PotlatchDeltic’s Strong Roots Amidst Headwinds

| Price $43.24 | Core Holding | August 30, 2024 |

- 4.2% Dividend Yield

- Trading at substantial discount to our $53 per share estimate of asset value.

- Timberland is good inflation hedge.

- Share repurchases demonstrate management’s belief in the underlying asset values.

- Strong real estate performance has offset the weak performance in the wood products segment.

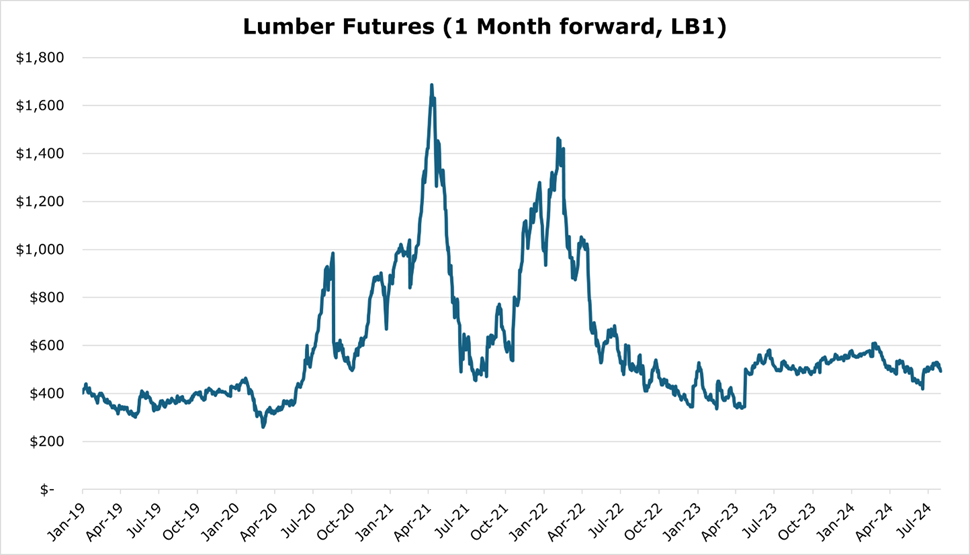

- Lumber market appears to have bottomed out with expectations of a recovery in the spring.

Investment Thesis

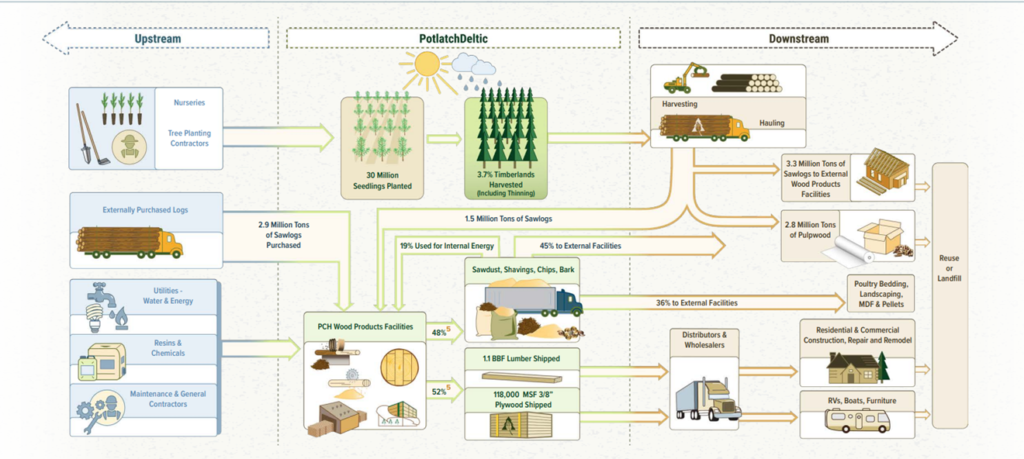

PotlatchDeltic (PCH) is a lumber REIT with 2.2 million acres of timberland and 7 sawmills, concentrated largely in the Pacific Northwest and Deep South.

