UPS’s Huge Free Cash Backs its Leading 5.0% Dividend

| Price $131.02 | Dividend Holding | October 8, 2024 |

- 5.0% Yield.

- Offering services to enhance margin including more small-business mix and specialized medical logistics services.

- Consolidating 200 sorting centers, with the new automated counterparts offering a reported 30% efficiency improvement.

- Expects to generate $5.8 billion in free cash in 2024, adding to its already massive $6.3 billion cash position.

- Industry-leading capital efficiency, with a return on invested capital median of 27% for the last 3 years.

Investment Thesis

United Parcel Service (UPS) is an American delivery company that processes more than 20 million packages per day across its fleet of 115,000 ground vehicles and 500 aircraft. UPS is repositioning to target more SMB (Small Medium Business) customers and more specialized logistics services, specifically medical cold-chain and medical custody compliance. Additionally, it is consolidating 200 sorting locations into more heavily automated facilities.

Currently volumes are below seasonal averages due to deteriorating B2B (Business to Business) conditions, not able to be offset by continued B2C (Business to Consumer) volume growth. UPS has an industry-leading balance sheet, expecting to deliver $5.8 billion in free cash in 2024 adding to its $6.3 billion cash position, providing ample safety for its 5.0% dividend yield. Overall, we believe that UPS will recover secularly as the economy enters the upswing. In the meantime, investors can take advantage of its blue-chip yield.

Estimated Fair Value

EFV (Estimated Fair Value) = EFY25 EPS (Earnings Per Share) times P/E (Price/EPS)

EFV = E25 EPS X P/E = $9.00 X 17.6 = $158.43

UPS does trade below its own long-term P/E median of 20.9x, with the cyclicality of a lower than historical valuation. We feel that as economic conditions improve and as UPS’s pushes toward automation and higher-margin business units, the earnings power of UPS will be demonstrated, driving the price higher.

| E2024 | E2025 | E2026 | |

| Price-to-Sales | 1.2 | 1.2 | 1.1 |

| Price-to-Earnings | 17.6 | 14.7 | 12.7 |

Results

Volumes for the first half of the year ending June 2024 saw a decrease of 1.8%. UPS reported that declines were worst for B2B customers but that there was not a particular industry or customer size that made up the majority of the decline. B2C volumes were still strong, though no longer able to fully offset B2B declines.

On a per segment basis, US domestic saw average daily package volume increase marginally by 0.7% year over year for the quarter ending June 2024. On a more granular basis, UPS reported that B2B volume was down 4.6% year over year while B2C growth was still strong at 4.8% year over year. However, for the first half of 2024, total volumes were still down 1.3% in total. We feel this is due to soft economic conditions and volumes will recover with the economy.

The international segment saw volumes decline 2.9% year over year for the quarter ending June 2024. For the first half of the year this figure was 4.4%.

Finally, the supply chain segment saw overall positive results, with revenue increasing 2.6% year over year for the quarter ending June 2024, though still down 1.4% for the first half of the year. UPS does not report supply chain volumes, but revenue growth was led by the ‘other’ segment which saw 7.1% growth for the quarter ending June 2024. This was due to growth in the new healthcare logistics area, though it was not enough to offset the other declines impacting the logistics segment.

Expansion

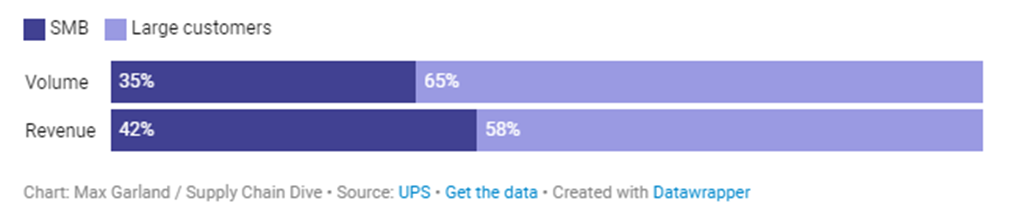

To keep margins high during low-volume periods, UPS is repositioning to appeal more to SMBs Currently SMBs make up 29% of UPS’s US volumes, with a target of 40%. Though in the international segment, the mix is more favorable with around 60% SMB. With large customers the prices charged are usually negotiated, offering little in terms of margin. According to a former marketing director speaking to SupplyChainDrive the contribution margin of a single SMB package can often equal 10 enterprise packages.

