Economic and Market Review

June 30, 2026

| Equity Indices | Index Level | YTD Return |

| Dow Jones | 52,665.71 | 8.85% |

| S&P500 | 7,516.56 | 9.60% |

| NASDAQ | 26,156.56 | 12.57% |

| S&P Developed Ex-US | 523.81 | 12.36% |

| MSCI–Emerging | 949.30 | 23.85% |

| Bonds (Yield) | ||

| 2yr Treasury | 4.13% | 0.51% |

| 10yr Treasury | 4.38% | -0.02% |

| 10yr Municipal | 2.90% | 2.93% |

| US Prime Rate | 6.75% | |

| Commodities | Price | YTD Return |

| Gold | 4,083.84 | -6.71% |

| Silver | 60.34 | -18.25% |

| Crude Oil (WTI) | 68.10 | 18.64% |

| Natural Gas (NYMEX) | 3.22 | -13.31% |

| Currencies | Index Level | YTD Return |

| Dollar Index (DXY) | 101.30 | 3.03% |

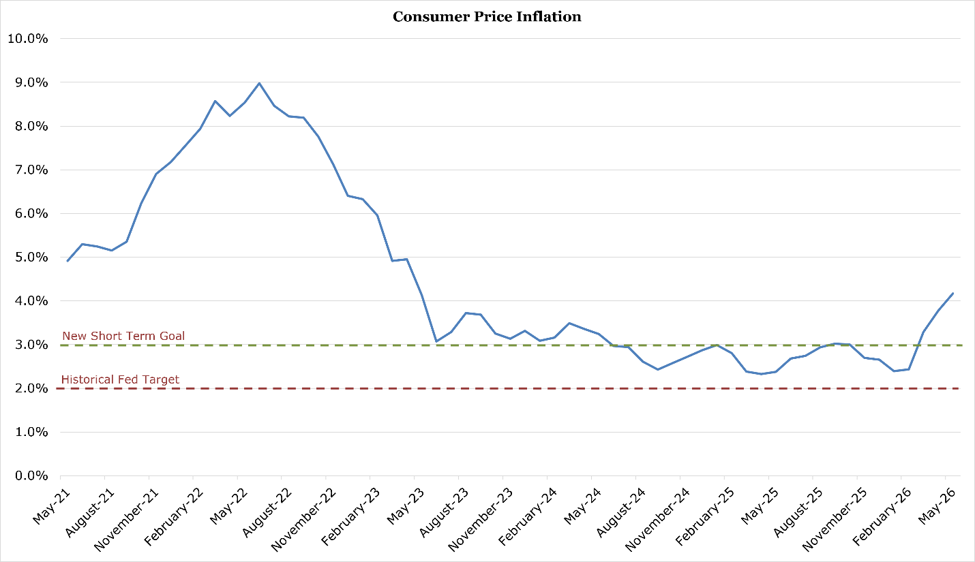

Inflation Has Peaked for This Cycle

Inflation has peaked for this cycle. The four-and-a-quarter percent year-over-year CPI reading for May looks like the high, and the rate should decline from here and into next year, heading toward roughly three and a half percent. That is still above the Fed’s stated goal of 2%, or the “under 3%” the new chairman has signaled, but it is an improvement on where inflation ran after the Iranian war and the oil spike.