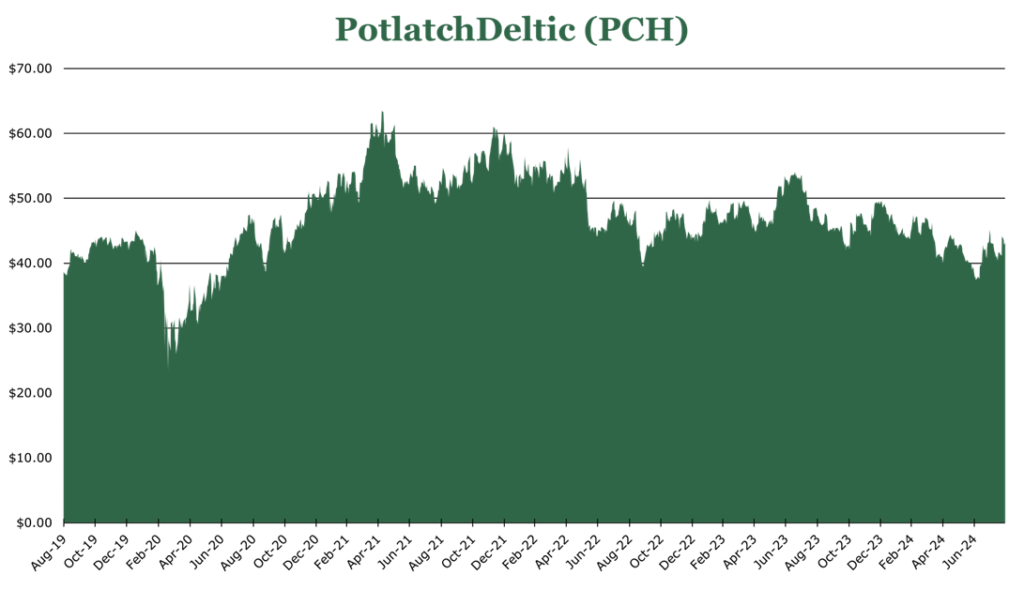

Currently, the lumber market is depressed by oversupply and unseasonably low construction demand. This has driven PotlatchDeltic’s price down by 11% over the trailing twelve months, now trading at a discount to asset value which is $53 per share in our opinion.

| Asset | Asset Value (Per Share) | % of total |

| Timberland | $42.51 | 80.3% |

| Roads/Non-Mill Land Improvements | $1.70 | 3.2% |

| Milling inventory | $1.80 | 3.4% |

| PPE (net) | $6.94 | 13.1% |

| Total | $52.95 | – |

While the short-term remains challenging, PotlatchDeltic’s initiatives in cost reductions at its sawmills, capex spend on modernization of sawmills, and strong liquidity position put it in an excellent position once the upcycle starts. In the meantime, we believe that its strong performance in the real estate development segment will largely offset any losses from poor lumber pricing and continue to provide investors with its 4.2% yield.

Estimated Fair Value

EFV (Estimated Fair Value) = EFY25 EPS (Funds from Operations) times P/FFO (Price/FFO)

EFV = E25 FFO X P/FFO = $3.10 * 17.5x = $54.25

While we expect some headwinds in funds from operations due to lumber pricing, we believe PotlatchDeltic trades at a discount to its asset value, which we feel is currently $53/share. Thus we feel that a price to funds from operations ratio of 17.5x would not only close this gap but also bring it more in line with peers.

| E2024 | E2025 | E2026 | |

| Price-to-Sales | 3.3 | 3.2 | 3.2 |

| Price-to-Funds from Operations | 16.3 | 14.5 | 13.2 |

Market Conditions

The slump in lumber prices has taken a toll on mill assets, with more than 1.6 billion board feet capacity closing across 13 mills in North America – or around 2% of total capacity

