Carter’s Commands Children’s Clothing Market

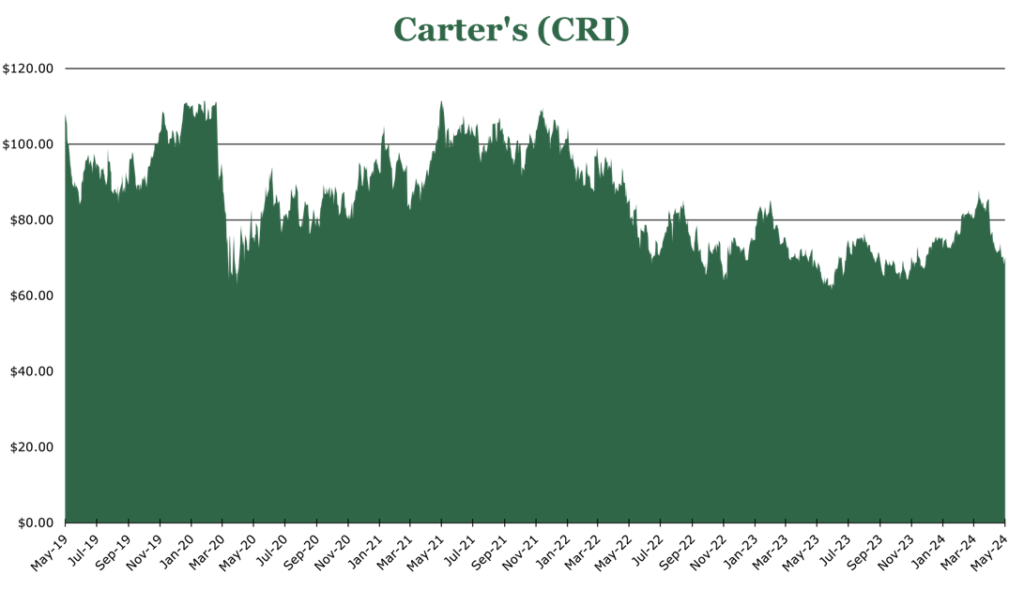

| Price $70.58 | Dividend Holding | May 6, 2024 |

- 4.6% dividend yield.

- Largest market share in baby and children’s clothing in the US, holding 10% market share.

- Collaboration with major retailers like Walmart, Amazon, and Target have helped expand wholesale operating margin by 540bps to 24%.

- Despite a downturn in customer volume, CRI’s retail locations are seeing higher conversion and per-customer unit growth.

- Better mix is expected in wholesale as firms continue to wind down inventory and return to “just-in-time” inventory management.

Investment Thesis

Carter’s Inc. (CRI) is a leading retailer and wholesaler in the young child and baby clothing market. With a significant 10% market share and many competitors being private labels, CRI excels in a market expected to grow at 4-4.5% CAGR through 2028, outpacing the growth rates of adult apparel.

CRI’s partnerships with major retailers like Walmart, Amazon, and Target have yielded strong results even amidst the economic downturn. Additionally, CRI’s retail segment is showing signs of recovery, with improving sales conversions and per-customer unit growth despite an overall decrease in customer volume.

We believe that as the consumer goods upcycle takes hold, CRI to grow at least in line line with, or exceed, the retail sector. In the meantime, the 4.6% dividend yield makes CRI an attractive stock for income-focused investors.

Estimated Fair Value

EFV (Estimated Fair Value) = EFY25 EPS (Earnings Per Share) times P/E (Price/EPS)

EFV = E25 EPS X P/E = $6.75 X 13.3 = $89.78

| E2024 | E2025 | E2026 | |

| Price-to-Sales | 1.0 | 1.0 | 1.0 |

| Price-to-Earnings | 14.3 | 13.3 | 12.4 |

Market Conditions

The young child and baby clothing market was valued at around $250 billion globally in 2023, with an expected growth rate of around 4-4.5% CAGR to 2028. This growth outpaces comparable adult spending on apparel, which is expected to grow only around 2.8-3% CAGR over the same time frame. Of the estimated $28 billion US market, CRI has an estimated 10% market share – the top spot.

