Economic and Market Review

March 31, 2025

| Equity Indices | YTD Return |

| Dow Jones | -0.92% |

| S&P500 | -4.37% |

| NASDAQ | -10.28% |

| MSCI – Europe | 11.33% |

| MSCI–Emerging | 4.15% |

| Bonds (Yield) | |

| 2yr Treasury | 3.89% |

| 10yr Treasury | 4.21% |

| 10yr Municipal | 3.2% |

| U.S. Corporate | 5.15% |

| Commodities | |

| Gold | $3,124.61/oz |

| Silver | $34.10/oz |

| Crude Oil (WTI) | $71.40/bbl |

| Natural Gas | $4.13/MMBtu |

| Currencies | |

| CAD/USD | $0.69 |

| GBP/USD | $1.29 |

| USD/JPY | ¥149.91 |

| EUR/USD | $1.08 |

Overview

Trump’s shifting tariff pronouncements continued to introduce significant uncertainty, with inflation indicators ticking higher. This combination pushed market sentiment into extremely bearish territory, with consumer confidence registering its lowest reading in 12 years.

However, this pessimism may be disproportionate to actual economic conditions. While stocks are down 4.6% YTD, current sentiment measures match those typically seen during much deeper 20% drawdowns and recessions. The economic data presents a mixed picture: leading indicators have been deteriorating, but current economic data remains relatively resilient.

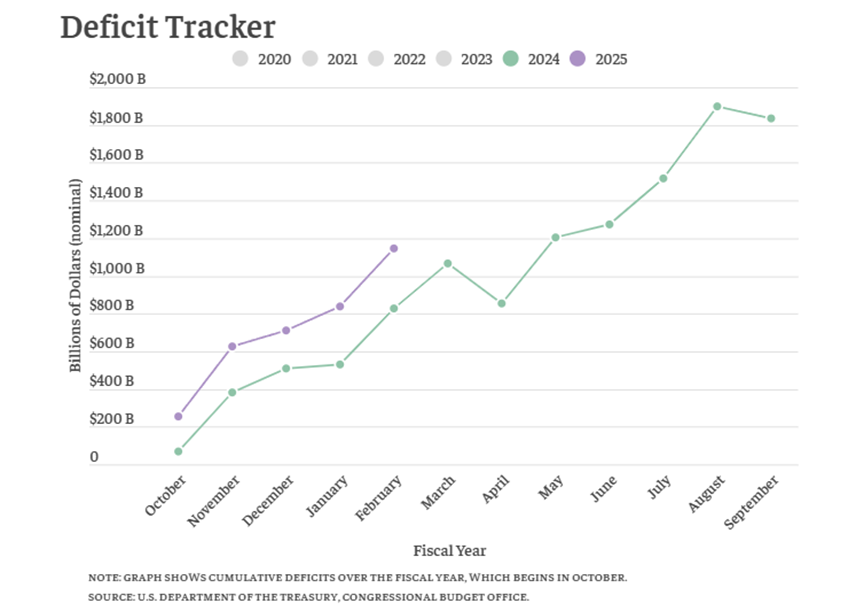

The federal deficit remains substantial, totaling nearly $1.3 trillion for the first five fiscal months of the year — approximately $500 billion greater than the same period last year. This continued fiscal stimulus has prevented economic contraction despite slowing growth.

However, this level of spending continues to fuel inflation, with PCE (personal consumption expenditures) exceeding expectations and future inflation expectations remaining elevated.

The Federal Reserve appears on track for two additional rate cuts later this year in response to expected economic weakness, though longer-term rates remain persistently high against the administration’s preferences. April 2nd has been designated as “Liberation Day,” when comprehensive tariff plans will be formalized, including potential 25% auto-import and other “reciprocal” tariffs affecting up to $1.5 trillion in trade flows. While many of these proposals may ultimately be modified through negotiations, the current uncertainty continues to weigh on markets.