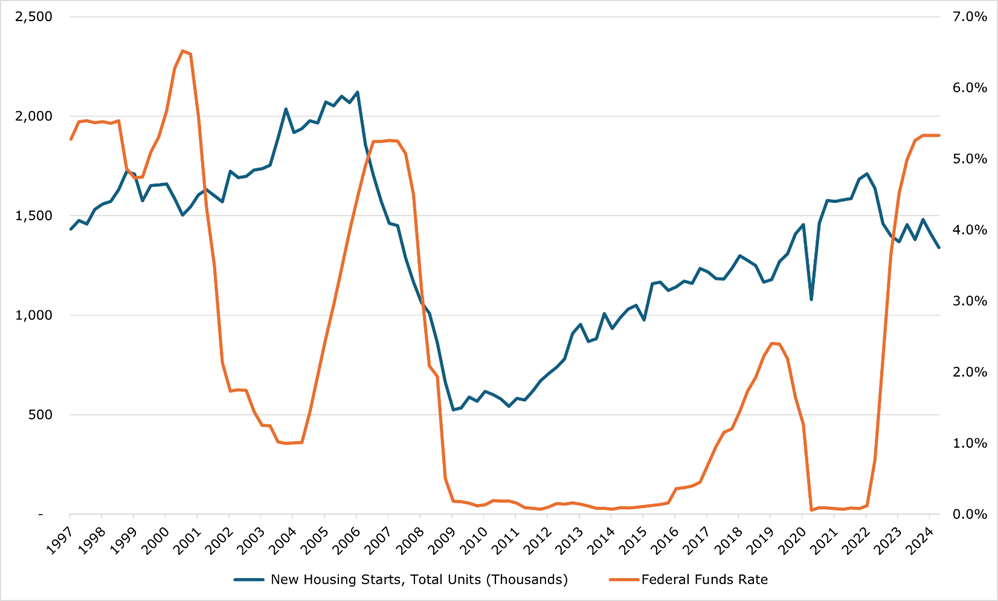

Overall, there has been stagnant housing starts and lack of remodeling demand, with high interest rates putting substantial downward pressure on lumber prices. In our view, housing is still undersupplied in the United States. Therefore, we feel as though the lumber market is bottoming out and will begin the upcycle once interest rates come down. PotlatchDeltic expects the upcycle to begin in 2025, with some favorable pricing tailwinds if the Fed cuts rates as expected in the remaining part of 2024.

Lower rates should help housing starts and thus drive increased lumber demand which will in turn improve timber volumes and possibly pricing. While Northern timber typically has higher realized prices, its strength means it has more limited end uses. On the other hand, Southern timber, which typically has a lower realized price, will likely see higher volumes as the upcycle begins and its more diverse end product usage and thus more consistent demand.

Core Business

PotlatchDeltic manages 2.2 million acres of timberland and 7 sawmills, with around 30% being in Idaho, and the remaining being in the South concentrated in Arkansas. Typically, PotlatchDeltic utilizes about 60% of Southern timber internally with 33% of Northern timber used for its own sawmills to produce lumber. The remaining is sold as raw sawlogs, or the rights to harvest the land is leased to others. The real estate development segment is the sale of land holdings that can be sold at prices well above timber acres, such as for a planned housing community. Finally, the wood product segment operates PotlatchDeltic’s sawmills which produce both finished products like softwood board lumber and associated byproducts.

While typically the real estate segment has relied on the sale of land to generate revenue, there is increasing demand for environmental products which PotlatchDeltic labels NCS (Natural Climate Solutions). These include solar options, carbon offset credits, and mining rights options. In our view, the most promising of these is solar leasing options contracts. As of the half year ending June 2024 PotlatchDeltic has options on approximately 1% of its land, or $300 million in NPV if the options are exercised, to firms exploring land for solar development. Typically, these options last for around 5 years. Since 2018, only 2 of these have been exercised into full leases, though PotlatchDeltic did state that it has seen substantially more activity in the area since the IRA (Inflation Reduction Act) and expects to see 1 or 2 be converted into leases in 2025.

Risk

Currently the timberland market is very competitive with high interest rates and low-timber prices making the premiums on acquiring timber assets not as attractive for PotlatchDeltic. During the Nareit conference, PotlatchDeltic stated that it had bid on 12 separate deals during 2023 and lost on all of them being unwilling to pay the premium demanded by the existing land holder. Much of PotlatchDeltic’s current expansion in holdings comes from private land deals. Though, high M&A prices has allowed additional capital to be deployed in both share repurchases and capital expenditures.

Around 75% of PotlatchDeltic’s timberland volume is directly tied to the current spot price of lumber. During the pandemic, this was incredibly advantageous with prices hitting record highs, but now that we are near or at the floor of the cycle, it has dragged down revenue as well as made revenue more volatile.