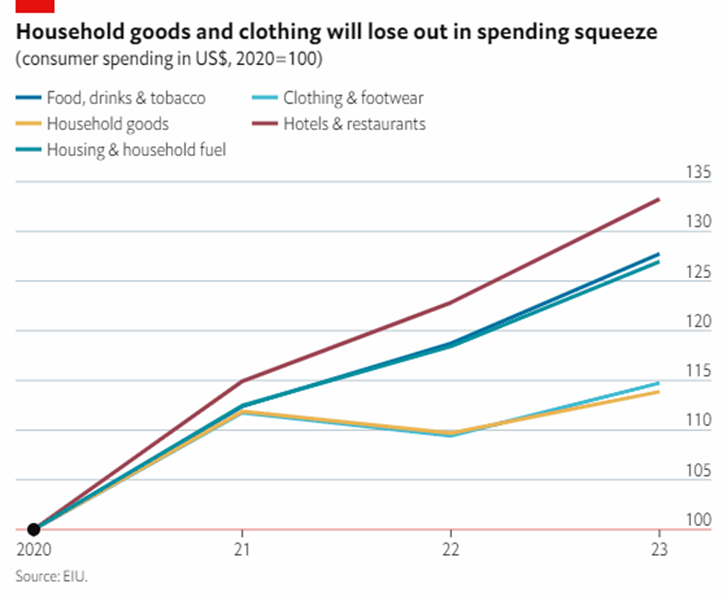

The consumer downcycle has adversely affected CRI, stating that families with young children are particularly susceptible to higher costs of living brought on by inflation. According to The Economist, while consumers have sustained spending on services, the purchasing of goods like clothing and footwear has seen a distinct drop below the trend.

We believe this effect on Children’s items may be more muted. As parents cut back on their own spending, they generally maintain spending on their children, which may limit CRI’s exposure to the downside seen thus far at other retailers.

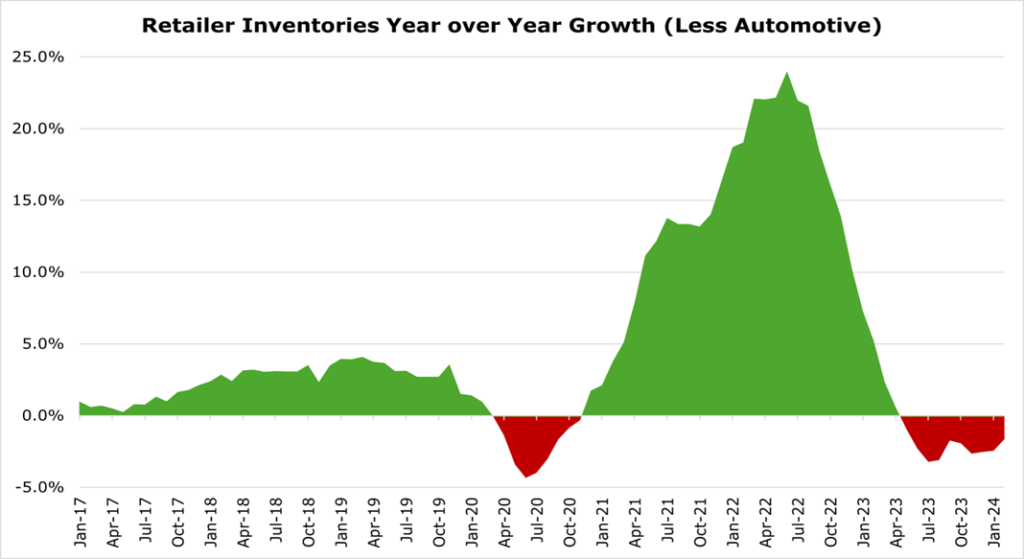

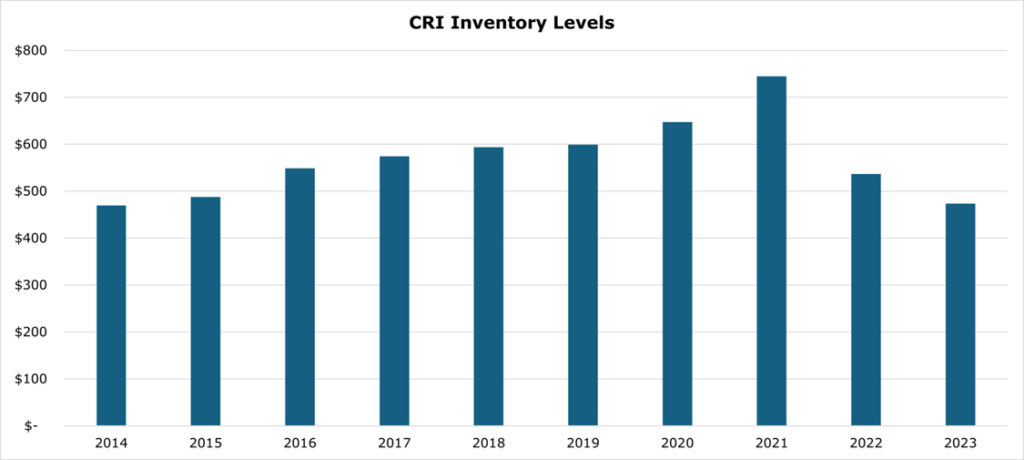

As a result of the consumer downcycle and supply chain contractions seen during the pandemic, retailers began overstocking inventory. This resulted in a glut of inventory during the consumer downturn in 2022 and 2023. CRI reports its own inventory is down 23% year over year.

