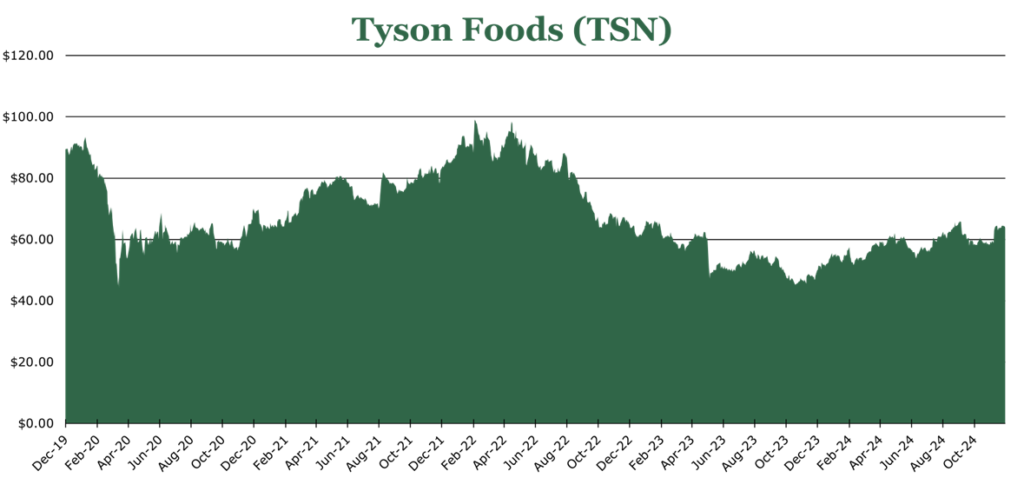

Tyson Foods Farms Free Cash Despite Cyclical Downturn

| Price $63.79 | Dividend Holding | December 10, 2024 |

- 3.14% Dividend Yield

- 13 consecutive years of dividend increases, most recently increasing by 2% in November 2024.

- Despite overlapping downcycles in pork and beef markets, Tyson generated $1.5 billion in free cash flow.

- Shifting more production to high margin value-added products like pre-made food and pre-seasoned meat across all segments.

- Targeting leverage ratio of net debt to EBITDA of under 2.0x, currently 2.6x with most debt maturing past 2027.

Investment Thesis

Tyson Foods (TSN) is an American meat-processing giant, producing about 20% of the consumer beef chicken and pork sold in the United States. With both pork and beef markets experiencing a cyclical downturn, coupled with a strained consumer, Tyson has seen its margins contract and volumes remain relatively flat.

Despite this, it generated $1.5 billion in free cash for the fiscal year ending September 2024 and increased its dividend by 2%. In 2025, it expects the situation to improve towards the end of the year and end with margins slightly higher. In our view, TSN is prepared to weather the storm and once pork and beef markets begin the upcycle, it will be well-prepared to expand its cash generation ability and shareholder returns.

Estimated Fair Value

EFV (Estimated Fair Value) = EFY27 EPS (Earnings Per Share) times P/E (Price/EPS)

EFV = E25 EPS X P/E = $5.40 X 18.2 = $98.0018

A P/E of 18.2x would both bring Tyson to a modest discount to consumer staples and price-in its 20% market share in meat products in the US.

