TDK’s Tech Surge Sparks Free Cash Potential

| Price $12.14 | Growth Holding | October 31, 2024 |

- TDK is leader in small solid state batteries and announced supply agreement with Apple

- Growth areas in wearables, phones, IoT (Internet of Things) and EVs (Electric Vehicles)

- Dominant market share in several areas, including in smartphone battery components, holding the #1 market share of 50-60%.

- Strong manufacturing and materials science expertise, first to bring silicon anode batteries to market in 2023.

- Targeting late-stage development products for M&A.

- Aggressive capital efficiency plan, potentially divesting business units that do not meet the 10% ROIC watermark.

$1 USD = 150 JPY

Investment Thesis

TDK (TTDKY) is a Japanese industrial components supplier, manufacturing 120,000 different products across 80 business units and 4 segments. We feel that TDK has secular tailwinds from continued electrification and continued embedded IoT (Internet of Things) growth across the global economy.

On a more granular level, TDK continues to be a market leader in small-scale battery technology and material science, being the first to bring new silicon anode batteries to market. In its more mature magnetic components segment, TDK invested heavily in turning around the HDD (hard-disk drive) market over the trailing 3 years; attempting to bring HAMR (heat-assisted magnetic recording) drives to market to continue beating solid-state drives in total cost of ownership.

Overall, TDK is upstream of several key growth markets. Thus, we think that its diversity of products and conservative management with a renewed commitment to shareholder returns while running leaner, make it a good buy for investors seeking broad exposure to high-tech manufacturing.

Estimated Fair Value

EFV (Estimated Fair Value) = EFY25 EPS (Earnings Per Share) times P/E (Price/Earnings)

EFV = E25 EPS X P/E = $0.80 x 19.4x = $15.52

We note that the current P/E of 16.8x lags electronic component peers and does not price in the secular growth in EVs and small batteries.

| A2024 | E2025 | E2026 | |

| Price-to-Sales | 1.7 | 1.6 | 1.5 |

| Price-to-Earnings | 21.7 | 16.8 | 15.8 |

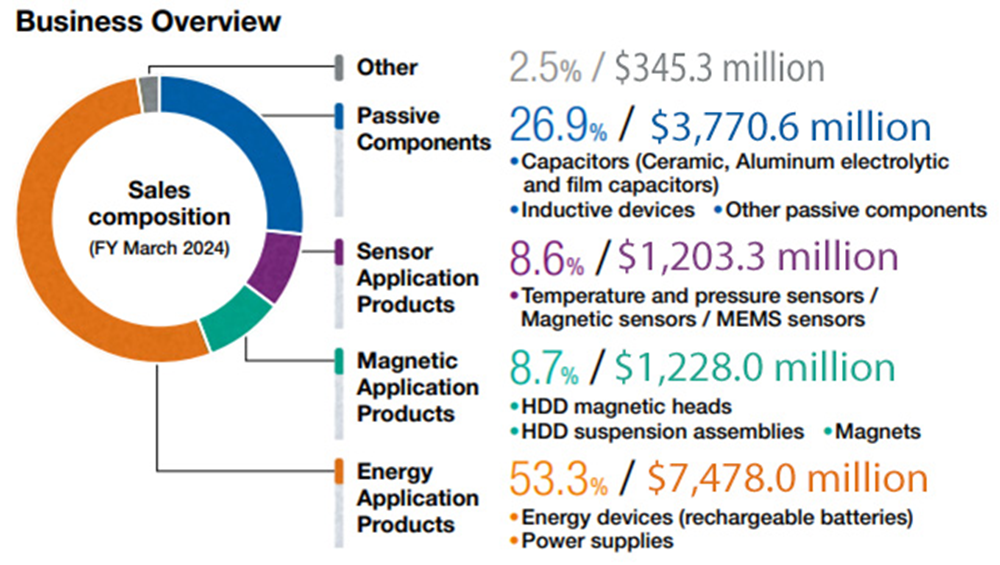

Core Business

In the energy application segment, sales decreased by 4.4% year over year in the quarter ending June 2024 primarily due to transferring parts of the industrial manufacturing base to joint ventures. However, operating margin expanded to 21.0% representing an operating income increase of 71.9% year over year.

In passive components, sales increased by 1.6% year over year, due to increases in demand for inductors in both the automotive and communications end use categories. Overall, the segment increased its operating income by 13.6% year over year, though it was unprofitable due to continued weakness in the EV (electric vehicle) and industrial end markets. Over the medium term, we expect the segment to return to profitability with the recovery of the EV market.