The supply glut, coupled with consumer spending on goods being meaningfully weaker, has likely made retailers more conservative at inventory management. According to the Census Bureau, inventory destocking is still underway as of March 2024, albeit at a slower pace than during 2023. Most economists believe that inventories will return to a normalized level during the second half of 2024.

Primary Business

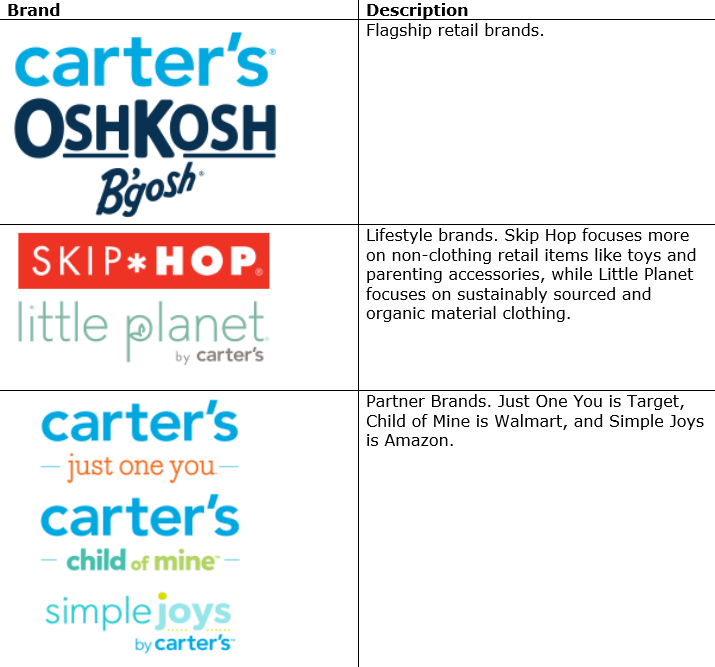

In-person shopping is still the #1 source of customer acquisition for CRI, representing 67% of the US retail segment across 789 locations. On a financial basis, CRI reports that physical locations have a 13-15% return on invested capital, which would put them above the average general retailer by at least 300bps.

To enhance operating leverage, CRI is converting individual Carter’s or OshKosh locations into ‘side-by-side’ cobranded locations. The conversion is already complete at 150 locations, and it has been reported that these side-by-side locations were the best-performing in the quarter ended March 2024. CRI did report that there was higher conversion to sales and units sold per visiting customer, with in-person stores showing a faster recovery than e-commerce.

Physical stores are also important in driving the e-commerce value chain, handling around 38% of digital orders. A key part of the e-commerce expansion strategy will be leveraging physical store openings to fulfill online orders. CRI indicated that its conversion to sales per website visit was higher than the year prior, even though web traffic was down. Given the improvement in conversion rate, CRI will focus heavily on driving traffic to e-commerce and retail locations to capitalize on higher conversion and per-customer unit growth.

The in-store retail industry saw a minor contraction of a 5% decrease in revenues. On a unit basis, sales only fell by 1%. In our view, while warmer weather contributed to better-than-expected results in the Midwest and Northern United States, continued consumer pressure across the board weighed down the segment.

CRI plans to open 40 new stores in 2024 and accelerate the pace of the conversions to side-by-side locations. Over the medium term, CRI plans to expand the retail footprint by an additional 200 openings by 2028.

Wholesale

CRI is the largest supplier of young children’s apparel to retailers in the US, managing relationships with 17,000 points of distribution, including e-commerce retailers.

CRI reported “earlier and higher than planned demand” through the quarter ending March 2024 through its wholesale channels. CRI reports, as previously discussed, that there is less long-term inventory purchasing demand from department stores and off-price retailers. In our view, sustained wholesale growth will come from branded partnerships with large retailers like Target, Walmart, and Amazon, which have seen particular strength even during the consumer down cycle. Overall, these three brand partnerships are expected to be around 54% of wholesale sales in 2024.

Overall, despite the down 6% in wholesale revenue, the operating margin expanded 540bps year over year to 24%. CRI attributed this to mix, as it was able to charge higher prices for “just-in-time” inventory while experiencing reduced transportation and production costs compared to 2023.

