Navigating Horizontal Expansion Amid Challenges

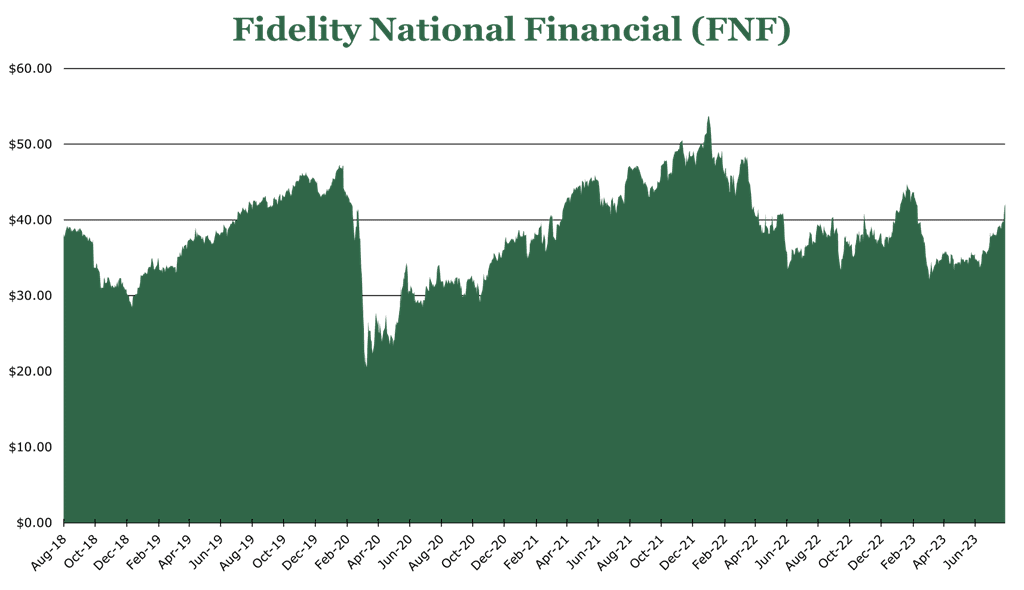

| Price $41.90 | Dividend Holding | August 14, 2023 |

- Dividend yield 4.27%, experiencing a recovery in both commercial and residential title issuance markets.

- Investment in technology to provide further value-added solutions for real estate.

- Long-term reinsurance deal with Blackstone, significantly reducing risk on the books and costs by as much as 25%.

- Strong balance sheet, free cash flow machine at $21.70/share past year.

Investment Thesis

Fidelity National Financial (FNF) is an insurance company providing a wide range of insurance, financial services, and technical solutions. Through dedicated investment to diversify the business, FNF has utilized its market-leading position in title insurance to expand.

Despite persistent weakness in the commercial real estate market and a still-recovering housing market, FNF has strong free cash generation, continuous expansion outside of title insurance, and a stable dividend yield of 4.27%.

Estimated Fair Value

EFV (Estimated Fair Value) = E24 EPS (Earnings Per Share) times PE (Price/EPS)

EFV = E24 EPS X P/E = $4.80 X 14.2 = $68.16

| E2023 | E2024 | E2025 | |

| Price-to-Sales | 1.0 | 1.0 | 1.0 |

| Price-to-Earnings | 10.5 | 8.6 | 7.0 |

Title Insurance

The segment in which FNF has the largest stake is 31% market share in the title insurance market. Title insurance is offered to protect property buyers or brokers from potentially unseen legal claims to property. This industry is roughly $29.7 billion, growing by 10% 5-year CAGR, largely due to the spike in housing prices making property claims more valuable.

Of title insurance sold directly to buyers, it has 41% market share, and in real estate agent sales, it has a 29% market share. What sets FNF’s strategy apart in the title insurance space is its usage of a multi-brand, often localized, strategy to increase scale. This includes several wholly-owned subsidiaries with significant localized advertising. Normalized pre-tax title insurance margins are 15-20%, but rising interest rates and reduced commercial real estate activity have pressed down new originations. However, due to its scale, FNF still maintains a higher than peer margin. Typically, FNF keeps 300 million in reserves for title claims, with an average loss ratio of 3-5%.

