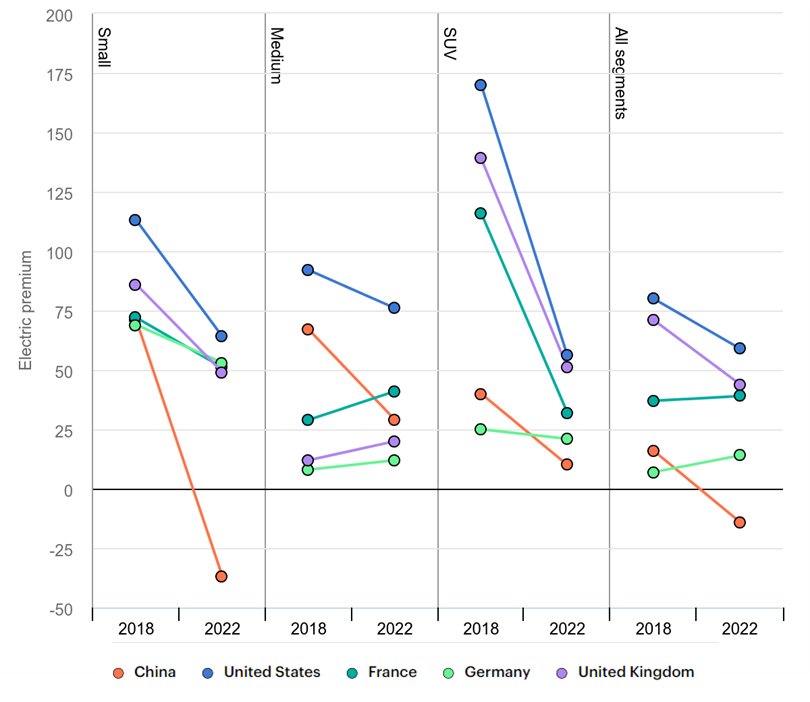

The dynamics of purchasing in the EV market are quite different from typical ICE vehicles, with a higher percentage of consumers financing EVs, and EVs having a lower resale value compared to an ICE vehicle. The premium charged on EVs has begun to fall, though in the US the premium is still 59% over a typical ICE vehicle. Overall, the aggregate effect is individuals and fleet customers alike slowing their purchases of EVs. Individuals are waiting for cheaper and better vehicles in the face of very-low resale values and limited on-the-go charging opportunities despite the hefty premium. Fleet customers, specifically rental companies, are selling off their existing EV fleets due to limited range and limited charging options, which severely restrict customer use.

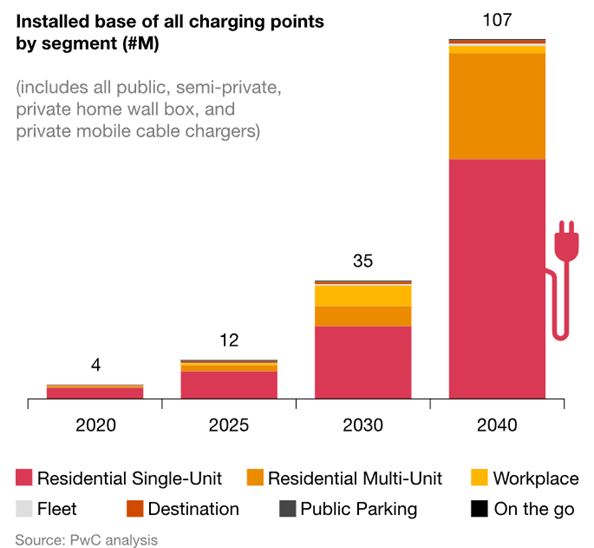

Largely, consumers still rely on public charging infrastructure for EVs. While the US government has put forward $7.5 billion to expand the architecture, with similar spends around the world, growth in public charging infrastructure has lagged substantially relative to spending. In the US, the geographic distribution of public EV charging stations is highly skewed leaving out much of middle America leaving home charging as the only option for many.

Overall, we feel that the manufacturing side of the transition to EVs has outpaced the consumer demand for those vehicles. For now, ICE vehicles will likely remain dominant outside of Europe and China. Over the long-term, we remain unsure if EVs will ever catch on to the extent outlined in various automaker and government plans.