Results

| 6 Months Ending June 2024 | ||

| Segment | % of Total Revenue | EBITDDA Margin |

| Timberland | 31.9% | 35.9% |

| Wood Products (Mills) | 50.3% | -2.3% |

| Real Estate | 17.8% | 89.7% |

| Company Wide | – | 24.2% |

The Timberland segment expects to harvest 7.6 million tons for the full year 2024 which would be flat year over year. Around 80% of volumes will come from the South due to the previously discussed wood’s end use being more diverse and thus more stabilized in price. Additionally, we believe that based on the guidance of 55% sawlog sales in the South (compared to 44.6% in 2023) is indicative of PotlatchDeltic routing more sawlogs to the market rather than sending them to its own sawmills.

| Segment | 2024 Expected Revenue ($ millions) | Change from 2023 (%) |

| Timberland | $373.7 | 7.2% |

| Wood Products (Mills) | $469.7 | -7.5% |

| Real Estate (Rural) | $121.0 | 122.0% |

| Real Estate (Planned) | $16.4 | -18.9% |

PotlatchDeltic reported minor EBITDDA losses for the first 6 months of 2024 in the milling segment. Currently, PotlatchDeltic does not have any plans to downsize milling operations but has instead embarked on a campaign of changing product mix to more premium products that still have margin to capture and switching to a more “just-in-time” inventory system until demand recovers. Additionally, PotlatchDeltic will continue its modernization program of its Waldo, Arkansas sawmill which will reduce capacity by 10% (25 million board feet out of the current 200 million in capacity) temporarily until the mill returns to service. On return to service, PotlatchDeltic expects costs to improve by about 30%, add 6% to recovery rate, and increase capacity by 42.5%, which at the mid cycle of the lumber market would equal about $25 million in additional EBITDDA per year. Remaining capex for the project is estimated to be $44 million with around half to be spent in 2024.

Even still, PotlatchDeltic saw a 28.7% year over year increase for EBITDDA in the first half of 2024 due to strong rural land demand in the real estate segment. Overall, PotlatchDeltic expects revenue to be flat or slightly down this year. For the first 6 months of 2024, operating margin was 2.3%, which is a substantial contraction from the first half of 2023 which saw 9.8% operating margin. While real estate has thus far been able to buoy margins amidst low prices, we do expect the second half of 2024 to be slightly weaker in real estate which may no longer be able to offset the wood products segment if lumber prices do not begin to recover until 2025.

Financials

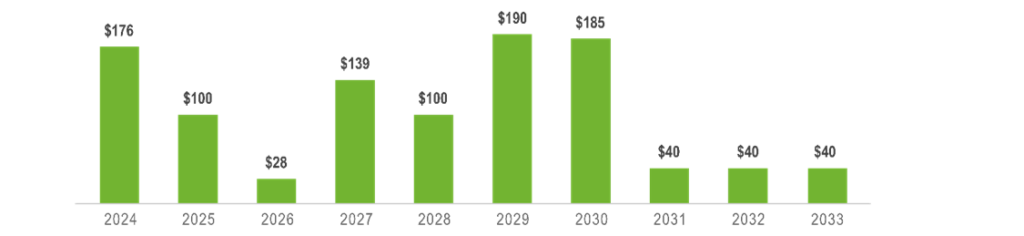

PotlatchDeltic has a current ratio of 1.3x, with a net debt to EBITDDA of 6.4x, with a long-term net debt of $1 billion. PotlatchDeltic will refinance $176 million of its maturity portion of debt to acquire lower interest rates.

While the debt load is high, PotlatchDeltic has a strong liquidity position with $199.7 million in cash on hand and a $500 million credit revolver. With M&A prices unfavorable, we don’t expect the debt load to increase meaningfully above its current level.

PotlatchDeltic pays out 4.2% dividend yield, a $1.80 annual payout which has grown at 2.4% CAGR since 2019. PotlatchDeltic has $100 million remaining in repurchases, or around 3% of outstanding shares. As previously mentioned, higher than desired M&A prices have made repurchasing shares more attractive for PotlatchDeltic, which we expect to continue at its current pace of around ~1% per quarter or slightly accelerate before the upcycle.

Capex for the full year 2024 is expected to be $100-110 million, due to the previously mentioned Waldo sawmill upgrade. The company expects less capex going into 2025, back to a “normalized level”. In our view, this means that capex will reduce back down to the $50-75 million level, which may free up capital for M&A activity at premium prices, or further shareholder returns.

Conclusion

In the face of weak demand and pricing, PotlatchDeltic has pulled back around 11% over the trailing twelve months. This pullback pushed it to trading at a discount to enterprise value, which currently sits at around $53 per share. While the short-term remains challenging with weak lumber prices and high M&A costs, we believe the market has bottomed out.

As the upcycle takes hold due to falling interest rates spurring construction, PotlatchDeltic is in an excellent position to capture the upside while offsetting any short-term downside with real estate sales. We believe the 4.2% dividend yield and discount to asset value provides a strong case for dividend investors looking to get in at a discount.

Competitive Comparisons