Melco is a Discounted Way into Asia-Pacific Gambling Recovery

| Price $5.27 | Growth Holding | March 31, 2025 |

- Melco’s strategic shift to an asset-light model promises improved capital efficiency while maintaining its strong 15.6% Macau market share.

- Ongoing property renovations across the portfolio to organically attract high-value customers after junket market contraction.

- 2025 Projected capex increase of 70.5% to $415 million, backed by a $1.1 billion cash position.

- Targeted expansion into emerging markets like Sri Lanka and potentially Thailand creates long-term growth avenues beyond the core Macau operations.

- Despite 6.1x net debt to EBITDA ratio, management’s focus on deleveraging and potential Manila asset sale should strengthen the balance sheet.

Investment Thesis

Melco Resorts & Entertainment (MLCO) is an integrated casino-resort operator primarily focused on Asian operations. Its largest geographic footprint is in Macau, though it recently opened a casino on Cyprus and is moving forward with an investment in Sri Lanka.

For future investments, Melco has stated it is switching to be more asset-light targeting only fitting and operating gaming floors as a part of other integrated resorts, rather than self-building new properties. We believe this is a step in the right direction and will allow Melco to expand its footprint while also continuing to operate its highly profitable Macanese properties.

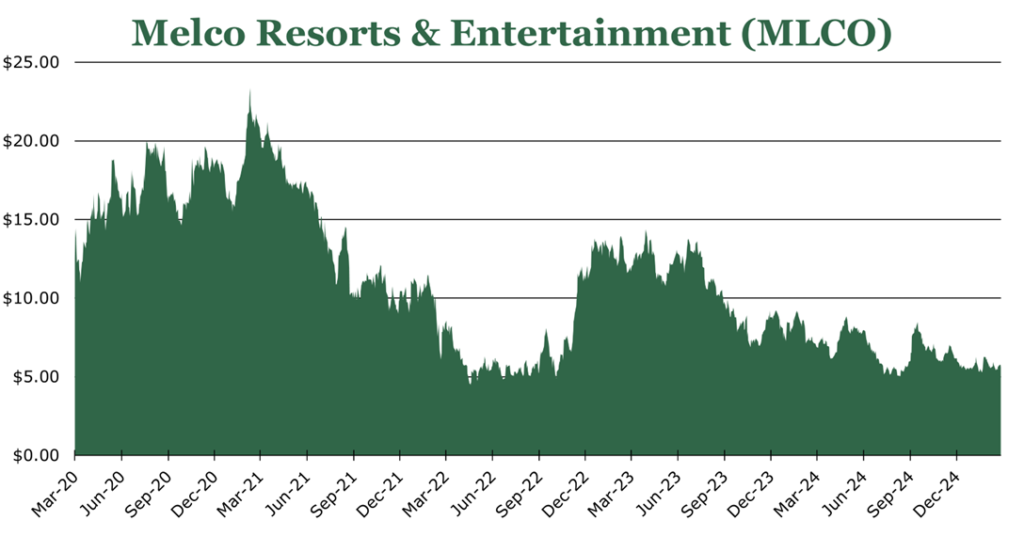

Over the trailing twelve months, the stock has fallen 20.6% following a continued crackdown on junkets weighing down VIP spend and tourism to Macau being only 79% of pre-pandemic levels. However, with several key expansions opening during 2025 which should provide a boost to earnings and a stated focus on reducing the debt level, we believe that Melco’s shares are undervalued.

Estimated Fair Value

EFV (Estimated Fair Value) = EFY26 EPS (Earnings Per Share) times P/E (Price/EPS)

EFV = E26 EPS X P/E = $0.58 X 15 = $8.70

| E2025 | E2026 | E2027 | |

| Price-to-Sales | 0.5 | 0.5 | 0.4 |

| Price-to-Earnings | 15.1 | 8.9 | 6.8 |

SeekingAlpha Analyst Consensus

Important Definitions

Mass Table Hold: this is the percentage of chips purchased by non-VIPs that is retained by the casino. For example, if the mass table hold is 30%, the casino retains $0.30 for every $1 in chips purchased. There is generally an inverse relationship between length of gambling and mass table hold. Put another way, high mass table hold indicates that non-VIP players typically have short play sessions.