As discussed in our FedEx article, USPS (United States Postal Service) has switched providers to UPS for air mail services. The contract will last for at least the next 5.5 years. While it had provided a drag on FedEx, UPS tends to have a more efficient air network with its Worldport strategy of fewer massive air sorting facilities allowing for a smaller, more optimized air fleet. Management states it expects the USPS contract to be margin accretive, especially going into peak holiday season. With UPS US domestic air volumes down 8%, the contract could provide a small boost during down markets. Provided that UPS does not expand its aircraft fleet to accommodate mail volumes and uses the mail to improve capacity utilization, we feel that it will be accretive.

UPS has continued its expansion into healthcare, with the acquisition of two German healthcare logistics providers. Under the Supply Chain Solutions segment, healthcare logistics reported $10 billion in revenue for the full year 2023. UPS expects this to grow to $20 billion by 2026. More specifically, UPS is targeting the more ‘complex’ side of the market – cold chain and sensor-equipped shipping to ensure proper custody and handling. It does offer traditional healthcare logistics services such as same-day delivery and inventory reduction services through shared decontamination.

The aging developed world population is a massive secular tailwind for Healthcare demand and volumes. According to a study commissioned by UPS in 2022, medical devices as a market will grow at a CAGR of 5.4% to 2028. More critically, only around 15-20% of medical device sales are controlled by the top 10 companies leaving the market incredibly segmented with cost of compliance and logistics the top two concerns for providers.

Risk

Despite Amazon moving more of its logistics operations to its internal service, Amazon still represents 12% of UPS’s total revenue. While the continued loss of this business could potentially hamper e-commerce based revenue and volume growth, it is likely in our view, that the Amazon business is lower than average margins but improves capacity utilization. According to the UPS CFO, the wind-down of Amazon as a UPS customer is mutually planned and will not cause sudden earning shocks.

Overcapacity has been a theme in the logistics and transport market, after massive demand for e-commerce during the pandemic turned into unseasonably lower demand in 2022 and 2023. UPS is no different, with UPS announcing trimming 12,000 jobs in the first half of 2024. According to the CEO during the earnings call for the quarter ending March 2024, the United States had an excess parcel capacity of 12 million pieces per day, with around 6 million belonging to the private sector like UPS and FedEx. UPS will bring its network more in line with demand by closing and consolidating 200 locations.

Financials

For the first 6 months of 2024, UPS had a contraction in revenue of 3.2%, with a 0.8% increase in operating expenses. We believe that this increase in expenses is related to the new union contract kicking in mixed with unseasonably low volumes due to soft economic conditions weighing down the top line. Though, increases in operating expenses will be mitigated as severance expenses conclude from the 12,000 layoffs in the first half of the year.

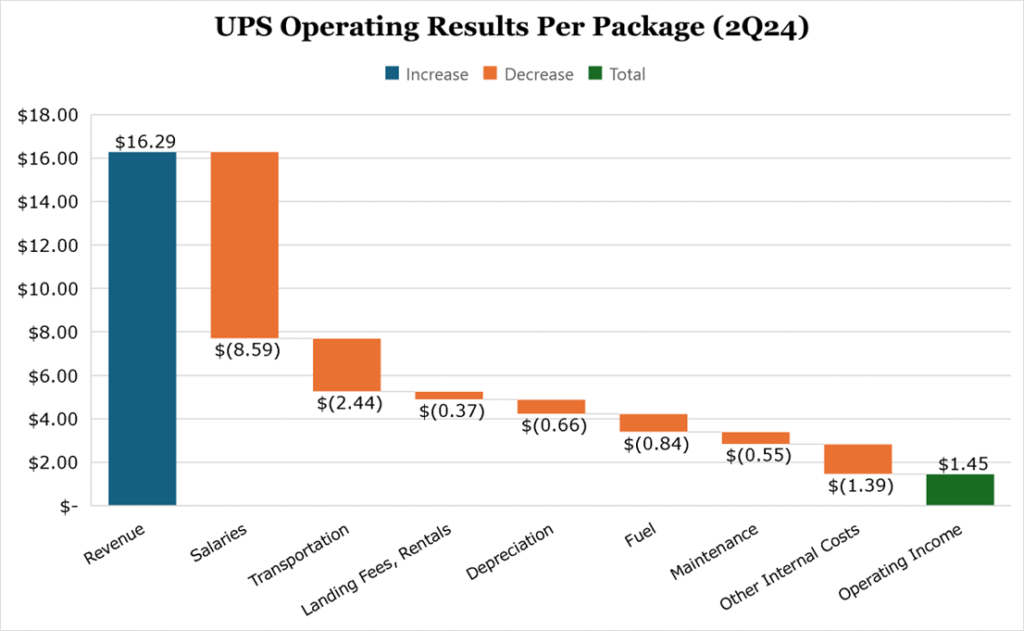

The repositioning toward SMBs and specialized medical logistical services could replace the volume from Amazon. Additionally, targeting SMBs as previously discussed would have much higher margins than pre-negotiated agreements with large shippers. For the trailing twelve months, UPS reports an operating margin of 9.1%, and a net income margin of 5.9% which is slightly above its peers.