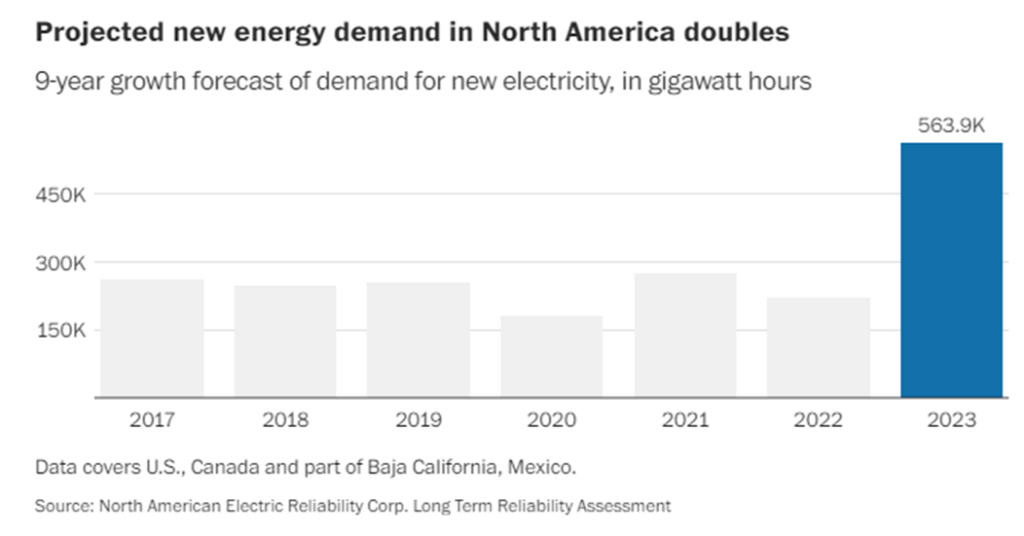

This is both due to the previously mentioned consumer issues and the load on the grid generated by economy-wide electrification, retirement of fossil fuel generators without sufficient replacement, and datacenter growth. The rolling 9-year forward forecast for electricity demand doubled in a single year.

Volkswagen is re-allocating capital more toward ICE (internal combustion engine) development. This represents $65.5 billion in new ICE investment, or around 36% of the projected capital spend to 2028. Initially, all vehicles under the Volkswagen group were supposed to be all-electric by 2033, but Volkswagen is certainly not the first to re-amp spending in ICE and take a more vague stance on the future of EVs, with Ford and Mercedes both also committing to longer-term ICE support.

Core Business

Volkswagen includes several international brands, delivering just shy of 4.4 million vehicles in the first half of 2024, accounting for an 11% global market share. Compared to the first half of 2023, deliveries were down 0.6% across the whole company, of which 0.2% was passenger. Volkswagen attributes this to an overall reduction in demand for EVs on the passenger side and overall lower demand in the commercial area due to macroeconomic conditions.

| First Half 2024, Flagship Brands | |||||

| Brand | Description | VWAGY Share | Deliveries (thousands of vehicles) | Operating Margin | % of Total Revenues |

| Traton (Scania, MAN, Navistar) | Commercial | 89.7% | 161 | 11.0% | 14.3% |

| Progressive Brand Group (Audi, Lamborghini, Ducati, Bentley) | Premium Vehicle | 100% | 539 | 6.4% | 19.5% |

| Core Brand Group (VW, Skoda, SEAT) | Light Vehicle | 100% | 2,494 | 5.0% | 43.5% |

| Sport Luxury (Porsche) | Premium Vehicle | 75.8% | 152 | 16.4% | 11.1% |

| Chinese Operations | Light Vehicle | Varies | 1,265 | N/A | 0.5% |

Overall, as previously discussed, market conditions have pushed down consumer spending on large purchases. We feel that this will continue until global interest rates begin to move down more substantially in the second half of 2025.

Overall, the core of the business is rock-solid. In the short term we believe that it is for the best that Volkswagen is renewing ICE spending and is taking a more long-term approach to EVs through partnerships and steady organic market growth rather than trying to push for an all-EV fleet by the end of the decade.

Rivian Partnership and EVs

In July 2024, Volkswagen said it would invest as much as $5 billion into Rivian, with an initial commitment of $1 billion. The first step is a $1 billion investment into Rivian with a convertible note that will convert into Rivian common stock upon regulatory approval. The second $1 billion will come upon regulatory approval and be allocated toward the 50-50 JV. If Rivian meets certain financial and technological targets, these targets are not yet public, it will qualify for $2 billion more in investment in its stock from Volkswagen, and an additional $1 billion loan for the JV past 2026. Provided Rivian hits all targets and the JV is approved, at current prices and market cap, Volkswagen would own approximately 22.7% ($0.60 per VWAGY share of value) of Rivian at the end of 2026.

The 50-50 JV will work to create both EV architecture and associated software suites that work across both firm’s vehicles, acting as a standard. The completion of the JV’s run up is expected in the final quarter of 2024 with full benefits realized by the end of the decade.

Rivian, despite it remaining unprofitable, has been a key innovator in the premium EV market. Rivian has managed to reduce both its required suppliers by cutting down on its required ECUs (electronic control units) by using novel zonal architecture and its proprietary software. In the context of competitors, Rivian’s only have 7 ECUs while an average ICE vehicle has between 40-150. Volkswagen has expressed a desire to implement the same zonal architecture in its vehicles to cut down on costs.