International

Globally, CRI has wholesale partnerships with 40 firms in over 100 countries, with 250 corporate-owned locations in Canada and Mexico, and 1,100 licensed locations in over 90 other countries. The International segment saw lower demand everywhere except South and Central America, with revenue down 3% overall or 4% on a unit basis. However, the future is bright for the international area, with CRI holding the top market share in Canada, Brazil, and Mexico.

Central and South America is quickly becoming a key market, with CRI expecting to double its square footage footprint in Mexico by 2028. The Mexican market is expected to grow by double digits in 2024. Additionally, CRI has a large wholesale market in Brazil through Lojas Riachuelo, the third-largest department store in Brazil and the largest fashion brand in the country. The Brazilian market is also expecting double-digit sales growth in 2024.

CRI expects a further contraction in the more developed Canadian market. In our view, the Canadian market will likely track slightly below the US retail segment, given weak economic conditions in Canada.

Risk

2023 saw the lowest US birthrate since 1979, largely driven by both economic downturn and lagging effects from the pandemic. Overall, fertility rates in the developed world do decline secularly over time, and the reduction seen in 2023 was not outside of the trend. If the trend were to accelerate downward, it could impact the growth in the addressable market over the long term.

The largest risk facing CRI is a delayed consumer upcycle. While most economists believe that consumers will begin the goods upcycle in late 2024, there is a possibility that the consumer downturn will last longer than expected. However, we don’t feel as though a longer contraction would pose a material risk to CRI.

54% of CRI’s wholesale market, or around 21% of total revenue, comes from 3 major retailers. Losing one or more of these relationships would have adverse effects on the business.

Outlook

The growth strategy for 2024 is largely centered around driving traffic to both physical locations and e-commerce platforms. Part of the effort to increase repeat customers is introducing a loyalty program that includes membership tiers for rewards at spending milestones. According to CRI, 93% of customers are enrolled in the program,

Other initiatives are centered around footprint growth, as previously discussed, which CRI will attempt to offset increased costs associated with expansion with productivity initiatives. We believe this will take the form of some SG&A growth during the first half of the year, which will begin to provide leverage to the bottom line as the consumer upcycle begins in the second half of the year. As previously discussed, the higher year-over-year inventory numbers expected by the end of the year will likely reduce cash flow as inventories are rebuilt. However, CRI expects less “pack-and-hold” inventory (long-term pre-order) across all segments, which will lead to an improved mix and higher year-end margins.

While the full company experienced favorable manufacturing and shipping costs relative to 2023, relatively muted demand offset this and ended the first quarter ending March 2024 down on a year-over-year basis. On the upside, CRI still performed far better than expected, with higher and earlier-than-expected wholesale demand. In our view, this may indicate that recovery in consumer discretionary is already underway or the bottom was near.

| Segment | Quarter ending June Expected | Full Year 2024 Expected |

| US Retail Revenue | Down 5-10% | Down 5% – Up 5% |

| US Wholesale Revenue | Down 0-5% | Up 0-5% |

| International Revenue | Down 5-10% | Flat |

| Earnings Per Share | $0.35-0.45 | $6.30 |

While expecting a narrow revenue recovery, CRI does expect to see a substantial earnings recovery, in the mid-single-digit range, or around $6.30. Typically, the first and second quarters of the year are the weakest for retailers, with results weighted toward the end of the year. We expect this effect to be particularly exaggerated, with consumer recovery likely not occurring until the latter half of the year.

CRI has a strong balance sheet, with a single note totaling $500 million due in 2027, with an interest rate of 5.6%. The total cash on hand was $267 million, though CRI also holds an additional $800 million short-term credit revolver, which currently holds no balance. CRI is currently BB+ rated, with a stable outlook.

The dividend in the quarter ending March was raised by 7% to $0.80/share, bringing the full yield to 4.6%. Total share repurchases on a year-to-date basis are $19 million or just under 1% of shares. Total authorization, including this number, is $649.5 million, or around 25% of outstanding shares.

Conclusion

CRI is well-positioned to leverage the anticipated consumer upcycle, backed by its strategic expansion in retail locations and e-commerce enhancements. Despite broader market challenges in the short term, CRI expects these to be at least partially offset by superior mix due to inventory management across the sector. Going into the latter half of 2024, CRI expects to see strength in retail sales through volume improvements in both e-commerce and physical locations. Moreover, CRI’s 4.6% dividend yield makes it an attractive stock for income-focused investors.

Competitive Comparisons