ALB: Doubling In Size Inside a Decade

| Price $205.67 | Growth Holding | May 16, 2023 |

- Second largest Lithium producer in the world.

- 3 Expansion opportunities within the next decade, expecting global lithium demand to surge by 275% by 2030.

- Favorable pricing above $20/kg has made >100 locations viable for expansion.

- Global focus on electrification creating surge in demand for Lithium.

Investment Thesis

Albemarle (ALB) is one of the largest Lithium producers in the world. Lithium is experiencing surge in demand with electrification of vehicles, with global EV sales up 73% year over year. In addition, surging prices have made new developments economically viable for the first time; nonetheless, demand is still expected to outpace supply creating a shortage.

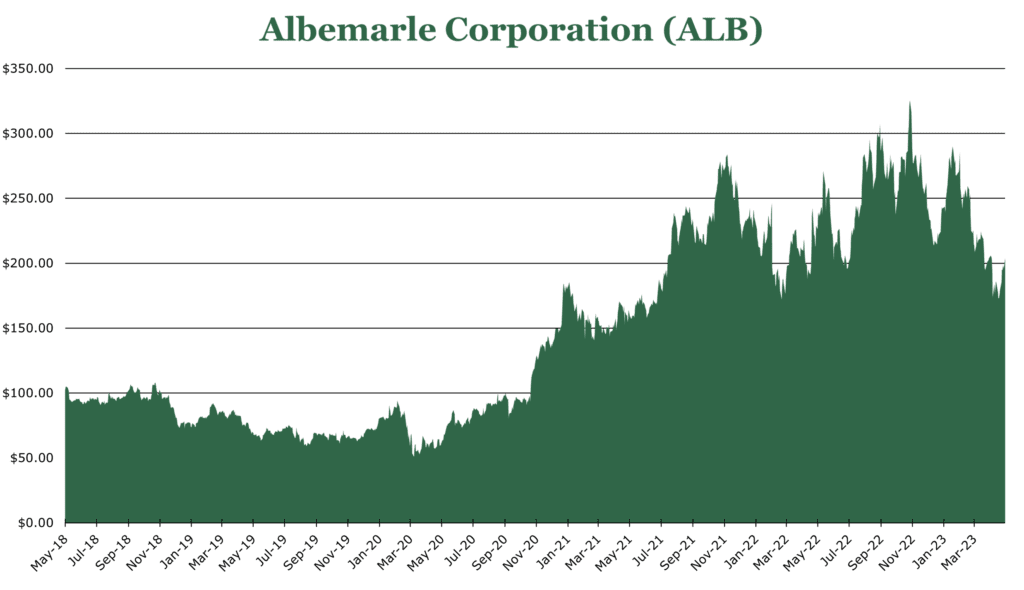

ALB is an experienced player in the chemicals space and has the experience for mining, refining, and manufacturing required for electrification to proceed. The recent drop in price experienced by ALB, driven by a retracement of last year’s surge in Lithium price, marks a good entry point for the long-term investor to capitalize on a critical resource.

Estimated Fair Value

EFV (Estimated Fair Value) = E24 EPS (Earnings Per Share) times PE (Price/EPS)

EFV = E24 EPS X P/E = $21.00 X 12.5 = $ 262.50.

| E2023 | E2024 | E2025 | |

|---|---|---|---|

| Price-to-Sales | 2.4 | 2.3 | 2.2 |

| Price-to-Earnings | 9.0 | 8.6 | 8.8 |

Business Overview

ALB operates two primary divisions, Lithium and Chemical Catalysts – largely Bromine products.

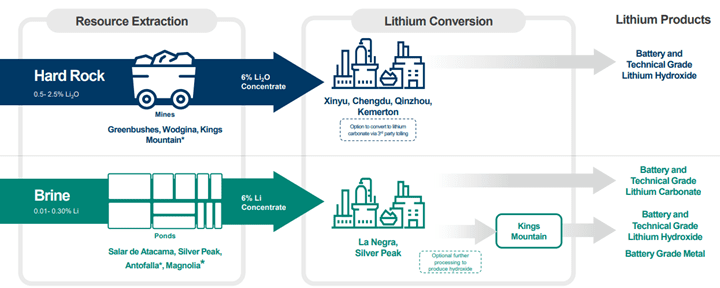

There are two primary methods for converting Lithium into concentrate capable of being utilized in industrial products. Lithium is found in Lithium-Oxide rock and Lithium based brine-pools. Brine pool extraction is often called DLE (Direct Lithium Extraction). Either form is converted into various Lithium products, such as Lithium Carbonate or Lithium Hydroxide for batteries.