VIP Win Rate: this is a measure of gambling turnover from VIP customers. As VIP customers typically utilize rolling-chips and gamble longer, this metric is slightly different from mass table to account for this effect. For example, if the VIP win rate is 2.5%, VIP players wager $1,000,000 over the course of their stay, the Casino expects to retain $25,000.

Integrated Resort: differs slightly from a standalone casino or a casino-hotel in that it typically has a mall-like assortment of amenities such as theatres, attractions, different hotel or casino options and several restaurants on the same property.

Gaming

The major revenue driver for casinos globally, is gaming. Casinos make money on the house edge in games, which is a built-in advantage usually derived from lower payouts than the true odds, probability manipulation in slots, or rules that favor the casino. Over time, the house edge approaches the lower bounds in the table below.

| Games | House Edge |

| Baccarat/Punto Banco | 1.1% |

| Blackjack | 0.3% |

| American Roulette | 5.3% |

| European/Asian Roulette | 2.7% |

| Craps (across all bets) | ~1.5% |

| Sic Bo/Cussec | 2.8% |

| Slots | 5-15% (usually a legal maximum) |

Source: Wizard of Odds. House edges are considered absolute minimums, actual outcomes are typically wider in spread based on length of stay.

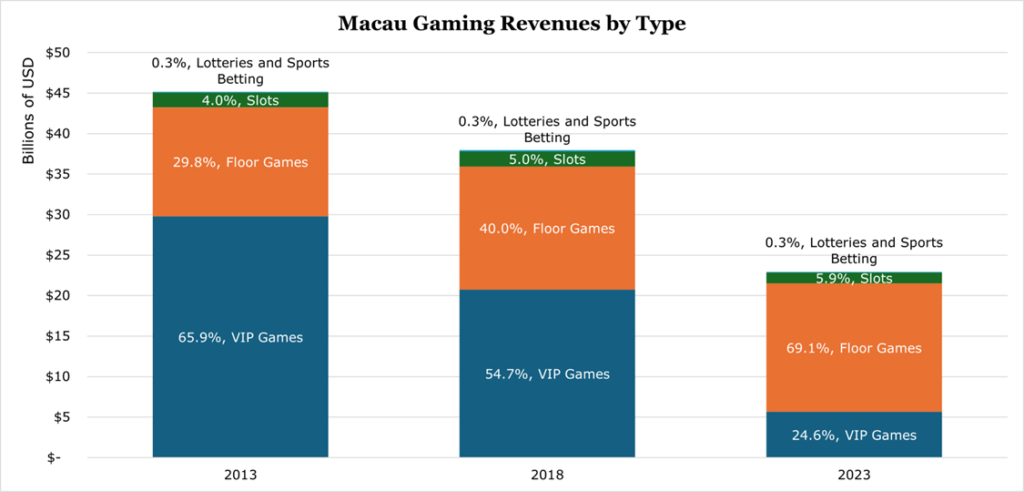

Geographically, this poses a challenge for operators. In Asian casinos, players typically prefer table games with more luck than skill, namely Baccarat, which represented 84% of gaming revenue in Macau in 2023, second to Slots at 5.9%, and third Sic Bo (also called Cussec) at 3.5%. Statistically, Baccarat has one of the lowest house edges, only beaten by a skilled player in Blackjack. In Western casinos, slot play typically makes up around 60-70% of gaming revenues, though at Melco’s Cypriot casino slot play is 50.8% of gaming revenues.

Junkets: A Special Consideration

On a per-gambler basis, Asian casinos typically generate a much larger portion of their revenue from a much smaller group of high-roller clientele than Western casinos. The difference is due to the prevalence of gambling promoters known as “junkets”.