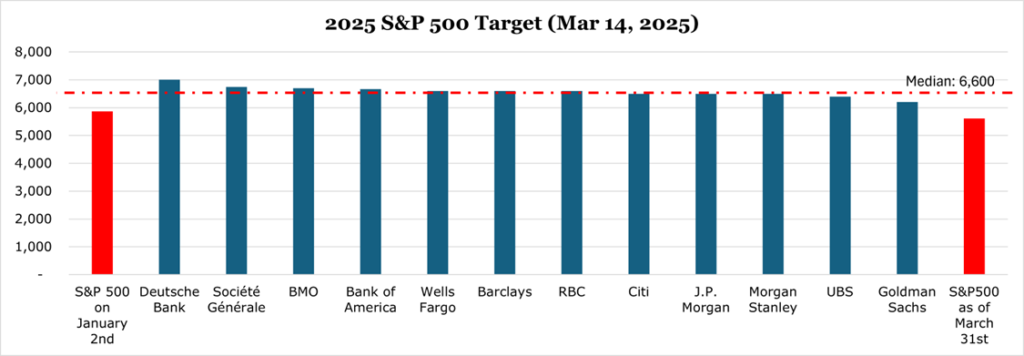

Wall Street institutions have begun reducing year-end price targets. Since the January 20 inauguration, the S&P500 has retreated by 6.8%, marking the second worst post-inaugural market performance on record. Alternative assets continue to show strength, with gold up nearly 20% year-to-date, its best quarter since 1986. This performance reflects growing concerns about economic management and financial stability.

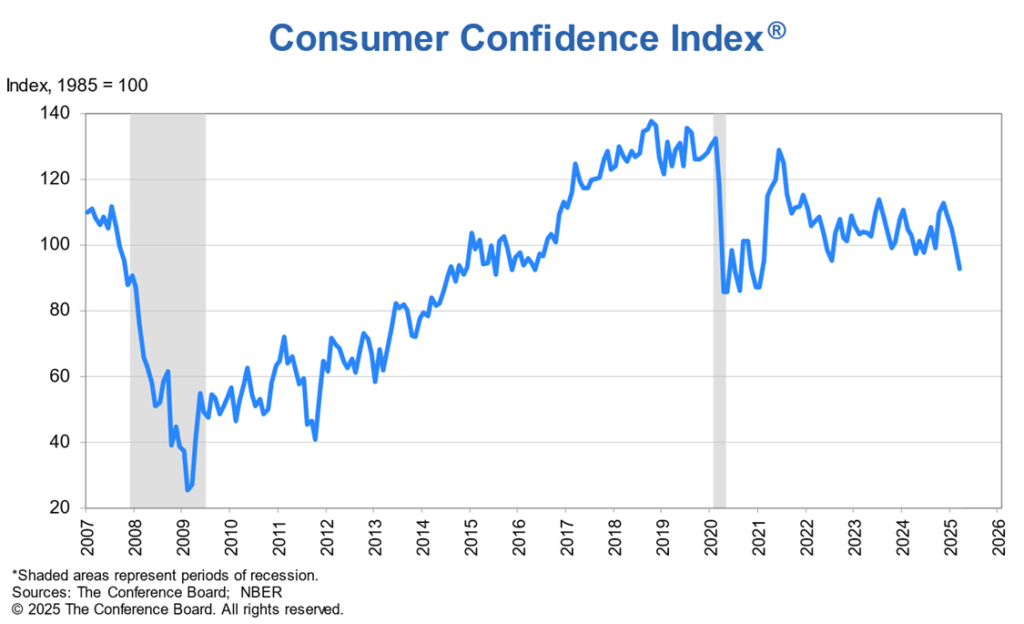

Consumer Confidence Crushed, Inflation Expectations Rise

Consumer confidence fell in March, to its lowest level in 12 years. While the election of President Trump had increased consumer confidence tariffs and aggressive government spending cuts, that have only yielded increases in the deficit, have significantly impacted future expectations.