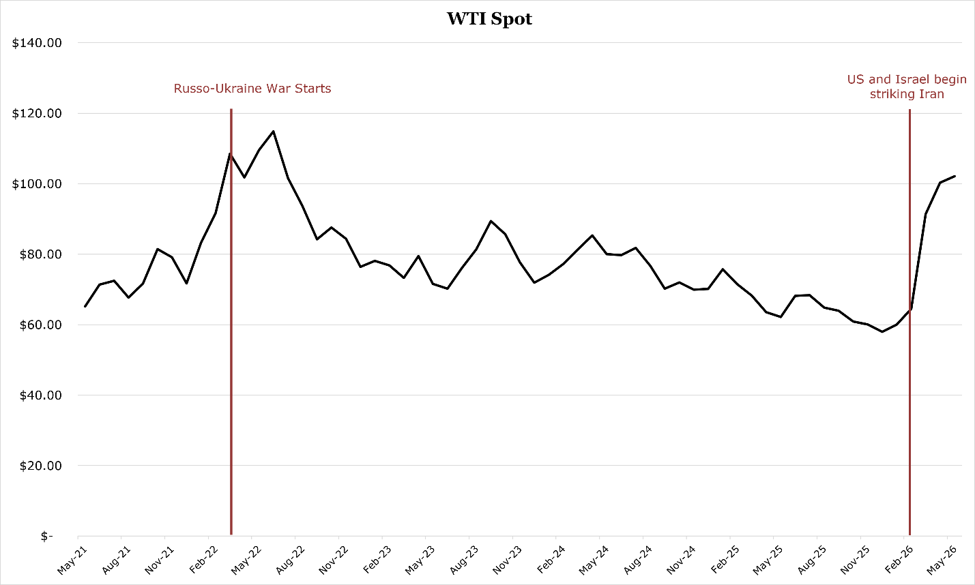

Oil was the biggest driver. Prices jumped during the war and reached about $112 a barrel. Crude has since retraced to roughly $69, close to where it traded before the war began. That should let inflation roll down, energy feeds into nearly every product, from making plastic to the gasoline in your tank. It is a central input to the economy and a key driver of cyclical inflation.

A ceasefire and a signed memorandum of understanding should move things toward ending the Iranian war, but skirmishes continue. Iran attacked ships, the United States retaliated against Iranian military facilities, and the situation could deteriorate again. Our current working assumption even with the skirmishes is that the war winds down rather than flaring back into a full conflict. Barring a full-scale war, energy prices have likely peaked and could fall below pre-war levels. OPEC is fraying, with the UAE leaving so it can produce more oil, and Iraq wants its quotas raised sharply or it may threaten to exit. With the cartel in disarray, oil production could rise enough to overwhelm demand for a stretch and push prices down hard.

We have positioned our portfolios for that. Exploration stocks are now underweight across the board. Oil markets can swing violently, as the past six months show, and during COVID demand collapsed so far that crude briefly traded below zero in the futures market. We will keep following it, but for now we are light on oil equities.

Before leaving energy, we hold meaningful positions in natural gas producers and the pipelines that move gas to market. US natural gas in particular benefits from the shut-in of Russian supply as Europe weans itself off Russian gas. Qatar lost a significant share of its liquefied natural gas (LNG) capacity to damage during the Iranian war, which will crimp global LNG supply and support gas prices further.

Artificial intelligence is growing fast, and it is an energy hog. The only way to add power cost-effectively and quickly today is natural gas, so gas-fired generation is going up to feed AI data centers, and that is driving gas demand. Nuclear power, including new plants and small modular reactors, is the longer-term answer, but it is years away. Wind and solar depend on the weather, which makes them unreliable, and even where they are installed you still need gas plants to cover the gaps when the wind drops or the sun sets. Natural gas sits in the sweet spot, and we like the space. AI is one of the main forces behind it.