In the magnetic components segment, sales increased by 43.9% year over year due to the startup of several new products cycles in the smartphone area and general seasonality. The increase in sales was enough to bring the segment into profitability, with a 1.4% operating margin.

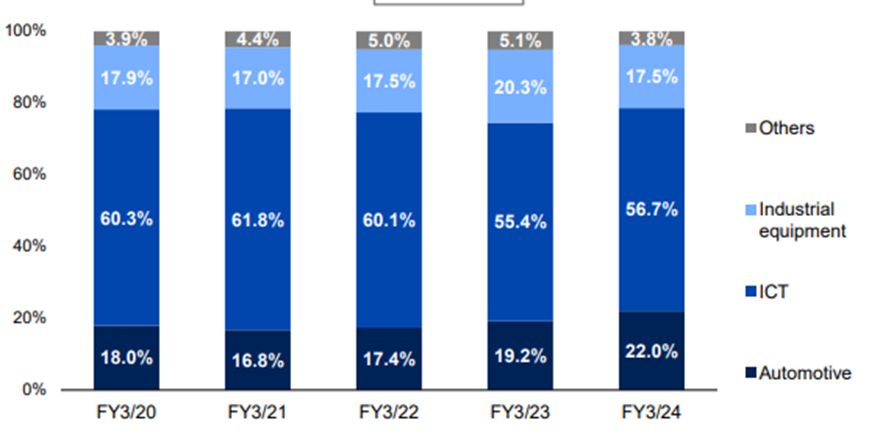

Secularly, we expect the automotive area to continue to grow as a percentage of TDK’s total revenue. According to the 2024 Integrated Report, TDK expects the market for automotive components to grow in excess of 12% CAGR to 2029.

Continued Material Advancements in Battery Technology

TDK holds the #1 share (15-20%) in medium capacity batteries, for end uses such as battery backups or tool electrification. TDK also holds the #1 share (50-60%) of small capacity batteries for usage in wearables, IoT, and smartphones.

In January 2024, TDK became the first company in the world to take silicon anode lithium batteries to market. TDK states that the new batteries have an extra 10% capacity over conventional graphite anode batteries, though laboratory testing showed up to 40% capacity over the conventional material. As of the announcement, silicon anode batteries made up under 5% of TDK’s smartphone battery sales. Over the long term, we expect TDK to continue to transfer small battery capacity toward silicon anodes. To 2027, we expect a 10% annual ramp, with TDK stating that it expects to switch over 10% of small-battery capacity to silicon anodes in 2025. While TDK has not commented on the margin profile of the silicon anode business, it is likely that its higher energy density provides a strong value-added proposition relative to cost of manufacturing.

In June 2024, TDK announced it had made a materials science breakthrough in the form of a new solid-state battery cell, with an energy density 100x larger than its current graphite cells in lab testing. The new technology can be made much lighter, longer-lasting, and faster charging than a traditional lithium-ion battery. The new battery would also be far safer, utilizing ceramics instead of graphite giving both better heat resistance and eliminating the risk of corrosion. Over the medium term, TDK will market the material to be used in products that use traditional coin batteries or require frequent charging, like smart watches, wireless earphones, and hearing aids.

As of the announcement, TDK is working on scaling up the technology for large scale production and a potential scale up to smartphone usage. We remain optimistic that TDK will be able to take the technology to market, and if successful, would likely have first-mover advantage given its large book of business including customers like Apple. Apple has been steadily increasing its presence in the wearables space, ending 2023 with approximately 38 million Apple Watches sold, and 75 million sets of Air Pods sold.

New Growth with Automotive

As of the quarter ending June 2024, automotive end-uses represent 22% of TDK’s business, growing 89% since 2020 and 5.1% year over year. While demand growth for EV battery components has seen some slippage, it was more than offset by sensor sales. While TDK does not provide a full EV sized battery for automobiles, it is a leading provider of upstream technology.

TDK has two core products in the automotive area, EMC filters (1 market share, 45-50%) and ceramic capacitors (2 market share, 35-40%). EMC (electromagnetic compatibility filters) and ceramic capacitors are designed to reduce interference on sensitive electronic components, like ECUs (electronic control units). We feel with the transition to ‘software-defined vehicles’ as discussed in our Volkswagen article; EMC components will be in much higher demand given the growing usage of more delicate computing components in automobiles.