| E2025 | E2026 | E2027 | |

| Price-to-Sales | 0.4 | 0.4 | 0.4 |

| Price-to-Earnings | 18.0 | 14.8 | 11.3 |

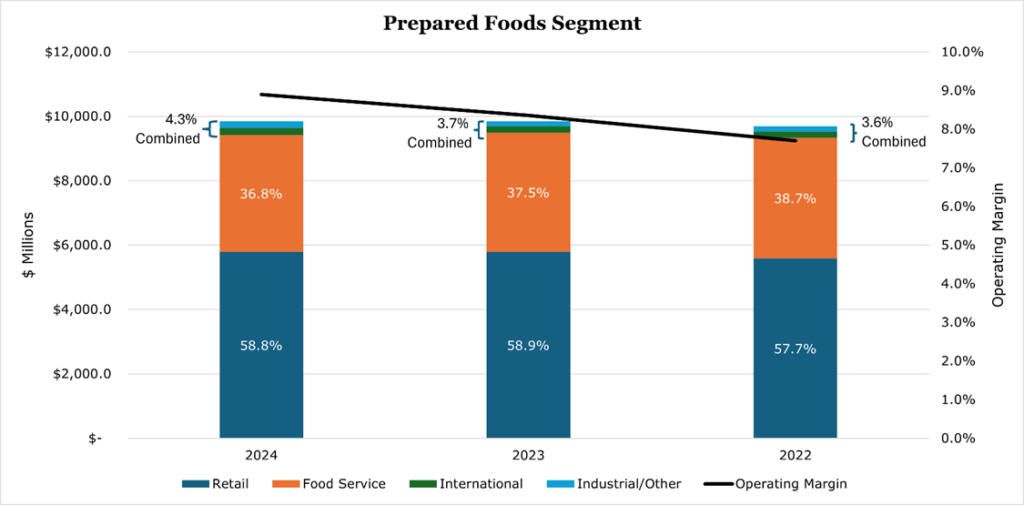

Prepared Foods

Prepared foods contains prepared foods like Jimmy Dean, lunch meats, and pre-cooked items. As of the fiscal year ending September 2024, it represented 18.5% of revenues. Topline growth in the segment was 1.0% year over year, with segment operating margins expanding 56bps to end the year at 8.9%. Average sales price did decrease due to mix changes, but this was fully offset by decreasing input costs.

End customer distribution has remained relatively stable over time, with TSN typically targeting higher-margin retail customers. Over the long term we expect prepared foods to grow to be a larger component of Tyson’s portfolio given its more attractive value-added economics. The market for prepared food does tend to be more seasonal than other segments with a downcycle in the winter.

Management will target further margin improvements in the segment in 2025 to offset companywide flat volumes and weakness in the pork and beef areas. The largest of these initiatives is to reduce the number of products on offer to reduce required inputs and reduce waste. Over the short term, it expects these improvements to yield around 10% growth on the bottom line, ending 2025 at $1 billion operating income, excluding restructuring charges.

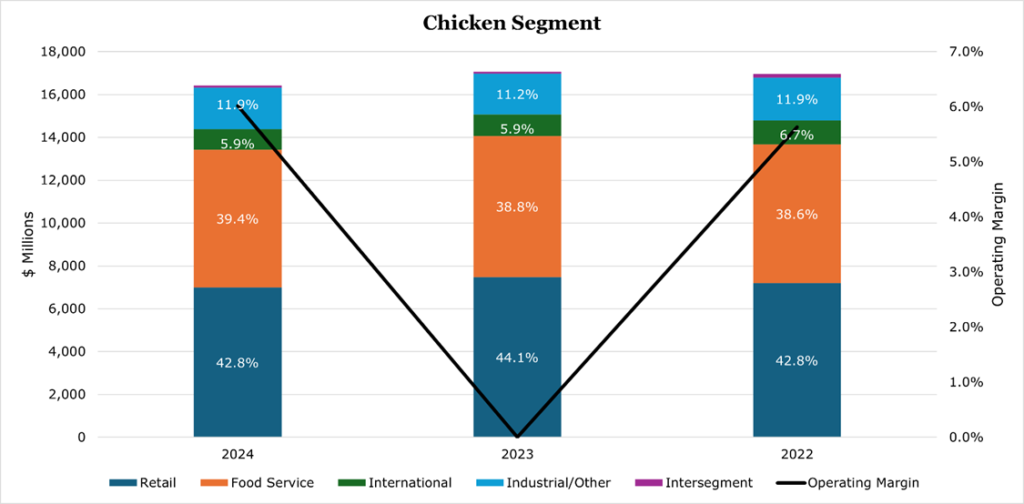

Chicken

The chicken segment contains the vertically integrated chicken processing arm, as well as some pre-packaged chicken products like chicken nuggets. As of the fiscal year ending September 2024, it represented 30.8% of revenues. Revenues in the segment had a -3.7% year over year decline, seeing weakness sales price down 2.4% and volumes down 2.2%. However, segment operating margins recovered to end the year in the positive, generating 6.0% operating margins.

Tyson’s chicken segment tends to have less meat commodity exposure than the red-meat segments, given it has a largely vertically integrated chicken process, raising chickens from egg to slaughter. This has the effect of making margins more stable over time, but still allows Tyson to take advantage of market price increases.

Over the long-term the chicken segment will continue to see some volume tailwinds from the secular shift away from red meats. These include the continued shift toward a health- and environmentally conscious consumer, the favorable economics of chicken production making the market more price stable, and some export demand growth from the rise in global incomes.

Tyson expects the operating income of the chicken segment to grow around the 8% mark, ending 2025 at $1.1 billion in operating income at the midpoint, before restructuring charges.

Much of this will come from the expansion of value-added products, like chicken nuggets, pre-seasoned products, or pre-cooked chicken. While management did not speak specifically on numbers it indicated that the return on investment for these lines in chicken is meaningfully higher than expanding the existing raw processing. In fact, Tyson has shrunk its processing capacity in raw chicken, closing 6 plants (around 10.6% of capacity) since January 2023, commenting that it overestimated the demand for raw chicken.