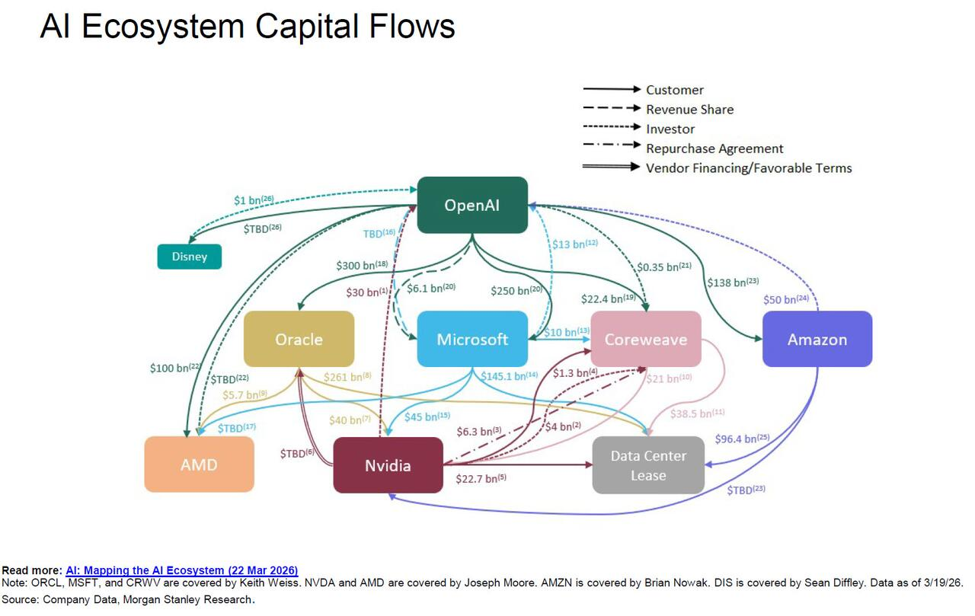

AI Capex Continues to Explode

The spending to build AI has surged. The SpaceX IPO, one of the largest ever, valued the company above $1 trillion almost immediately. One of its biggest divisions is xAI, merged in a few months before the offering. OpenAI, the company behind ChatGPT, and Anthropic, the company behind Claude, are also planning IPOs. This past week OpenAI announced it is pushing its IPO to 2027. That rattled AI-related investors, because these businesses need enormous amounts of capital. OpenAI needs funding to build its planned data centers and to invest in its models, and it cannot proceed without raising more, because the business currently loses billions of dollars a year. Postponing the IPO is a warning flag that the AI spending boom may be near a peak. Anthropic is on firmer financial footing than OpenAI. It will probably still come to market this year, though its finances may not require it, and it could instead raise another private round from private equity and venture capital.

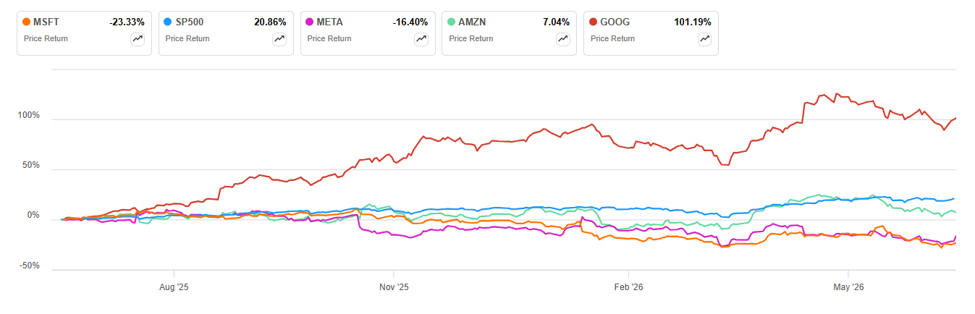

The boom is enormous. The four hyperscalers, Google, Microsoft, Amazon, and Meta, are approaching a combined trillion dollars in capital expenditure, roughly triple their spend of a few years ago. That capex now matches or exceeds their cash flows, so they are turning to outside financing. Google has already done a secondary stock offering, and we expect the others to issue substantial debt to fund the buildout.

The cash flows AI generates today do not justify the spending, on either an operating or a capital basis. Investors are starting to worry that AI, revolutionary as it is and likely to reshape the workforce, especially knowledge work, will not produce enough revenue and profit to pay for what is being spent. The four hyperscalers are down year-to-date in aggregate, because they are pouring out cash and no longer generating the free cash flow that made them reliably profitable for decades.

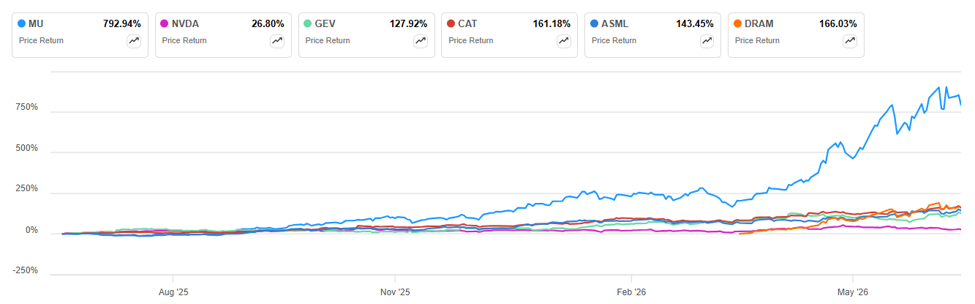

The market is repricing them. The money is going somewhere, though, and most of it flows to semiconductor companies, which are seeing booming demand and pricing power. It also flows to electrical generation and grid connections, to cooling, and to construction.

That has produced a boom for the hyperscalers’ suppliers, and any pullback in spending would test the pricing power those suppliers now hold. In semiconductors that pricing power has been extraordinary. Nvidia is posting gross margins the industry has never seen, and memory makers have recently tripled or quadrupled their prices. If spending eases and some of the double-ordering gets cancelled, the stocks of these memory and semiconductor names could take real damage.

The boom is bigger than almost anyone expected two years ago, and it is setting up for at least a slowdown toward more rational spending. We are wary of AI names broadly, though we still own a few in more aggressive accounts.

Our core strategy stays focused on dividend value: broad-based companies across many sectors that grow dividends, earnings, and free cash flow and trade at reasonable valuations. Many of these have been neglected while attention fixates on AI. A large number now merit a close look and ownership.