In the medium term, GM and TDK are in talks to open a TDK operated factory in the southern US for the production of CATL (Contemporary Amperex Technology) licensed battery components for EVs. This is a change from GM’s initial posture of seeking to solely-own a factory. We feel that GM’s decision is likely due its own internal struggles to produce batteries and Ford landing in hot water with congressional lawmakers over CATL’s Chinese origin.

We feel that the likelihood of the licensing agreement is good, as CATL has a long-standing relationship with TDK, and already has regulatory approval for a JV with TDK in battery-tech. The terms of the deal are not yet public, but Bloomberg has reported it will be a long-term fixed-price contract.

Datacenter Driven Magnetic Business Recovery

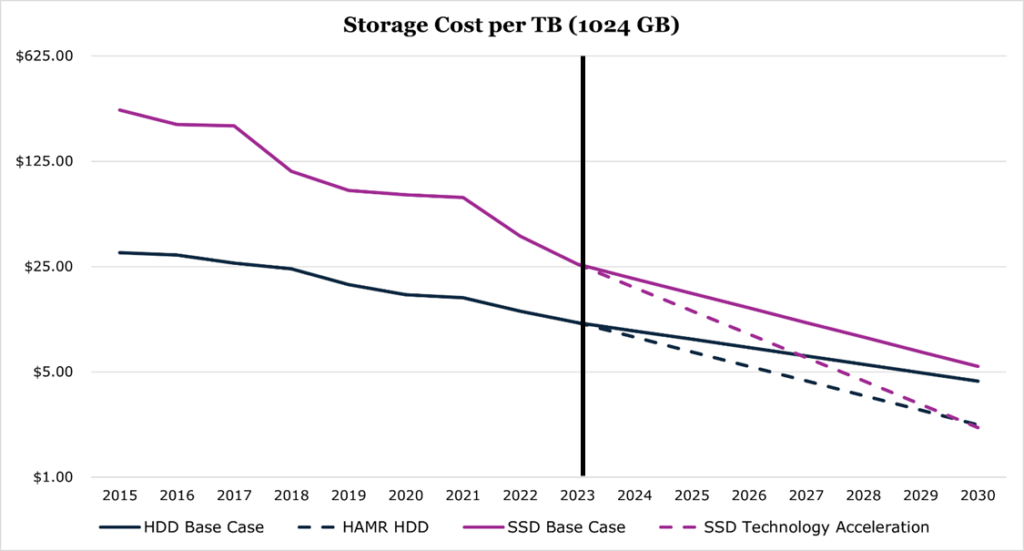

Currently, the HDD (hard disk drives)-linked business makes up 8.7% of TDK’s revenues and is at a long-term bottom. We feel that this is due to AI workloads requiring faster SSDs (Solid-State-Drives), thus most of the boom in datacenters has been concentrated in SSD-required workloads.

TDK is investing in HAMR (heat-assisted magnetic recording) to extend the longevity of the business, potentially allowing HDDs to continue to beat out SSDs at scale in reliability and storage density. TDK is confident in its current ability to manufacture HAMRs at cost-effective scale by 2027, with competitor Seagate already shipping HAMR sample drives to customers and claim that HAMR HDDs will continue to hold a 6:1 total cost ratio over SSDs.

SSDs have been steadily improving in cost per TB (terabyte). Aggressive estimates put the crossover point where SSDs match HDDs in cost sometime in 2026 or 2027. Though, in this aggressive case, we feel that other factors like HAMR reliability and storage density improvements will still leave substantial market share on the table for the HDD businesses.

We feel that as AI-hype dies down, the elevated capex many companies have put into SSD storage will roll off, and datacenter providers will return toward a mixed-storage solution to optimize total cost of ownership. Overall, we feel that HDDs may regain some market share with the introduction of high-density high-reliability technologies such as HAMR (heat-assisted magnetic recording).

Risk

The CATL licensing agreement with TDK could come under fire from US lawmakers. Previously, CATL and Ford’s deal caused a congressional probe, which has thus far not had broader consequences, but did put Ford in hot water. Starting in 2025, the Inflation Reduction Act prohibits battery components or minerals from ‘foreign entities of concern’ from being a part of investments or purchases that would normally provide tax credits or grants. On the political side, former President Trump has stated that if re-elected, he would suspend the Inflation Reduction Act, which would kill the $7,500 clean vehicle tax credit which has provided a much-needed boost to the consumer-side of EV demand.

We find that GM’s unwillingness to enter as an equity partner into the battery factory odd. We feel it is unlikely that TDK will be able to fund the plant, estimated to employ 1,000 people, on its own without taking on substantial debt.