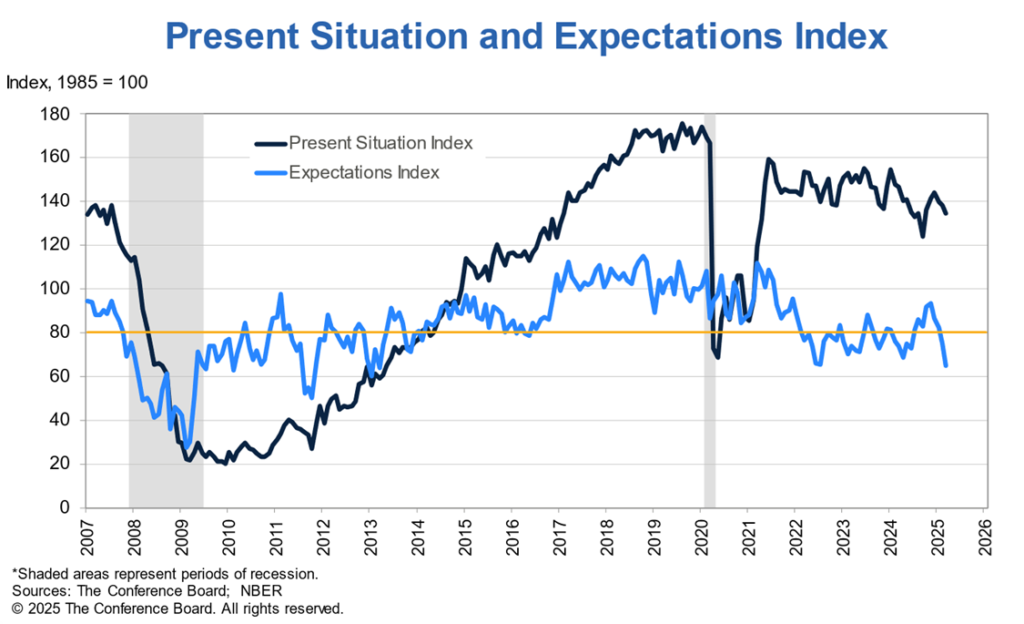

While the Present Situation Index demonstrates that consumers are still consuming at normal levels, more than 40% now indicate that they are uncertain about the future. The Conference Board maintains that any level of future expectations below 80 can indicate consumers shifting behaviors to a recessionary footing. Unlike previous releases of the index, the drop in confidence was demographically uneven compared to normal. Consumers over 55 represented much of the decline, with those in the 35-55 bracket also losing confidence. Contrary to typical releases, those under 35 saw confidence marginally increase.

In the write-in response section, consumers indicated anxiety around tariff policy and how it would affect the economy. According to the New York Fed’s survey of consumer inflation expectations, the median 12-month forward inflation rate has spiked from 3.0% in October 2024 to 4.3% at the end of February 2025.

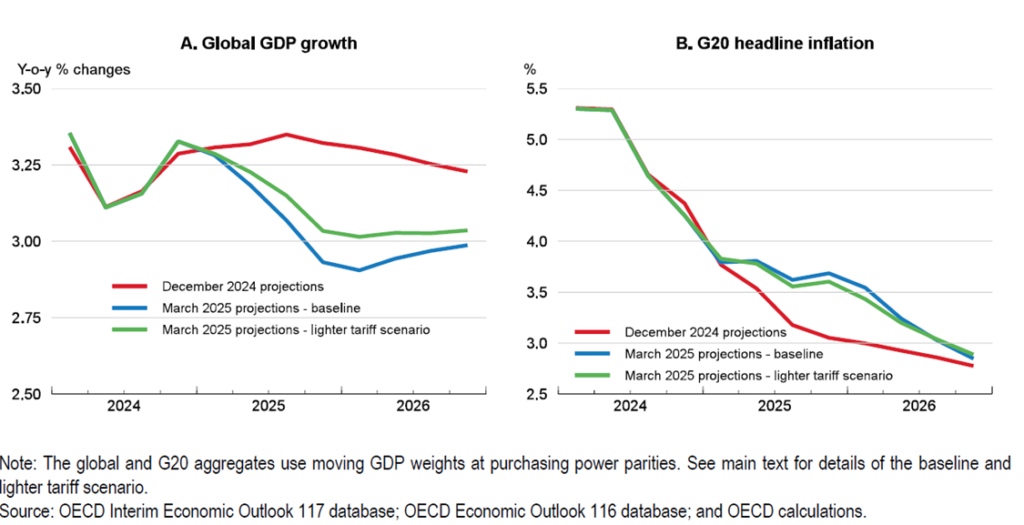

OECD Downgrades Global GDP Expectations

Global GDP growth is projected to moderate from 3.2% in 2024 to 3.1% in 2025 and further to 3.0% 2026, representing a substantial downward revision from previous forecasts. Among major economies, the United States is expected to see growth decelerate from its 2.8% pace in 2024 to 2.2% in 2025 and 1.6% in 2026.