Historically, these operators came about to exploit loopholes in China’s strict currency outflow controls. Junkets serve as intermediaries between casinos and wealthy clients, providing credit to prospective gamblers so that they don’t have to move large sums of money out of China and risk running afoul of domestic controls on gambling outflows. This credit is exchanged for special chips at the casinos, called “rolling chips”. These are different from normal chips, as they must be wagered at least once before cashing out. This guarantees every dollar is gambled at least once. While the house-edge on popular VIP games like Baccarat is low, the high-stakes gambling generally allows for high profit. For bringing in the customers, junkets are often paid a commission based on the total volume of bets placed by a high roller rather than a percentage of winnings.

This relationship has come under intense scrutiny by Chinese authorities. As of 2022, junket operators are capped to a limit of 1.25% commission on chip wagers, are banned from revenue sharing, are banned from having preferred access to casino facilities, and several CEOs were arrested. On the casino side, casinos are now legally responsible for junket misconduct which has changed the risk calculus involved in using junkets versus organic expansion. The amount of junkets licensed in Macau collapsed from 235 in 2013 to just 36 in 2023. This has broader implications in the Asia-Pacific region generally, with many Australian, and Philippine casinos also relying heavily on Macau-based junkets for high-roller customers.

In order to cope with lost gaming revenues from a fading junket market, pressure from Chinese authorities, and a quickly diversifying base of visitors, many casinos including Melco, have begun large investment programs into alternative entertainment options and programs to drive more organic high-value customer growth. While we expect there to be growing pains associated, the Singaporean model of small-casinos and large-entertainment venues has proven successful. However, this does run counter to the asset-light plans of management.

More than 80% of Macanese government tax revenues come from gambling taxes. Thus, we expect the approach to be softer handed going forward now that the junket market has been reined in.

Macau Operations

Macau operations represent most Melco revenues, with the CEO reporting that Melco had a 15.6% market share in Macau gambling during the quarter ending December 2024. Melco operates 3 flagship properties in the city, Altira, City of Dreams, and Studio City with Studio City being only 60% owned by Melco. Combined, all properties had 4,588 hotel rooms and 8 total Michelin Stars across their 7 major restaurants. Macau operations also include non-casino gaming clubs in the form of Mocha.

City of Dreams is the flagship of Melco’s operations, targeting high-end luxury customers through its 770 rooms. For the full year ending December 2024, the average daily rate increased 5.0%, with occupancy increasing 700bps to 93% thanks to a stronger peak tourism season. In the quarter ending December 2024, revenues were up 11% year over year, driven by a 14% increase in gaming revenues which was evenly split across all player segments.

| City of Dreams (Macau) | ||

| Quarter Ending December 2024 | Change from 4Q23 | |

| Non-Gaming Revenue | 14.5% | flat |

| Table Revenue Per Unit Per Day | $16,118 | 8.5% |

| Machine Revenue Per Unit Per Day | $571 | 6.3% |

| Mass Table Hold | 32.0% | +49bps |

| VIP Win Rate | 2.35% | -20bps |

| Operating Margin | 13.6% | -506bps |

A driver of the decrease in operating margin is due to increases in staff for better service quality, and a lower VIP win rate. We believe that this, along with renovations for accessibility, is part of the broader push to retain high-value customers organically rather than relying on junkets. We expect margins to recover back to normal levels in 2025, as Studio City transferred its VIP operations to City of Dreams in October 2024.

Studio City is Melco’s newest Macanese integrated resort with a planned 1,600 rooms, targeting the middle to upper end of the mass market. For the full year 2024, average daily rate increased 7.8% with occupancy increasing 600bps to 96%, thanks to the previously mentioned strong peak tourism season. Total revenues were up 13%, driven by a strong focus on slot play which increased 19%.

| Studio City (60% Ownership) | ||

| Quarter Ending December 2024 | Change from 4Q23 | |

| Non-Gaming Revenue | 16.3% | +52bps |

| Table Revenue Per Unit Per Day | $12,563 | 5.2% |

| Machine Revenue Per Unit Per Day | $401 | -4.1% |

| Mass Table Hold | 31.1% | +211bps |

| VIP Win Rate | 3.48% | +162bps |

| Operating Margin | 6.7% | -46bps |

The small decrease in operating margin was due to the transfer of VIP operations to City of Dreams. We expect margins to continue to be down in 2025 due to continued renovations. However, impacts may be limited as the renovations in the high-limit area are rolling off, which should bring in higher numbers of wealthy players organically.