The Inflation Reduction Act has cut-outs in funding for batteries made with Chinese-originated components. While the licensing of technology does not currently render a battery ineligible to receive various credits and grants, TDK does have several manufacturing facilities in China that it would be unable to source base components from. Specific output numbers by geography are not public, but 52.2% of TDK revenue for the quarter ending June 2024 originated from China and TDK currently operates two large manufacturing facilities in China. In an effort to de-risk its supply chain, TDK has begun a strategy of “China Plus” to begin battery component manufacturing operations in India in 2025.

In the HDD business, TDK is in a difficult situation. With negative ROIC and low profitability, it has largely cut the segment from future capex, with cumulative capex from 2025-2027 projected to fall by 52.6% compared to the 2022–2024-time frame. Without substantial manufacturing investment, it is unlikely that HAMR technology will ever reach economies of scale required for profitability and thus the HDD business will continue to a secular decline.

Financials

Compared to the previous mid-term plan (March 2022 – March 2024), TDK exceeded revenue, free cash, and capex targets. However, it missed operating margin and ROE goals.

The new medium-term plan (March 2024 – March 2027) emphasizes growing into higher margin value-added products, which ideally will translate to higher free cash generation through improved operating margin. The previous plan emphasized ‘turnaround’ spending in mature segments, which did not pay off as expected on the bottom line.

| Metric | March 2022 Plan Targets ($ millions) | Actual March 2024 Results ($ millions) | March 2027 Goals ($ millions) |

| Sales | $13,333 | $14,026 | $16,6667 |

| Operating Margin | 12.0% | 8.2% | 11.0% |

| ROE | 14.0% | 7.9% | 10.0% |

| FCF (after repurchases and dividends, cumulative 3-year) | Positive | $1,040 | $1,733 |

For the new plan TDK will focus more on portfolio-level growth potential, namely more aggressive ROIC targets on a per-segment basis. TDK’s CEO emphasized that even if a business unit meets profitability targets, if the ROIC falls below the hurdle rate of 10%, parts of it could be on the chopping block within the decade. In our view, this will be met with much more aggressive and proactive divestitures in mature business units, and a more aggressive growth posture either through M&A or JVs.

| Segment | March 2024 ROIC Actual | March 2027 ROIC Target | March 2027 Capex Target (cumulative $ millions) | Change in Capex (compared to 2022-2024 period) |

| Passive Components | 7.7% | 15.0% | $1,333 | 4.3% |

| Sensor Products | 1.2% | 8.0% | $533 | 22.5% |

| Magnetic Products | -12.2% | 4.0% | $400 | -52.6% |

| Energy Products | 21.5% | 18.0% | $2,133 | -15.8% |

| Company-wide | 5.3% | 8.0% | $4,667 | -10.8% |

On the M&A side, TDK has a self-imposed deal size limit of around $1 billion which we feel will likely fit into Energy Products or Sensor Products segments. Both segments fit into the broader secular tailwind of electrification and offer high-value-added potential to boost margin and ROIC. Historically, TDK has targeted the acquisition of companies in late-stage development utilizing its manufacturing expertise and customer connections to accelerate the product to market.

Currently TDK has more than $4 billion in cash on the balance sheet, which is elevated compared to its typical $2-3 billion figure. We feel this is due to exchange rate risk in Japan and management’s historical conservatism. Currently, TDK targets a long-term debt-to-equity between 0.3x and 0.4x, of which it is currently 0.37x. We feel that the number will likely fall to the lower end of the target, with TDK reducing its debt by 12.3% year over year for the quarter ending June 2024. Overall, we see little balance sheet risk given management’s conservatism, with an interest coverage ratio of 17.9x.

The new medium-term plan out more shareholder returns than the previous plan, with a payout ratio boosted to 35% from 30%. Currently TTDKY yields 1.0% and does not conduct share repurchases. However, the new medium-term plan does carve out the potential for repurchases with excess cash. Management has stated repurchases will be considered if TDK increases its price to book to consistently over 2.0x (currently 1.97x).

Conclusion

Despite headwinds in its mature segments and low industrial demand, TDK holds a diverse portfolio of products that are upstream of key growth markets in IoT, EVs, and consumer technology. Overall, we are confident in management’s ability to execute its 2027 plan, which includes stronger free cash generation, a higher focus on shareholder returns, and better portfolio management on top of expansion into high-value areas such as energy and sensor technology.