Inflationary pressures continue to linger globally. Services price inflation remains elevated, with a median rate of 3.6% across OECD economies in January 2025. Meanwhile, goods inflation has recently turned upward in many countries, though the change has largely been a return to the pre-COVID average rather than a sudden spike above expectations. The OECD now projects headline inflation in G20 economies to fall from 5.3% in 2024 to 3.8% in 2025 and 3.2% in 2026. This level is approximately the same as previous expectations, with a moderating oil price projection offsetting goods inflation.

Another key reason, which we have discussed before, is changing tariff landscape globally. The US has proclaimed April 2nd to be “Liberation Day” – the day when sweeping tariffs are to be levied across the global economy. Already, the US has implemented 20% tariffs on China, as well as 25% tariffs on Canada and Mexico which have been marred with confusion about implementation.

Germany’s Historic Fiscal Expansion

Germany’s debt brake, known as the “Schuldenbremse,” was enshrined in the German constitution in 2009 during the global financial crisis, representing one of the most stringent fiscal rules in the developed world. The debt brake restricts the federal government’s ‘structural deficit’ (borrowing adjusted for economic cycles) to just 0.35% of GDP, while imposing even stricter rules on Germany’s 16 states, which were prohibited from running any structural deficits after 2020. The brake has been broadly effective at reigning in government spending, with Germany remaining near the bottom of the G20 and the Eurozone at debt-to-GDP.

On March 21, both houses of parliament approved a modification to the debt brake. The new amendment exempts defense spending of over 1% of GDP from the brake and adds an additional €500 billion to special carveout for infrastructure, to be spent over 10 years and be considered ‘off-budget’ and not factor into the debt limit. German states will also be permitted to run 0.35% of GDP as a deficit, matching the previous federal rule.

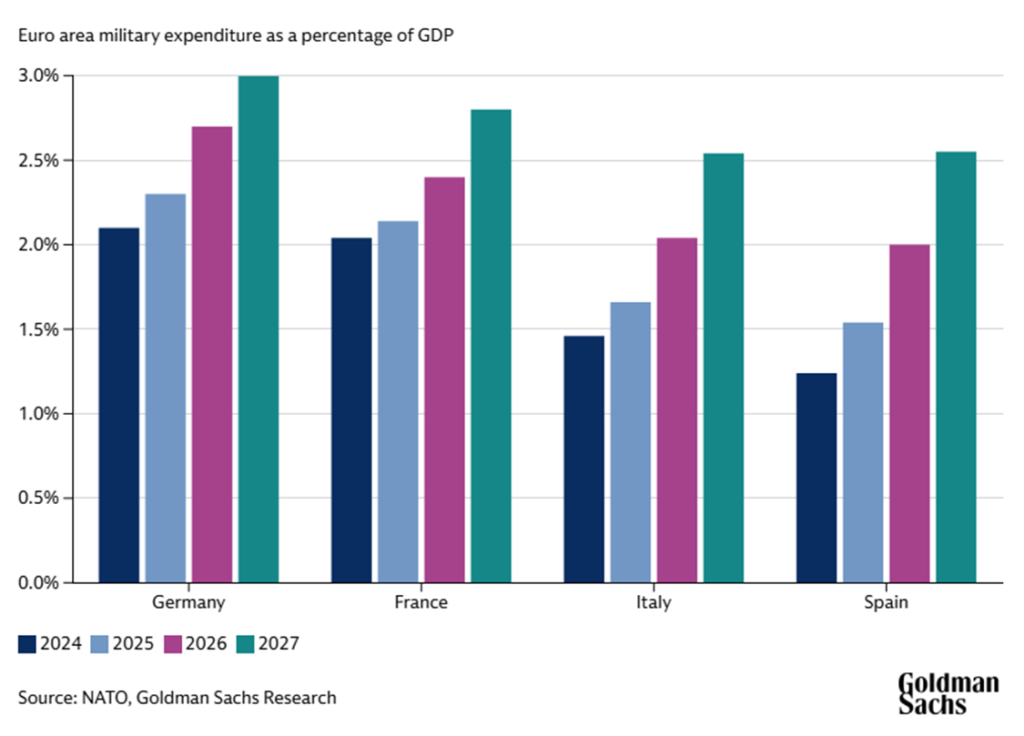

Most analysts believe that the linchpin that pushed negotiations over the edge to success was wanting to shake reliance on the United States for defense. As seen in the chart below, many major NATO partners have begun to re-adjust their spending profiles in order to re-arm amid the US’s threats to wind down its presence on the continent. Germany’s has been the most aggressive with plans to increase defense spending to more than 3.5% of GDP by 2030.