With the downturn in all mortgage originations, FNF has cut field staff by 26% net of acquisitions in 2H22. Year over year, residential title insurance is down 6%. Residential mortgages are generally seasonal, with most issuances occurring in Feb-April. Thus far in FY23, FNF has seen solid growth month over month in mortgages, including into late July, when mortgages traditionally are past their issuance peak for the year. This could signal recovery in the real estate market, with consumers adjusting to higher interest rates after pausing from sticker shock.

As previously stated, commercial real estate has seen significant weakness compared to pre-COVID volume with a 22% year-over-year reduction. However, volumes were up 12% quarter over quarter. FNF believes this is a sign that the weakness is still here but that a seasonal pattern is returning to commercial mortgages.

Technology and F&G

FNF has invested significant money into acquiring insurance and real estate technology. Automated platforms reduce costs and provide end-to-end transaction coverage, significantly improving the value proposition for a customer. The largest of these platforms is inHere, an end-to-end real estate technology solution. In 1H23, inHere has seen over 1 million sessions on its technology platforms, with 90% activity in the last 30 days. This demonstrates strong adoption of the platform, with FNF expecting to continue to invest money into the platform in the coming years.

In 1Q23, FNF purchased TitlePoint for $224 million in cash from Black Knight (BKI). TitlePoint is a property information research firm that utilizes proprietary tools to ensure no hidden property claims on a title before insurance is underwritten.

FNF operates F&G as a majority-owned subsidiary, selling off 15% equity to investors under the symbol FG. F&G is a full-service life insurance company serving retail and institutional life insurance. F&G boasted stronger results of 11% year over year in 2Q23, reaching a 15% increase in assets under management. However, reinsurance costs have been increasing, which has driven down margins. COVID-19-related mortality has dropped off significantly but still poses ongoing problems for reinsurance costs. F&G has a long-term reinsurance agreement with Blackstone, which has just been renewed to FY29. The partnership allows for a net reduction of fees of 25% on assets over $40 billion, significantly reducing reinsurance costs.

Risk

The increase in interest rates has driven the market value of fixed-income investments in FNF’s portfolio, creating $4.4 Billion in unrealized losses. FNF averages A rating for debt, and F&G averages an NAIC 1.43 rating, or roughly A equivalent. The consolidated investment portfolio has $54 billion in AUM, mostly concentrated on corporate and structured debt.

The real estate market heavily determines FNF’s revenue outside of the F&G segment. Persistent weakness in the real estate market would adversely affect results and the balance sheet. Similarly, high mortality events such as COVID-19 significantly impact life insurance claims for F&G.

Outlook

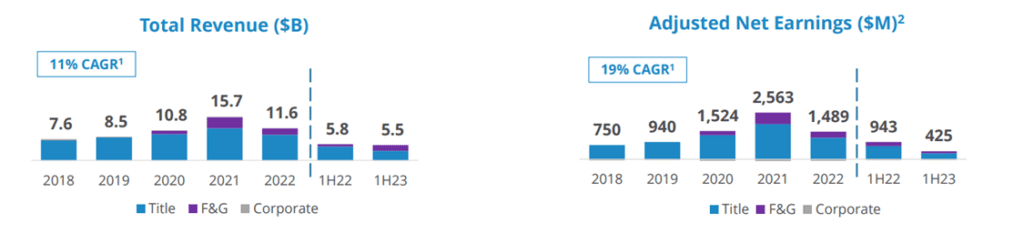

FNF’s revenue is volatile and highly dependent on real estate transactions; hence, revenues and profits have pulled back dramatically since 2021, but appear to be stabilizing and potentially recovering. FNF targets leverage usage with a minimum debt-to-capitalization ratio of 20. Currently, the debt-to-capital ratio is 28.3%.

FNF currently distributes $500 million per year in dividends with management indicating that it is stable. The dividend has no specific policy beyond this fixed figure, though quarterly cash flow and market conditions are reviewed. Share buybacks have a similar policy, with an announced slowdown in repurchase activity versus 2021 and 2022. Due to market conditions, FNF has repurchased $300 million less than last year. FNF does expect to accelerate buybacks in 2024. FNF currently holds $885 million in cash on hand for potential acquisitions or a cushion for unforeseen macroeconomic impacts on its business.

Despite the challenges, FNF demonstrates a strategic approach to the future of its business. Through robust FCF generation, stable dividend, and a strong balance sheet, we believe that FNF is a good dividend stock.

Competitive Comparisons