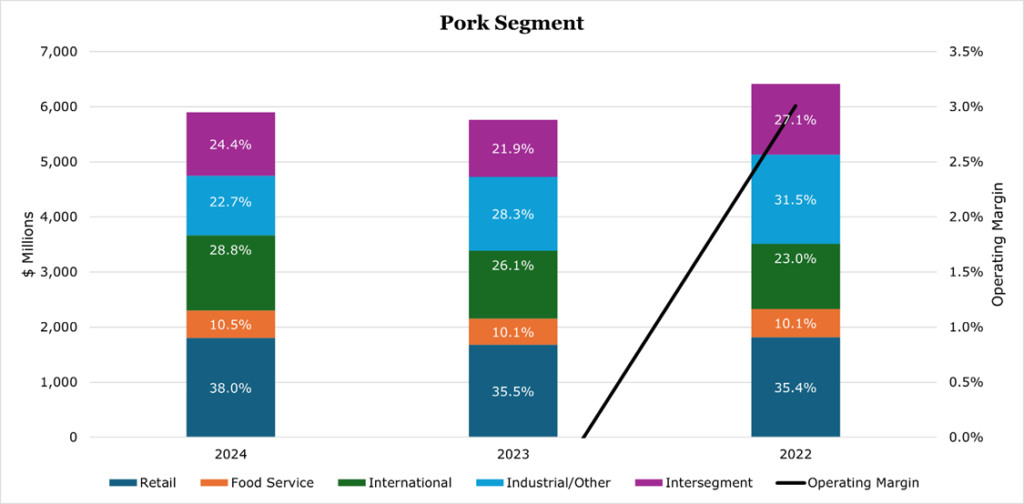

Pork

As of the fiscal year ending September 2024, the pork segment represented 11.1% of revenues. Revenues saw a moderate increase of 2.3% for the fiscal year ending September 2024, driven by a 3.8% increase in volumes. Segment operating margins ended the year at just below breakeven at -0.67%, it was a 28.7% year-over-year increase given the decreases in input prices.

Pork operations are sensitive to pork commodity prices, as Tyson typically purchases live hogs from the market before processing them. Currently, global pork demand has stalled amid a strained domestic consumer and low demand from China as it imports less. Conversely, the number of slaughtered pigs has increased due to fears of avian flu and a longer-term supply glut if Chinese demand continues to stall. To reach a more sustainable equilibrium during the downcycle, Tyson has contracted its pork processing capacity by 10.6% since the start of 2023.

Tyson expects the segment to be similarly breakeven to 2024, though management was optimistic it could be more positive on an operating margin basis in the second half of 2025.

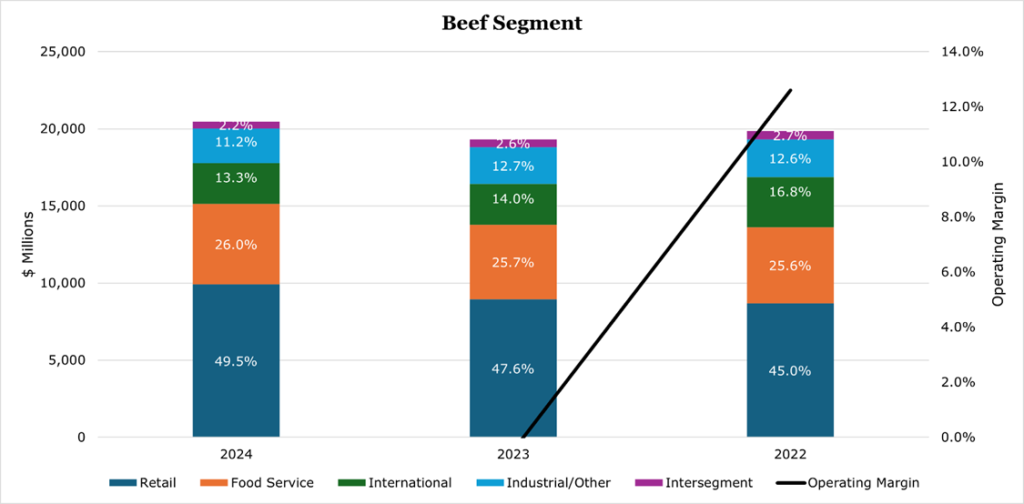

Beef

As of the fiscal year ending September 2024, the beef segment represented 38.4% of revenues. Revenues saw an increase of 6.0%, driven by a 1.6% increase in volumes, and a 4.4% increase in average price. Segment operating margins ended the year at -1.9%, with Tyson being highly sensitive to input prices.