The boost in spending is expected to immediately raise GDP by 0.8% during 2025, with a further 1.5% by 2026. Largely, these increases will be linked to massive and fast increases in defense spending with a target of 3% of GDP – currently at 2.0%. Already, the Ifo business climate index reports a rise to 86.7 in March from 85.2 in February, the highest level since July 2024

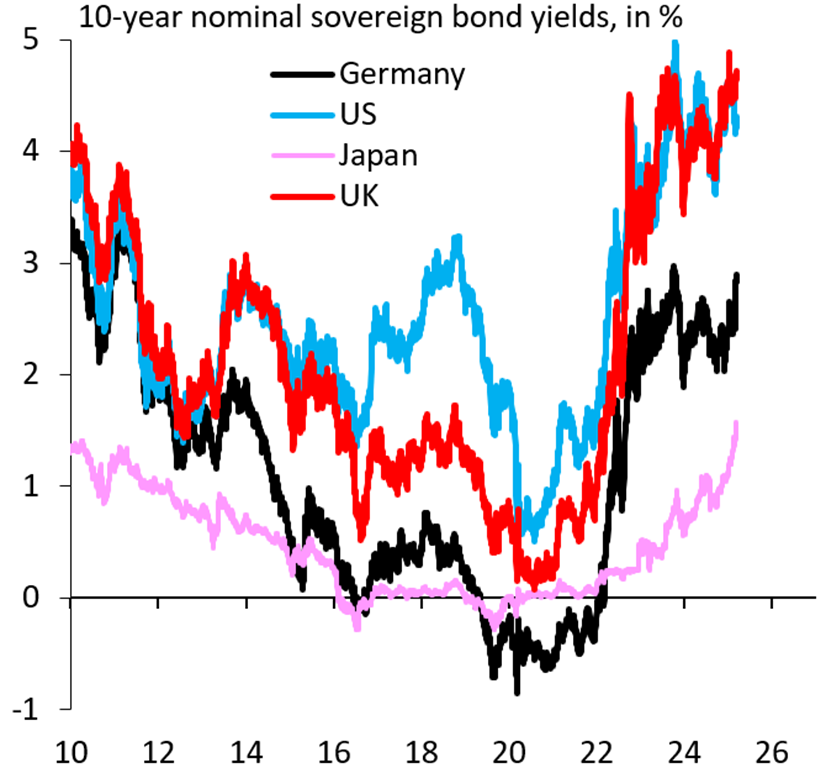

Markets began to price in this growth with EU 10-year bond yields spiking to their highest level since the end of the EU sovereign debt crisis. However, given the 10-year is still almost a full 200bps below the UK and US 10-year, the German government is likely to be undeterred. The only possible moderating factor is Article 26 of EU Regulation 2024/1263, which constrains long-term expenditure paths.

According to a Bruegel analysis, as a result of the EU regulations Germany is still likely to be moderate in its implementation, with a long-term debt-to-GDP by 2035 only rising to 83% from its current level – still below the current EU average of 88%.

Chinese Stimulus Is Working – So Far

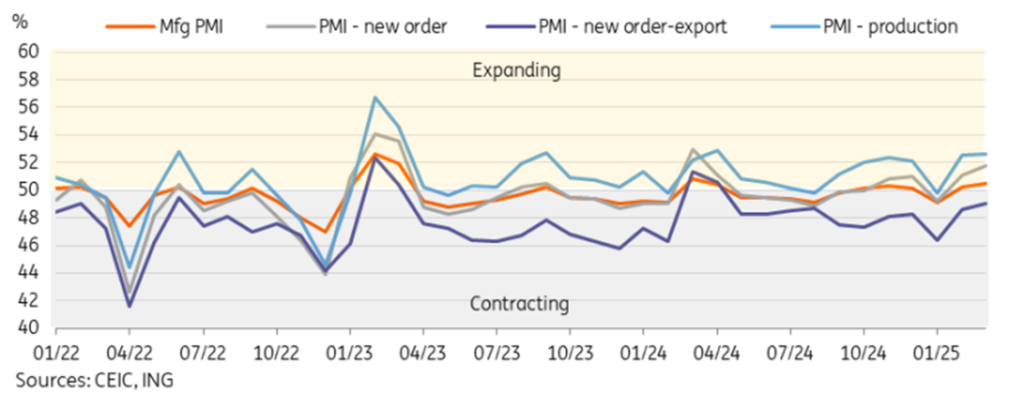

Manufacturing PMI (purchasing managers index) increased to 50.5 in March, above market expectations — though below government expectations — indicating a 5th straight month of expanding manufacturing activity. During the first 2 months of 2025, industrial output was up 6.9%, including 12% increase in automotive output and a 10.6% output for computers. Interestingly, export demand has increased to 49.0 from 48.6 which could indicate that either US tariffs imposed on March 4th have front-loading orders in anticipation for higher tariffs on more specific goods.