Real Assets Hold Value and Diversification is Key

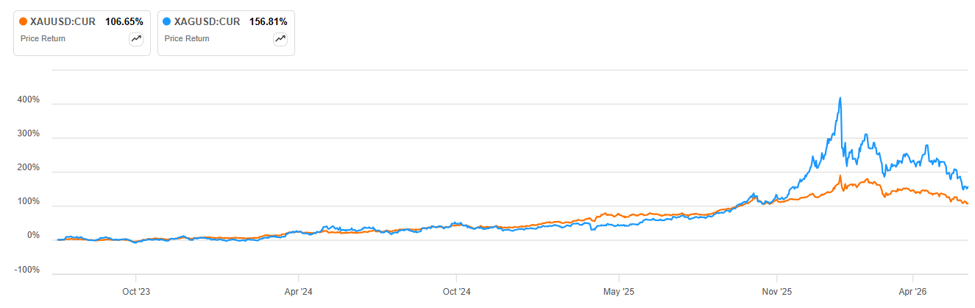

Our multi-year case for gold and silver, that both were badly undervalued and due to re-rate higher, played out through 2025 and into early 2026. Both have since fallen hard. That happened even during the Iranian war, when a flight to safety would normally lift them. It did not this time.

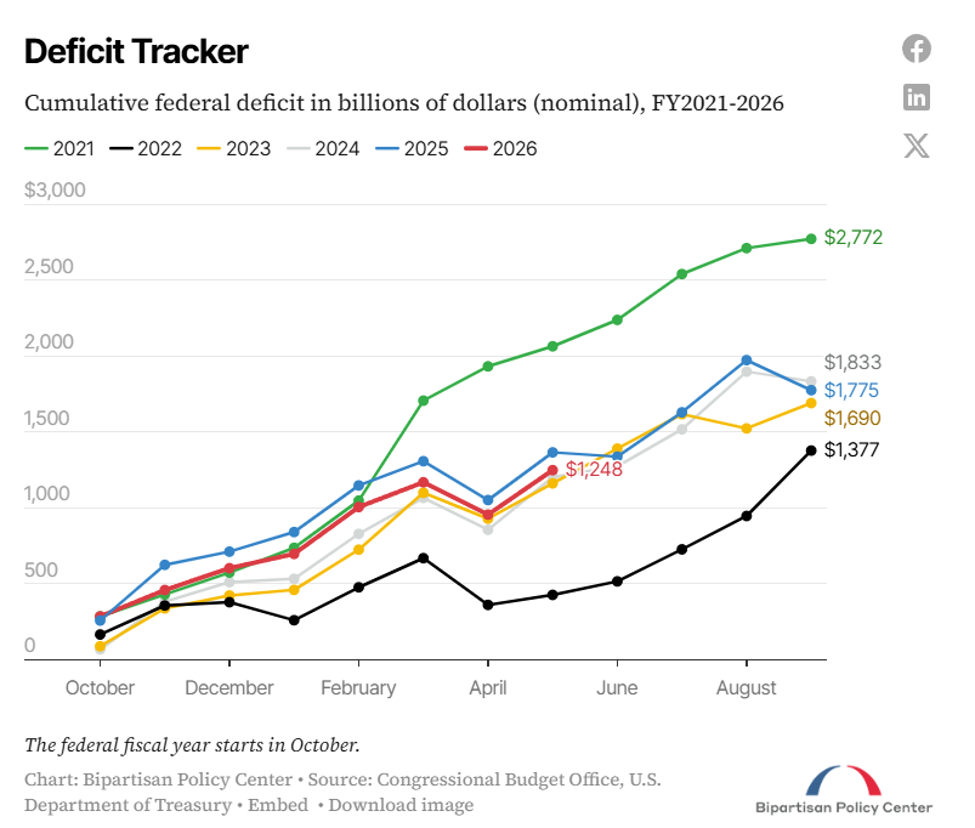

With the US federal government running a deficit above $2 trillion dollars a year and debt approaching $30 trillion, real assets make sense over time. The deficits driving that debt look politically unfixable given entrenched special interests, so the debt load has entered an exponential spiral. That favors real assets, stocks, and most things priced in dollars. As the dollar loses value, dollar prices for other assets rise. For some of these assets the gain is not real economic growth, only that they should hold value better than dollars or fixed income.

So we remain light holders of fixed income and significant holders of stocks, commodities, real assets, and other diversifying assets. We think that positioning is sound, and it has served well over the past few years.

If you have questions about your portfolio or would like more information, call or email us.