Altira is the smallest of Melco’s Macanese integrated resorts, with 230 rooms. For the full year 2024, average daily rate decreased by 2.2% due to renovation activity, though occupancy recovered to 96% by the end of December 2024. Total operating revenues were down 7%, due to a 17% decrease in gaming revenues because of the previously discussed renovation activity.

| Altira | ||

| Quarter Ending December 2024 | Change from 4Q23 | |

| Non-Gaming Revenue | 21.4% | flat |

| Table Revenue Per Unit Per Day | $8,363 | -6.7% |

| Machine Revenue Per Unit Per Day | $277 | 22.0% |

| Mass Table Hold | 22.7% | -107bps |

| VIP Win Rate | N/A | |

| Operating Margin | -8.0% | N/A |

Given promotional activity and a weak economic environment in China, a slower than expected return to gaming is not surprising. Altira operates no VIP operations, so there is very little buffer during economic downturn.

Finally, Mocha is a series of non-casino gaming clubs around Macau. These machine-focused clubs grew their revenues by 2.0% year over year for the quarter ending December 2024 with an operating margin of 16.3%. Hold percentages are typically marginally lower at 15.3%, though there are fewer staff and fewer comps to weigh down margins.

Other Asia

City of Dreams Manila is a 939-room integrated resort, part of a JV with local firm Belle Corp which owns 33% of the integrated resort. For the full year 2024, lodging facilities saw their average daily rate decline by 7.3% though occupancy remained steady at 97%. The decline in lodging revenues was driven by local competition and a decrease in Chinese tourists who traditionally make up the backbone of integrated resort visitors.

In the quarter ending December 2024, total revenue was up 11%, driven by a 14% year over year increase in gaming revenues. Increases in gaming revenues were driven entirely by a 109% increase in high-roller gambling. High-rollers at City of Dreams Manila represent 23.5% of total gross gaming revenue.

| City of Dreams Manila | ||

| Quarter Ending December 2024 | Change from 4Q23 | |

| Non-Gaming Revenue | 29.8% | +35bps |

| Table Revenue Per Unit Per Day | $3,773 | 24.7% |

| Machine Revenue Per Unit Per Day | $272 | flat |

| Mass Table Hold | 34.2% | +518bps |

| VIP Win Rate | 4.5% | +54bps |

| Operating Margin | 25.5% | +390bps |

Melco resorts announced its intention to ‘explore opportunities’ related to its property in Manila. We expect them to seek a sale though the most likely acquirer, its local partner Belle Corp, expressed it was not interested in buying out Melco’s share in their JV. City of Dreams Manila has had more than $500 million in hard construction costs and has generated north of $1.5 billion in EBITDA since its opening a decade ago.

In April 2024, Melco announced it would be investing $125 million with John Keells to furnish a gaming floor and a 113 room ultra-luxury hotel in Sri Lanka. The City of Dreams Sri Lanka is part of a broader commercial and residential development by John Keells which already has 687 rooms, conference center, mall, and several residential buildings. The total integrated resort site is projected to cost $1 billion in total and closely mirror the Singaporean model of entertainment-first. The small investment is expected to have a decent payout, with Morgan Stanley estimating $30 million in after-tax and royalty cashflow to Melco annually. While lower than other areas, the country is sparsely wealthy, with Melco’s CEO likening Sri Lanka’s potential to being India’s Macau. The Gaming floor is expected to open in the latter half of 2025.