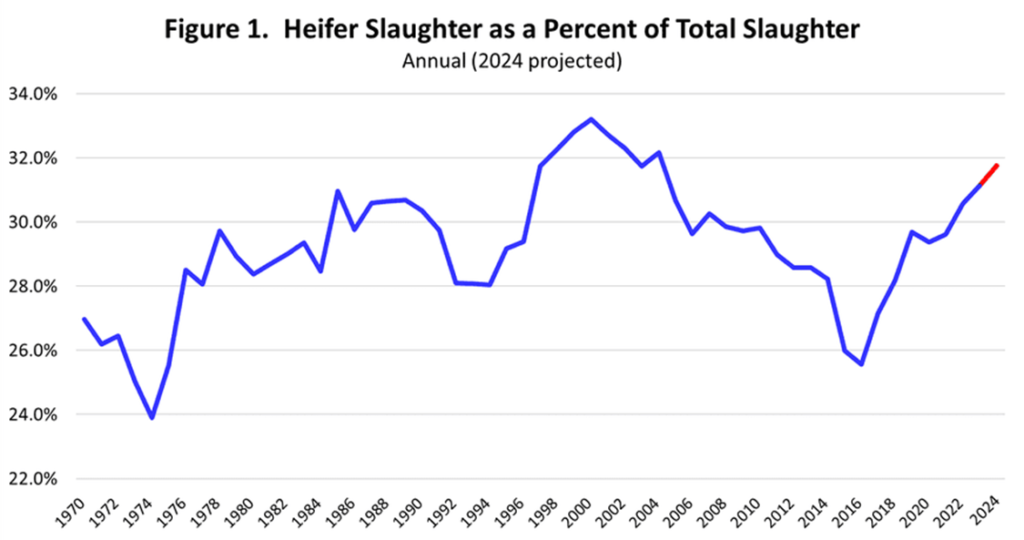

Over the last 5 years a mixture of drought, fertilizer shortages, tightening feed supplies, and economic hardship tightening consumer’s ability to spend on more expensive cuts have driven inventories to the lowest level in 73 years. There is little pressure for ranchers to expand their herds amid high interest rates and uncertainty regarding feed supply, which has extended the down part of the beef cycle and pushed the slaughter of Heifer (breeding cows) to all-time highs.

As of the end of October 2024, there is little sign that ranchers are retaining breeding stock to grow herds. Agriculture Bank CoBank says that weather conditions have improved – indicating relief on the horizon for feed prices – but tight credit conditions and opportunity costs are still pushing most to sell off or slaughter Heifers rather than retain them. Once the retention begins, it typically takes 2 years for Heifers to actually produce a calf to add to the beef-cattle population. Additionally, the number of cattle to slaughter would decrease during this time, which could put compression on margins across the supply chain.

In our view, it is unlikely that Tyson will see meaningful improvement in the Beef segment until the Heifer slaughter ratio increases below 30%, the long-term baseline and typical indicator used to determine if ranchers are rebuilding herds.

Tyson has not expanded or contracted its capacity since the beginning of 2023 and stated that it will be focusing on being prepared for the upcycle sometime past 2025. It expects similar profitability levels as 2024, but a more pronounced volume contraction once Heifer retention begins sometime in the second half of 2025.

Risk

International exports have traditionally offered a safe offloading point for excess capacity, as there is no need to adjust products to local consumption. Tyson reported at the Barclay’s consumer staples conference in September 2024 that exports of pork to Mexico held up the breakeven nature of the segment during the downturn. While the actual risk of a global tariff – or a blanket tariff on Mexican or Canadian goods – is low, it would pose material impacts to Tyson’s business if implemented.

In the non-value-added areas, like raw beef or pork processing, Tyson has very little control of the price of inputs. Given the commoditized and substitutable nature of proteins, it also has very little pricing power. During the quarter ending September 2024 earnings call, management indicated that around 85% of these businesses are at the mercy of market prices and they can do only loss-mitigation during downcycles.

While Tyson expects volumes to be flat overall, it could see some beneficial margin tailwinds. Primary food components for pigs and chickens, Corn and SBM (Soy-bean meal), have seen steady declines in price given supply gluts domestically. Historically demand for meat tends to be inelastic, meaning outside the chicken segment suppliers are likely to absorb any incremental gains. However, Tyson does still hold the opportunity for more margin gains in the Chicken segment as a result.