Presently, ALB owns 4 DLE facilities and 3 Lithium-Oxide rock facilities. Four of these are operational. The Chilean DLE facility, a Nevada DLE facility, and two Australian Lithium-Oxide rock mines, with 49% working interest and 60% working interest, respectively. The remainder are in the exploratory and development stages.

The exploratory facilities are in North Carolina, Arkansas, and Argentina. King’s Mountain in North Carolina was once one of the world’s largest Lithium-Oxide rock mines but shuttered in 1988. ALB seeks to utilize existing infrastructure and a $150 million grant from the Department of Energy, to re-open the mine now that economic conditions are more favorable. The existing mine infrastructure is estimated to have 10-15 years of viability remaining, with potential deposits in the surrounding 800 acres that ALB purchased.

Arkansas is a DLE development, working as a co-facility with the existing ALB Bromine operation. Arkansas sits on a unique formation called the Smackover Formation, providing the world’s largest sources of commercialized Bromine and a significant amount of oil. Early experiments indicate that the same brine containing Bromine can also be used to extract Lithium. The exact conversion ratio is unknown, but ALB announced $540 million in expansions to its operations in Arkansas.

The New Antofalla Argentinian facility is on the same formation as the existing Salar de Atacama facility – known as “The Lithium Triangle.” Argentina has some of the world’s largest reserves of DLE Lithium, with ALB 5411 hectares of land. ALB stated that its purchase could become one of the largest producing areas in Argentina. Previously no serious investment or exploration has been made in the Antofalla region by any company – but it has recently become the site of a major bidding war.

As for conversion, ALB operates 7 facilities globally. There is definitive plans for groundbreaking in 2024 for a new facility in South Carolina which will provide a diverse range of Lithium products utilizing domestic production. In addition, a new Asia Pacific facility and a new European facility are planned. However, both are still in the early stages, and little detail has been given.

Outside of the Lithium space, ALB refines and manufactures Bromine. In addition, ALB invested additional funds into a joint venture with the Arab Potash Company to open a recycling operation at the existing facility in Jordan. This recycling facility will turn byproducts into high-value-added materials and reduce the loss. Once at full capacity, it is expected to reduce production costs by $2 million in the first year.

Strategy

ALB is a global leader in Lithium batteries for electric vehicles, with 64% of revenues coming from energy storage.

Lithium demand in 2030 is expected to be 3.7 million tons per year. This translates to a 500% increase in the total addressable market by 2030, with most new demand for EVs. For the most favorable economics of expansion, prices of >$20/kg are required. Resources cost $5-25,000 upfront per annual ton of nameplate capacity. Even assuming a favorable growth rate of an additional 20,000 tons annually, 2030 will only have 3.0 million tons of nameplate capacity. Given regulatory and infrastructure requirements, ALB has averaged 10 years before initial production for mining operations. By 2030, including planned additions and acquisitions, ALB expects to reach 400-650,000 tons of production annually. This would be triple the current capacity of 200,000 tons per year.

Outside of the Lithium space, leveraging existing customers to expand the number of products sold is a key tenant for the sustainability of growth. Novel product launches are expected to increase sales by 10% by FY27, a 5-year CAGR of 5%.

Risk

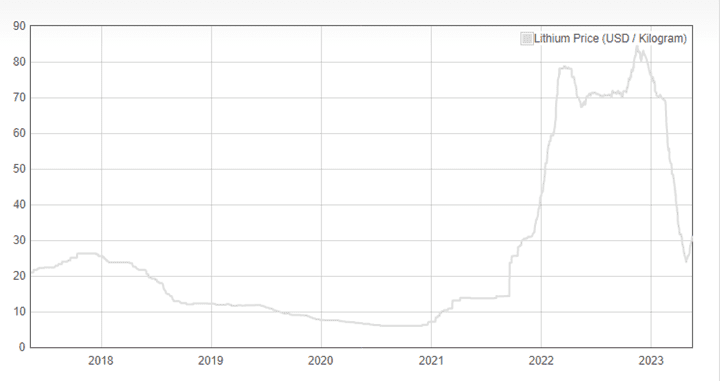

The most critical component in sustaining the growth of ALB is Lithium pricing. Recently, Lithium prices have tumbled 40% since their highs early in FY23. While the current price of around $30/kg is certainly higher than in previous years, and within the $20/kg target set by ALB, there is still volatility in the market. Historically, Lithium has hovered between $7/kg to $25/kg. A return to this price level would remove many locations from economic viability.