Europe

On Cyprus Melco operates 3 casinos in the City of Dreams Mediterranean, a 500-room integrated resort – the largest in Europe. For the full year 2024, facilities occupancy increased 300bps to 61% with average daily rate increasing 18.4%. The change in both resort and casino results is due to the facility opening in the middle of 2023 and continues to ramp operations.

| City of Dreams Mediterranean | ||

| Quarter Ending December 2024 | Change from 4Q23 | |

| Non-Gaming Revenue | 32.8% | +531bps |

| Table Revenue Per Unit Per Day | $2,896 | 45.9% |

| Machine Revenue Per Unit Per Day | $356 | 19.9% |

| Mass Table Hold | 21.8% | -29bps |

| VIP Win Rate | 3.1% | +1,191bps |

| Operating Margin | -1.5% | +18,000bps |

In the quarter ending December 2024, total revenue was up 25% year over year. While mass table hold rate declined by 29bps, the total volume of chips purchased increased by 44%, driving gaming revenues up by 31%.

We are apprehensive on the prospects of the casino. Its $660 million price tag and continued operating loss runs counter to the asset-light approach now pursued by management. The Mediterranean island is not a common tourist destination, with just 4 million visitors per year. More importantly, key targeted demographics historically have come from places that are currently embroiled in conflict; Israel, Russia, and Ukraine combined representing 29.5% of 2019 tourist visits.

Expansion

The largest greenfield development is potentially in Thailand. In Thailand, traditional casino gambling has been illegal. However, there is a continued lack of recovery in tourism with 15.6 million fewer tourists visiting Thailand compared to before the pandemic. The Thai government has become more receptive to legalizing gambling, and has approved a bill in January 2025, which will grant 5 gaming licenses with first casino openings projected by 2029. According to Skift, forecasts estimate an average annual boost of tourism of 5-10% and increase GDP by 1%, which would help the ailing tourism sector, which makes up 20% of GDP.

A key concession in the bill is Thai citizens will need to pay a $144 entrance tax to any casino, similar to Sri Lanka or Singapore. The other components are very similar to Singapore’s implementation of gambling, including rules restricting gaming space being fewer than 5% of total area, at least $288 million in liquidity on hand, $141 million per license, $28.7 million in annual fees to the government, and a 17% tax on gross gaming revenues.

Competitors who have already expressed interest include Wynn Resorts, MGM, Galaxy Entertainment and Las Vegas Sands. Melco has already set up an office in Bangkok, and has an ongoing collaboration with THACCA (Thailand National Soft Power Strategy Committee). However, Melco has stated that the timeline is unknown currently.

Given the asset-light approach currently undertaken, we believe the most likely scenario is that Melco licenses the usage of one of its brands to another provider or enters into a JV with a resort partner.

Risk

Sri Lanka represents some country risk. In accordance with the bailout of its $46 billion in defaulted debt, the IMF is requiring Sri Lanka to increase its tax revenue to GDP to at least 15%, up from 11.4% in 2023 and 7.3% of GDP in 2022. While this rapid increase does represent positive state building, it is possible that Sri Lanka will squeeze increasingly harder on foreign investments that rely heavily on foreign income. Sri Lanka levies a $50 fee on locals using casinos. As part of its new budget, the fee will be going up to $100, and taxes will be increased to 18% from 15%. Licensing fees have been raised to $1.5 million for the first 5 years, then $4.7 years for the next 15 years, on top of a $31 million renewal fee.

Gambling remains a heavily regulated industry. Often investments do not work out due to external factors and long legislative timelines. Melco had previously invested nearly $250 million in Yokohama and Osaka, across hotels and even hospitals hoping to earn one of only 3 licenses available in Japan. After 3 years, Melco dropped its pursuit due to the city of Yokohama renouncing its plans to issue a license and Osaka granting a license to MGM.