Financials

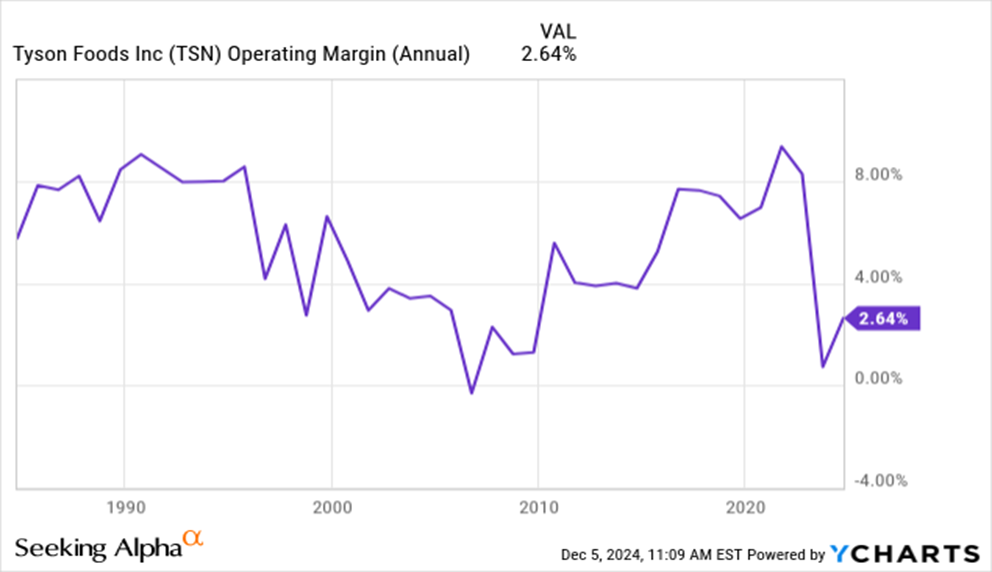

For the entire company, volumes were flat year over year, but still saw revenue growth of 0.8% thanks to increases in average sales price of 0.6%. Overall operating margins for the fiscal year ending September 2024 were 2.6%, a slight recovery year over year, but still at the bottom end of the cycle. Given the overlap in the downcycle of Pork and Beef, margins will remain challenged until at least 2026.

For the year ending September 2025, Tyson expects revenues to be flat but does expect some incremental gains in operating income. This will almost certainly come in the format of expanding high margin prepared foods across all segments.

Despite the challenging environment, Tyson generated $1.5 billion in free cash. For 2025, it expects to generate a similar level of free cash flow, which should mean the dividend is safe. Currently Tyson pays 3.14% yield, or a payout ratio of 63.2%. In early November Tyson raised its dividend by 2%, making 13 years of consecutive dividend increases. Given management is confident they are at the bottom of the cycle, we expect the dividend to increase at or just above 2% in fiscal 2025 depending on conditions in the second half of the year.

Tyson is currently authorized to repurchase 2.0% of outstanding shares, though given the down cycle and the relatively low pace of historical repurchase operations it is unlikely Tyson will repurchase a meaningful number of shares in 2025.

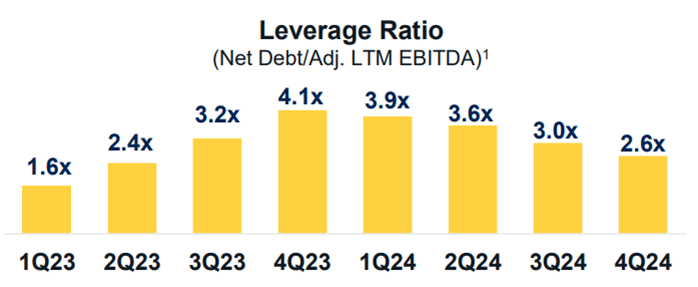

Tyson has a debt rating of BBB, and a long-term leverage target of 2.0x net debt to adjusted EBITDA. As of the quarter ending September 2024, it has moved down to 2.6x.

Overall debt levels are not meaningfully burdensome to continuing operations, with a coverage ratio of 3.7x and a weighted average interest rate of 4.8% on fixed-rate debt which represents 84.3% of debt outstanding. On variable debt, which represents 15.7% of outstanding debt, the rate is 6.7%. Given the high level of free cash even at the bottom of the cycle, Tyson could more aggressively pay down obligations. Equally, it will likely refinance the variable component of the debt if rates come down.

Conclusion

The overlapping downcycle in pork and beef markets has put downward pressure on volumes and margins for Tyson. However, Tyson has a strong bottom line from its growing prepared-foods segment and its dominance in the chicken market to offset the losses.

Overall, Tyson foods represents a safe consumer staples bet for dividend income. Once the upcycle begins for pork and beef, it is likely that Tyson will return to its long-term average operating margin and return to steady dividend increases.