The regulatory burden is high in the mining industry. ALB has an average of 10 years from exploration to opening for mining facilities across both DLE and Lithium-Oxide methods. While the Department of Energy has demonstrated a willingness to offer grants, much of the regulatory process is up to local governments. A significant change in the temperature toward ALB by the public or government could significantly place ALB behind the competition.

The Chilean government has moved to Nationalize lithium resources. Foreign utilization of Chilean Lithium will likely be done through joint ventures. Per ALB and per the Chilean president, leases will be honored for their length, of which ALB has a decade left. In our opinion, it is unlikely that all private utilization of lands in Chile for Lithium will be banned. Chile is a key supplier and should help reduce the world’s dependence on China as the primary supplier of Lithium. The exact details of what nationalization looks like are not clear as of the writing of this article.

Outlook

FY23 is expected to continue the trend of hyper-growth, with a 35-55% net sales increase expected. However, this trend will be more moderate over the longer term, with ALB expecting a 20% 5-year sales CAGR. In 1Q23, sales increased 129%, with the EBITDA margin expanding from 2400 bps to 62%.

We expect a contraction in EBITDA in the latter half of the year. In February of FY23 Lithium prices collapsed from their high of $83/kg, to $25/kg. Downstream supply agreements to OEMs range in the 2–5-year range. However, ALB acquires inputs utilizing contracts with a 3-month lag to market price. The 3-month lag contract model accounts for 90% of sales, with only 10% utilizing spot agreements.

For this reason, we will likely see a decrease in the EBITDA margin of 700 bps to 1300 bps realized in 2Q23. This will bring the EBITDA down to the 37-40% range. In perspective, this is still a more favorable margin position than ALB was in FY21, which was 26%.

Over the long term, ALB expects to achieve a stable 41-44% EBITDA margin by 2027 while maintaining a net debt-to-EBITDA ratio of 0.5x. In the short term, ALB expects to maintain 1x debt-to-EBITDA to maintain flexibility in expansion, with a ceiling at 2.5x debt-to-EBITDA.

In a similar trend to EBITDA and sales, ALB expects a 5-year CAGR to free cash flow of 30%. As previously mentioned, the regulatory environment often requires 10 years of permitting and planning before initial capacity can be reached. This cash flow will be instrumental in expanding greenfield and brownfield expansion capacity or through M&A or joint ventures. Dividends are expected to have their 29th consecutive year of growth in FY23. However, the volume of buybacks is expected to remain the same or decrease as ALB invests in growth.

In FY22, global EV sales increased by 72% year over year, and decarbonization is near the top of the corporate priority list. Strategically, the importance of domestic Lithium production and conversion cannot be understated. China controls 60% of the world’s Lithium refining capacity, and the Inflation Reduction Act seeks to tip the balance. Over the next decade, a critical electrification metal like Lithium will become a strategically important resource. ALB represents an excellent opportunity for a long-term investor to participate in the growing demand for Lithium.

Competitive Comparisons

| Albemarle (ALB) | DuPont de Nemours (DD) | Sociedad Química y Minera (SQM) | FMC Corp (FMC) | Pilbara Minerals (PILBF) | |

|---|---|---|---|---|---|

| Price-to-Earnings (FWD) | 9.04 | 18.07 | 6.30 | 14.20 | - |

| Price-to-Sales (TTM) | 2.72 | 2.5 | 1.96 | 2.39 | 4.51 |

| Price-to-Cash Flow (TTM) | 10.07 | 41.71 | 5.09 | 41.30 | 5.94 |

| EV-to-EBITDA (FWD) | 7.19 | 11.16 | 4.11 | 11.46 | 3.60 |

| Dividend Yield | 0.79% | 2.19% | - | 2.11% | 4.70% |