We believe that it is likely that the Rivian partnership stems from a desire to put Cariad behind Volkswagen, and substantially scale back internal spending on the segment. Cariad was Volkswagen’s attempt at an in-house software developer for its new generation of ICE vehicles and EVs and the broader trend of “software defined vehicles”. The software suite was plagued (which may be underselling it) with problems and even caused several launch delays losing Volkswagen $2.2 billion in 2022. Over the first half of the year ending June 2024, Cariad was still losing $1.2 billion.

The benefits for Volkswagen are obvious, being given access to a successful and proven electronics and software architecture will substantially reduce internal-spend on Capex, by an estimated $10.9 billion through 2029. Additionally, it may indicate a shift in Volkswagen’s EV strategy from trying to build cheap competitors to generate market share by converting ICE customers, and instead focus on premium EV offerings in the short term to take market share from competitors like Tesla.

In China for China

Recently Chinese EV maker BYD has dethroned Volkswagen as the top-selling vehicle manufacturer in China.

Largely, this is because Volkswagen vehicles still being priced at a relative premium in China compared to competitors. To combat its slipping market share and rising costs in the medium and low-end market Volkswagen has introduced a “In China for China” market plan.

This plan started with the construction of the EV-focused R&D center and plant in Hefei for $1.1 billion, which added to the already 38 facilities Volkswagen operates in China. The facility also operates as the “brain” of the In China for China strategy, which previously relied on managers in Germany at Volkswagen corporate to both procure and plan domestic Chinese production.

The new strategy will release several China-exclusive models targeted at consumer preferences in the low-middle market area, which will ideally have lower-cost procurement allowing for competitive pricing. These new models will also use the jointly developed with Xpeng architecture for EVs, with existing ICE sales in China forming the “profitable basis” by which the EV transformation will spring from. In our view, Volkswagen may be using China as a testbed for lower- and medium-end EV manufacturing and procurement. Currently the non-Chinese EV market is dominated by premium EV offerings, with little consumer demand for cheaper options, and a materials market not yet robust enough for consistently lower pricing.

Overall, the market in China for EVs is incredibly strong despite global muted demand, ING expects Chinese growth to be 3.0% compared to the US figure of 2.0% for 2024. If Volkswagen is able to successfully compete with Chinese EV makers on cost, we believe it could very easily outpace its foreign peers in the country and maintain its top spot in the market. Volkswagen is targeting $3.2 billion in attributable Chinese revenue by 2030, or around 15% overall growth in the business unit compared to 2023.

Risk

Chinese EVs and components sourced from China have become a tension point for the EU, US, and Canada with several manufacturers and governments supporting tariffs on Chinese EVs which will undoubtedly be met with countervailing tariffs on Western EVs and western manufactured parts. Ironically, this may actually be a boon for Volkswagen, provided its supply chain for Chinese-made vehicles is sufficiently insulated from its global operations. However, if the supply chain still relies on the importation of components made outside of China it could sink the “In China for China” strategy before it has the chance to get off the ground.

Financials

Volkswagen has re-emphasized its cost-cutting efforts amid margin contraction. Typically, Volkswagen’s quarterly net income margins have hovered around 5.5% but, in the quarter, ending June 2024 they moved down sharply to 3.9%. Additionally, operating margin fell to 6.3%, below the target of 7.0%.

On the operating line, Volkswagen attributed the margin contraction to unfavorable mix, and capacity going unused amid lower-than-expected consumer demand, especially in the higher-cost EV market. To combat this, Volkswagen stated that it is considering closing or retooling its Audi EV plant in Belgium, which would cost $2.8 billion up front but may lead to long-term operating margin improvement. On top of this, Volkswagen thinks it can save $11 billion by 2026 in various cost saving measures across the supply chain and other overheads, including incentivizing early retirement. Volkswagen projects that some of these items will begin to show results in the second half of the year and will end 2024 with an operating margin somewhere between 6.5-7.0%.

Capex will be cut by 8% over the 2024-2028 period compared to initial projections, and it would be shortening the R&D cycle, by around a year, to around 2 years to put new products to market quicker. This takes the aggregate spending amount to 2028 down to around $180.3 billion.

Currently Volkswagen has a BBB+ rating, and a trailing twelve-month net debt to EBITDA of 7.4x which is in line with peers. Overall, though, Volkswagen has $48.2 billion in cash on hand and an interest coverage ratio of 6.9x which indicates despite high margin, the debt is cheap at a reported 4.3% average interest.

Volkswagen targets paying out 30% of net income to shareholders, giving it a strong dividend yield of 8.9%. Though we expect overall macro headwinds will remain over the short-term, we see no reason why Volkswagen won’t continue to be at the top of the global automotive market into the EV age. Volkswagen remains a global leader in automobiles with a strong globally recognized brand portfolio at an attractive valuation and believe that its solid dividend yield and a low valuation make it a buy for investors seeking both income and capital appreciation.

Competitive Comparisons