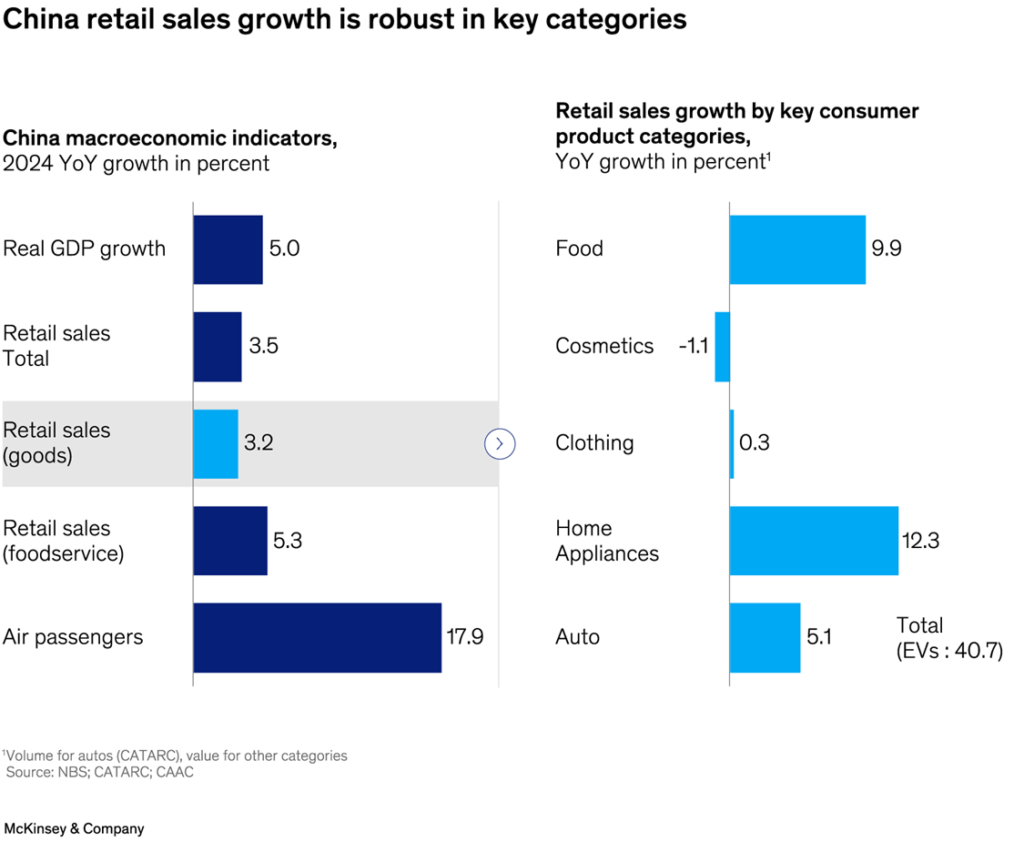

Trade-in incentives in consumer-facing sectors appear to be working, with the $41 billion program boosting consumption above expectations in the full year 2024, and even exceeding expectations in 2025 with the expansion of qualifying items. EV (electric vehicle) manufacturing grew 85% year over year in March, with long-term effects of stimulus expecting to continue until at least 2026. In the first two months of 2025, retail sales were up 4.0% year over year.

Despite tariffs, business expectations remain high at 57.2 which may give water to the ambitious 5% GDP growth target imposed by the government for 2025. Fixed asset investment, excluding investment properties, climbed by 8.4% year over year during February 2025.

The Chinese government has announced its intentions to continue and expand this stimulus, including in the service sector. The government is expected to introduce subsidies for childcare, AI, and ‘snow-tourism’ promoting domestic vacationing. Broader long-term goals include additional rural ‘housing reform’ and local government incentives for providing better wages to workers.