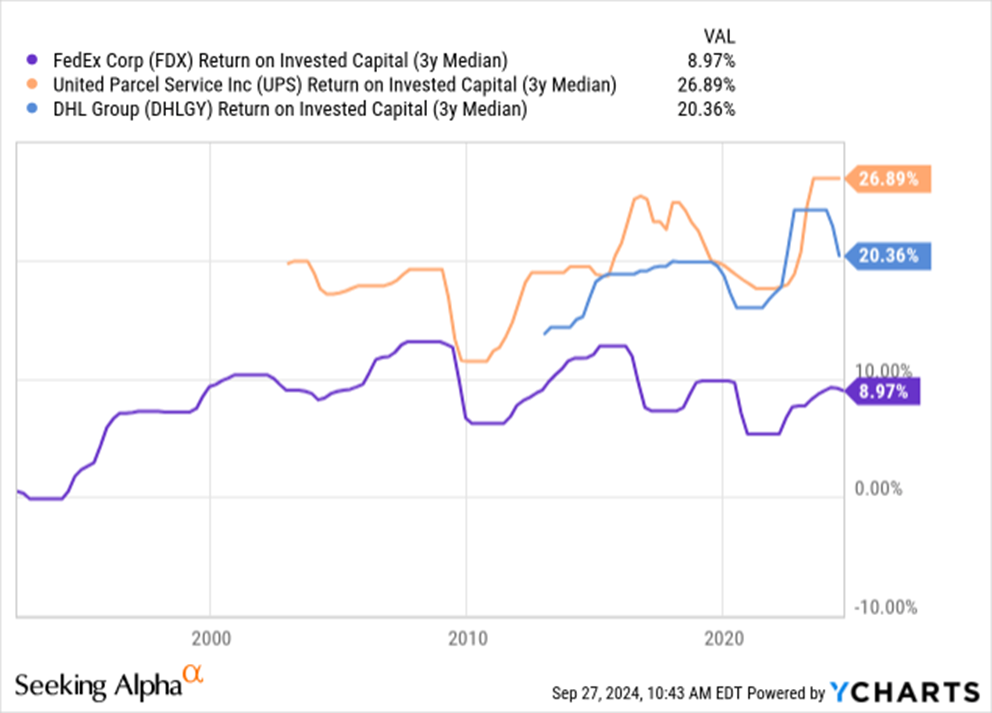

Over the next 5 years, UPS expects to heavily invest in automation, including highly automated distribution centers. According to FreightWaves, UPS will close and consolidate 200 sorting centers across the US, with the new consolidated centers having ~30% additional handling capacity. While we remain skeptical of the total estimated savings of $3 billion per year in savings, UPS claims it will realize $1.5 billion by 2026. For the remainder of 2024, UPS expects to spend less than originally anticipated in capex, now only projecting about $4 billion. As discussed in our FedEx article, UPS has industry-leading return on invested capital, leading with a 3-year median of 26.89%.

UPS expects to return $500 million in share repurchases for the second half of 2024, or about 0.5% of outstanding shares. Currently UPS has a dividend yield of 5.0%, which we feel is very safe. UPS has $6.3 billion in cash and ending 2023 with $5.1 billion in free cash flow generation and expecting to end 2024 with $5.8 billion. UPS has a trailing twelve-month net debt to EBITDA of 1.7x with an EBIT interest coverage ratio of 10x. The balance sheet will be further bolstered by the offloading of Coyote logistics to RXO for $1 billion. Overall, the balance sheet is healthy and continues to lead the industry in strength.

Conclusion

With its strong free cash generation profile and strong cash position it leads the sector. We believe that UPS will recover secularly as the economy enters the upswing, and that the increases in expenses faster than revenues is a result of broader conditions rather than a structural problem. While waiting for the upswing, investors can expect a solid 5.0% dividend yield.

Competitive Comparisons