Financials and Outlook

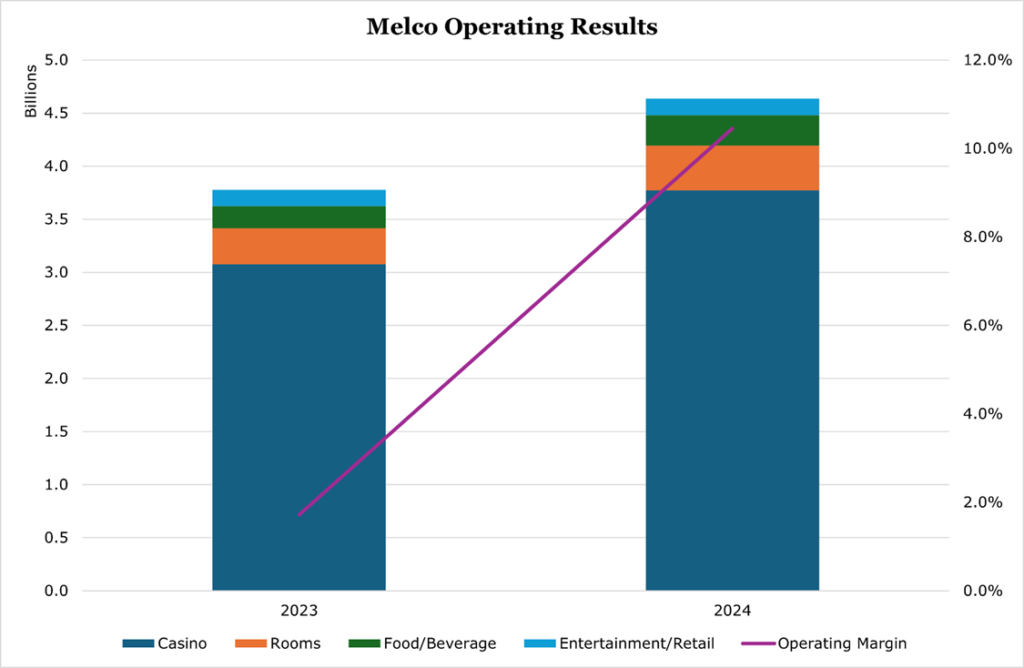

Companywide revenues were up 22.9% thanks to a broad recovery in Macanese tourism, though still only at 79% of pre-pandemic levels. The recovery in operating income was due to the roll off of several overlapping upgrade and renovation programs. We expect operating margins to increase slightly in 2025, though management alluded to high promotional spending activity to draw in more organic traffic along with increasing staff levels across higher-tier casinos and VIP areas.

As discussed previously, management has decided to prioritize an ‘asset light’ model focusing more heavily on operating the casino component of integrated resorts rather than building and operating the typical $1+ billion facilities themselves. We believe this will come in the form of further ‘strategic reviews’ after the completion of the Manila strategic review. Management emphasized it is “trying to shed weight” and that “if Macau lets me do a REIT tomorrow, I would do it.”

For 2025, Melco expects to spend $415 million in capex, a 70.5% increase compared to 2024. Of the $290 million to be deployed in Macau, $70 million will go toward the continuous upgrading and fitting out of Studio City’s new block of rooms. An additional $80 million will go toward Sri Lanka. As of the year ending December 2024, Melco had a cash position of $1.1 billion which is about average. For the full year 2024, Melco generated $383.2 million in free cash.

As of the end of 2024, Melco had a net debt to EBITDA of 6.1x with an annual interest expense of $486.7 million. While this is high, management has stated maturities in 2025 are covered and debt reduction is a key capital deployment priority. If the sale of City of Dreams in Manila goes through, we expect the primary proceed use to be restructuring debt.

Melco has authorization to repurchase 16.7% of its outstanding shares, and management commented that it believes its shares are undervalued. Given the elevated capex and focus on deleveraging, we do not expect substantial repurchasing activity in 2025.

Conclusion

We believe that Melco has a strong premium asset base that should provide strong cash flows over the long term. If a Chinese middle-class recovery materializes in the second half of 2025 it could provide an important boost to operations while Melco focuses capex efforts on expanding existing properties.

Despite facing secular headwinds in the Macanese market and a high debt load, we believe that focusing on asset-light expansions in the future, and a strategic review of operations, is the correct direction to unlock earnings potential. Overall, we believe Melco is undervalued at its current price. Moreover, Macau should continue to recover from Covid and the Chinese crackdown on junkets, thus setting the stage for an acceleration in revenues and earnings.

Peer Comparisons